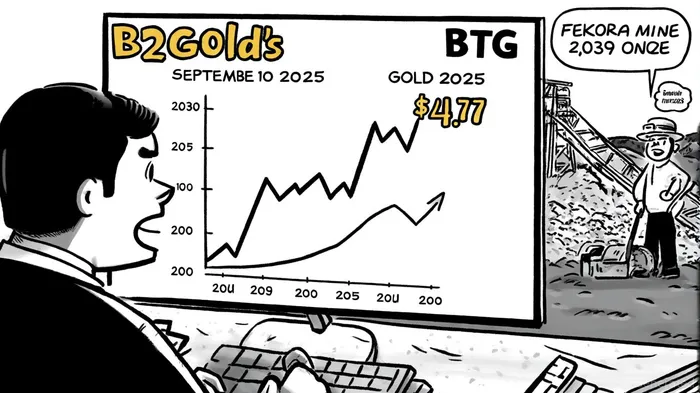

B2Gold's 52-Week High and Strategic Catalysts for Growth

The gold sector is experiencing a renaissance driven by a potent mix of macroeconomic forces. As inflation remains stubbornly elevated and geopolitical tensions escalate—from the ongoing war in Ukraine to escalating U.S.-China trade frictions—investors are increasingly turning to gold as a hedge. B2Gold Corp.BTG-- (BTG), a mid-tier gold producer with a robust growth pipeline, has capitalized on this environment, with its shares hitting a 52-week high of $4.77 on September 10, 2025, marking a 64% surge in six months and a 58% gain year-over-year [1]. This performance underscores the company's strategic positioning to unlock value in a sector primed for expansion.

Macroeconomic Tailwinds: Inflation and Geopolitical Uncertainty

Gold's appeal as a store of value has been rekindled by inflationary pressures and geopolitical volatility. According to a report by S&P Global Market Intelligence, gold prices have surged to a 19-month high of $2,039 per ounce, driven by central banks' aggressive rate hikes and persistent inflation [2]. Historically, gold has thrived in such conditions. For instance, during the 1971–1980 period, gold appreciated by 2,300% as the Dow Jones Industrial Average declined by 25%. Analysts at Forbes argue that similar dynamics—stagflation and geopolitical risks—could push gold prices toward $5,000 per ounce by 2030 [3]. This macroeconomic backdrop creates a fertile ground for gold sector value unlocking, particularly for companies with disciplined operational execution.

B2Gold's Strategic Catalysts: Operational Expansion and Cost Efficiency

B2Gold's recent stock price surge is not merely a function of macro trends but also a reflection of its operational momentum. The company's Fekola expansion in Mali and the ramp-up of the Goose Mine in the U.S. are pivotal to its growth narrative. As highlighted in a Seeking Alpha analysis, these projects are expected to significantly boost cash flow and production capacity, even amid geopolitical headwinds [4]. For example, the Fekola mine, which began commercial production in 2023, is projected to produce 500,000 ounces annually by 2026, while the Goose Mine's output has already exceeded 200,000 ounces in 2025.

These initiatives are underpinned by B2Gold's cost discipline. The company's all-in sustaining cost (AISC) of $750 per ounce in Q2 2025—well below the current gold price—positions it to generate robust margins. This efficiency is critical in a sector where operational costs can erode profitability during volatile price cycles.

Earnings Momentum and Analyst Outlook

B2Gold's financial performance has mirrored its operational success. The company reported a doubling of Q2 2025 earnings per share (EPS) to $0.12, with revenues surging to $692 million [1]. However, recent analyst forecasts suggest tempered expectations for the remainder of 2025. Cormark lowered its Q3 2025 EPS estimate to $0.17 from $0.22, citing seasonal production challenges, while projecting Q4 earnings at $0.28 [5]. Despite these adjustments, the stock maintains a “Hold” consensus rating, with a price target of C$6.75. Notably, Raymond James Financial upgraded B2GoldBTG-- to a “moderate buy,” citing its strong balance sheet and growth trajectory [5].

While the company's earnings reports have historically shown mixed short-term market reactions—with only three data points available since 2022—the observed trends suggest a mild positive drift in performance two to three weeks post-announcement. For instance, cumulative excess returns reached approximately +10–12% between days 21–30 after earnings releases, though these results lack statistical significance due to the limited sample size. This aligns with the broader narrative of B2Gold's long-term operational execution outpacing near-term volatility, reinforcing the case for a buy-and-hold strategy in a sector where fundamentals often take precedence over quarterly fluctuations.

Dividend Yield and Risk Mitigation

B2Gold's recent quarterly dividend of $0.02 per share, representing an annualized yield of 1.3%, further enhances its appeal in a high-interest-rate environment [5]. While the yield is modest compared to equities, it reflects the company's commitment to returning capital to shareholders—a rarity in a sector often criticized for underinvestment in dividends. This strategy helps mitigate risks associated with gold's price volatility, offering investors a dual benefit of capital appreciation and income.

Conclusion: A Strategic Bet in a Resilient Sector

B2Gold's 52-week high is a testament to its ability to harness macroeconomic tailwinds through disciplined execution and strategic expansion. While near-term risks—such as geopolitical disruptions in key mining regions—remain, the company's low-cost operations and growth catalysts position it to outperform peers. For investors seeking exposure to the gold sector's long-term potential, B2Gold offers a compelling blend of operational resilience and value creation.

Comentarios

Aún no hay comentarios