AvalonBay's Q3 2025 Core FFO Miss: A Misstep or a Buying Opportunity?

The Q3 Miss: Market Dynamics vs. Operational Slack

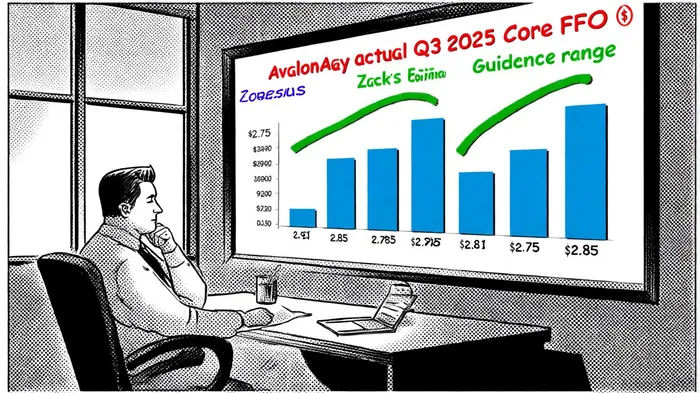

The shortfall was not due to a single factor but a confluence of macroeconomic and industry-specific headwinds. According to a U.S. News forecast, the U.S. apartment market saw a 0.3% decline in effective asking rents between July and September 2025, with high-growth markets like Denver and Phoenix experiencing steeper drops of 8% and 5%, respectively. AvalonBayAVB--, which operates heavily in these regions, faced a 6.2% average concession rate across 22% of its properties, dragging occupancy to 95.4% for the quarter (the U.S. News piece also highlights these market trends).

Rising operating expenses further pressured margins. Same-store residential operating costs increased year-over-year, a trend management attributes to inflationary pressures in labor and utilities, as noted in the U.S. News forecast. While AvalonBay maintained its Q3 guidance range, the result underscores the fragility of its business model in a cooling housing market.

Long-Term Fundamentals: A Mixed Picture

As noted in a MarketBeat filing, AvalonBay's balance sheet remains robust, with a debt-to-equity ratio of 0.71 and a market capitalization of $26.81 billion, giving the company the financial flexibility to weather cyclical downturns. Its 2025 full-year guidance of $11.15–$11.35 Core FFO per share, while conservative, reflects confidence in stabilizing same-store net operating income (NOI), which is projected to grow 2.2% year-over-year, according to a Nasdaq preview.

Strategic initiatives also suggest a focus on long-term value creation. AvalonBay has prioritized portfolio optimization, divesting non-core assets and reinvesting in high-growth markets. Additionally, its 3.7% dividend yield-supported by an annualized payout of $7.00-remains attractive in a rising interest rate environment (the MarketBeat filing details recent institutional trades). Institutional investors, however, are divided: Sumitomo Mitsui Trust Group Inc. increased its stake by 1.5%, while Nisa Investment Advisors LLC cut holdings by 19.4%, signaling cautious optimism and skepticism (these ownership moves were reported in the MarketBeat filing).

Management's Outlook: Navigating Uncertainty

AvalonBay's management has acknowledged the challenges but emphasized resilience. In its Q3 2025 earnings update, the company noted that it maintained occupancy above 96% in its core markets and expects modest rent growth in select regions like Boston and San Francisco (this was highlighted in the MarketBeat alert). However, elevated interest expenses-projected to rise 13.8% year-over-year-remain a drag on profitability, a point also raised in the Nasdaq preview.

The Zacks Rank of 4 (Sell) and a history of negative earnings surprises over the past four quarters add to investor caution, a trend discussed in the U.S. News forecast. Yet, AvalonBay's updated full-year guidance and dividend discipline suggest a commitment to shareholder returns, even amid a difficult operating environment.

Is This a Buying Opportunity?

The Q3 miss is a red flag, but not a death knell. For long-term investors, AvalonBay's strong balance sheet, strategic focus on high-growth markets, and defensive dividend yield could outweigh the near-term risks. However, the company's exposure to overbuilt apartment markets and rising costs means the path to recovery is far from guaranteed.

Investors should monitor two key metrics in the coming quarters: 1) the pace of rent stabilization in high-growth markets, and 2) AvalonBay's ability to control operating expenses without sacrificing occupancy. If the company can navigate these challenges, its discounted valuation-trading at a 12% discount to its 52-week high-may present an attractive entry point. For now, patience and a close watch on same-store NOI trends are warranted.

Comentarios

Aún no hay comentarios