Should You Avoid WDAY Stock Amid Declining Estimate Revisions?

Earnings estimates for Workday, Inc. WDAY for fiscal 2027 and fiscal 2028 have moved down 0.4% and 1.1% to $10.50 and $12.32 per share, respectively, over the past 60 days. The negative estimate revision depicts bearish sentiments about the stock’s growth potential.

Image Source: Zacks Investment Research

What Ails WDAY?

Workday historically grew rapidly because it was one of the first cloud-based providers for financial management and human resources domains. But now the company is entering a more mature stage, and growth is naturally slowing.

Much of this stunted growth is due to market saturation, with most large enterprises that want modern HR software already adopting cloud solutions. Moreover, WorkdayWDAY-- primarily targets large enterprises, which means the number of potential new clients is limited. In addition, HR systems generally change slowly (often every 8–10 years), limiting frequent upgrades.

Despite efforts to broaden its market presence, Workday continues to derive a substantial 75% of its revenue from the United States. The lack of geographical diversity exposes the company to various market risks. Economic downturns, shifts in consumer preferences and changes in the regulatory environment often drastically impact Workday’s revenues and profitability. While Workday offers a range of applications, the process of customizing and seamlessly integrating its software with an enterprise's existing systems can be a challenging and time-consuming endeavor.

Stiff Competition, Waning Margins Hurt WDAY

Competition in the Human Capital Management (HCM) and financial management software market is increasing, leading to pricing pressure and affecting Workday’s margins. Oracle’s strong momentum in the cloud is a headwind for the company. Moreover, we believe that Workday’s dominance could be challenged by new entrants. This could make the company resort to competitive pricing to maintain and capture further market share. Apart from this, the ongoing trend to invest more in cloud solutions exposes Workday to the risk of losing existing “on-premise customers”, which can adversely impact its top-line performance, especially in the near term.

The company’s margin continues to be affected by higher operating and SG&A expenses, primarily due to an increase in headcount and marketing spending. As of Jan. 31, 2026, Workday had more than 23,000 employees compared with about 1,500 employees as of its listing date in October 2012. We believe Workday’s continuous investments to achieve long-term growth will hurt its margins in the short term.

Image Source: Zacks Investment Research

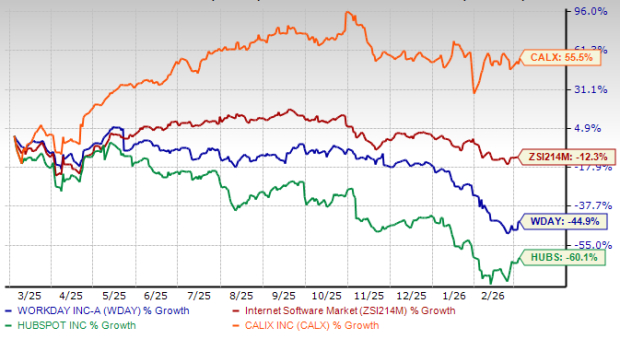

Price Performance

Workday has plummeted 44.9% over the past year compared with the industry’s decline of 12.3%. It has outperformed its peers like HubSpot, Inc. HUBS, but lagged Calix, Inc. CALX over this period. While HubSpot declined 60.1%, Calix is up 55.5% over the same period.

One-Year WDAY Stock Price Performance

Image Source: Zacks Investment Research

WDAY Diversifying to Ride Out the Storm

Workday is expanding its portfolio beyond core HCM solutions into the financial domain. It is customizing them for diverse industries and verticals, such as education, the public and financial services, among others. This has helped the company witness strong renewals and expand its customer base as business enterprises aim to consolidate spend and improve efficiency levels. Management is putting a strong focus on integrating advanced AI and ML capabilities. The ongoing AI-powered product development emphasizes natural language generation, content search, summarization, content augmentation and document understanding.

End Note

The portfolio diversification and focus on AI will likely help the company reap long-term benefits. Its diversified product portfolio continues to yield a steady flow of customers. It is also gaining traction in the international market.

However, the downtrend in estimate revisions portrays skepticism about the business model. Stiff competitive pressure and an uncertain geopolitical environment are headwinds for the company. High operating expenses remain an overhang as well. Consequently, it might be a prudent investment decision to avoid the stock at the moment.

Workday carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power, you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Calix, Inc (CALX): Free Stock Analysis Report

Workday, Inc. (WDAY): Free Stock Analysis Report

HubSpot, Inc. (HUBS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios