Australia's Credit Growth Signals Resilience Amid Global Uncertainties

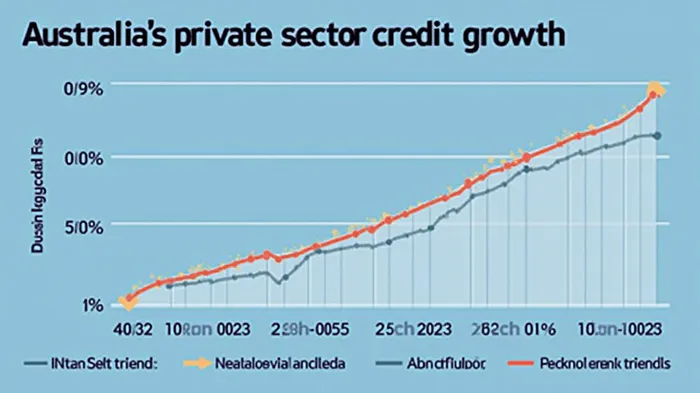

Australia’s credit markets delivered a resilient performance in March 2025, with total private sector credit rising by 0.5% month-over-month and annual growth hitting 6.5%—the strongest pace since April 2023. This growth, driven by surging demand for housing and personal loans, underscores a nuanced economic landscape where household borrowing remains robust despite broader financial headwinds. However, slowing business credit and lingering global trade risks suggest investors must tread carefully.

Credit Growth: A Sectoral Divide

The March data revealed a clear split in borrowing patterns. Housing credit grew 0.5% month-over-month, while personal loans surged 0.6%—the fastest pace since late 2024. In contrast, business credit slowed to 0.3%, down from February’s 0.7%, signaling cautious corporate spending.

The annual 6.5% credit expansion reflects sustained momentum from late 2023, when growth stabilized at this rate. Projections suggest moderation to 4.0% by 2026, aligning with historical averages of 10.26% annual growth since 1977.

Economic Context: Growth Amid Restraints

Australia’s economy expanded 0.6% in the December 2024 quarter, with annual GDP growth of 1.3%—driven by domestic consumption and net exports. Favorable terms of trade, boosted by rising export prices for minerals and liquefied natural gas (LNG), supported this resilience.

However, household debt-servicing costs remain elevated, with the cash rate above neutral estimates. Despite this, inflation held steady at 2.4%, within the Reserve Bank of Australia’s (RBA) target range. Markets now price in a 25 basis-point rate cut by early 2025, which could ease borrowing pressures and bolster credit demand.

Risks and Challenges

- Global Trade Uncertainty: U.S. trade policies and China’s economic slowdown have caused a 5% depreciation of the Australian dollar since November 2024, complicating export competitiveness.

- Corporate Caution: Business credit growth slowed in March, reflecting uncertainty over domestic demand and global supply chains. Sectors like construction face headwinds from labor shortages and rising costs.

- Household Debt: While consumer credit hit a record $2.36 trillion in March, household savings remain low (3.8% of income), leaving households vulnerable to income shocks.

Investment Implications

- Housing and Consumer Lending: Strong demand for mortgages and personal loans suggests opportunities in banks with robust retail lending exposure, such as Commonwealth Bank (CBA) or Westpac (WBC).

- Resource Sectors: The mining and energy sectors, benefiting from high export prices, could sustain corporate credit growth. Investors might consider ETFs tracking the ASX 200 Materials Index.

- Rate Sensitivity: A potential RBA rate cut by early 2025 may favor equities over bonds.

Conclusion

Australia’s credit markets are navigating a delicate balance between sustained household borrowing and corporate caution. The 6.5% annual credit growth and 0.5% monthly rise in March highlight underlying demand resilience, particularly in housing and personal finance. However, risks such as a weakening Australian dollar and slowing business investment demand vigilance.

Investors should prioritize sectors directly tied to export-driven industries and banks with strong consumer lending portfolios. While projections indicate a moderation to 4.0% annual credit growth by 2026, the current trajectory suggests Australia’s economy remains resilient—if uneven—in the face of global turbulence.

As the RBA weighs rate cuts against inflation risks, the coming quarters will test whether this credit momentum can translate into broader economic stability. For now, the data paints a picture of cautious optimism, anchored in household spending but tempered by corporate restraint.

Comentarios

Aún no hay comentarios