Auric Mining (ASX:AWJ): A High-EPS-Growth Opportunity in a Rising Gold Sector

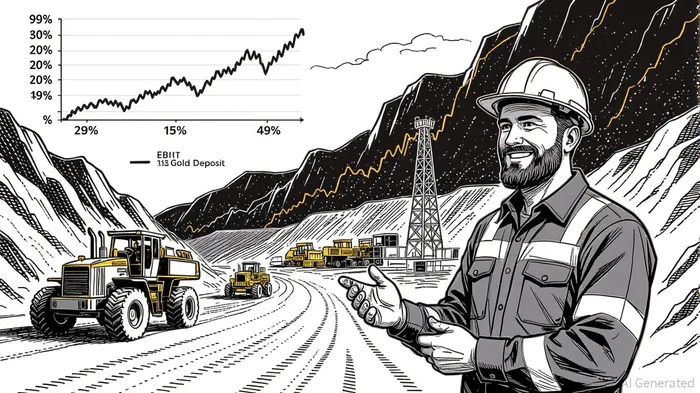

Auric Mining (ASX:AWJ) has emerged as a standout performer in the junior gold sector, driven by a combination of operational excellence, strategic resource expansion, and favorable market dynamics. Over the past 12 months, the company's EBIT margin has surged from 29% to 49%, a transformation fueled by record gold prices and cost discipline at its flagship Jeffreys Find Gold Mine. This margin expansion, coupled with a clear roadmap for resource growth and capital efficiency, positions Auric as a compelling candidate for investors seeking high-earnings-per-share (EPS) growth in a rising gold environment.

Operational Efficiency and EBIT Margin Expansion

Auric's EBIT margin expansion is a direct result of its ability to capitalize on elevated gold prices while maintaining tight cost controls. By February 2025, the Jeffreys Find Gold Mine had generated over $100 million in gold sales, with gold sold at an average price of A$4,024 per ounce—nearly 55% above the initial estimate of A$2,600 per ounce[1]. This pricing power, combined with a joint venture structure that ensures surplus cash is distributed only after all costs are paid, has amplified profitability. For instance, Stage Two of the project alone delivered $8.1 million in interim cash distributions, with an additional $3–$4 million expected as the remaining gold is sold[1].

The company's operational efficiency is further underscored by its ability to extract 17,900 ounces of gold from Stage Two mining, with 60,000 tonnes of material still slated for processing[1]. This output, achieved at a low-cost, high-grade asset, has directly contributed to the 49% EBIT margin reported in early 2025[2]. Analysts attribute this performance to Auric's lean management structure and its focus on low-capital, high-margin projects[2].

Strategic Positioning and Resource Expansion

Auric's strategic vision extends beyond Jeffreys Find, with the Munda Gold Project representing a pivotal next phase. The company has transitioned to independent operations at Munda, a 100%-owned asset with an Indicated & Inferred Resource of 145,000 ounces of gold at a grade of 1.23 g/t[1]. At current gold prices, Munda is projected to generate up to $15.5 million in surplus, with Auric retaining 100% of the profits—a stark contrast to the joint venture model at Jeffreys Find[1]. This shift to full ownership enhances both margin visibility and EPS potential.

To accelerate development, Auric has secured a $6.66 million capital raise[3], enabling the acquisition of the Burbanks Gold Facility and the Lindsay's Gold Project. These assets, located in Western Australia's gold-rich Coolgardie region, provide critical infrastructure for processing and production scaling. The Burbanks acquisition, in particular, adds a fully permitted gold processing plant, reducing capital expenditures and expediting time-to-market for Munda's output[3].

EPS Growth Drivers and Financial Strength

Auric's financial trajectory is equally compelling. In 2024, the company reported a $4.1 million profit before tax—a 212% year-on-year increase[4]—demonstrating its transition from a development-stage explorer to a cash-generative producer. This profitability, combined with a robust balance sheet (bolstered by $13 million in net proceeds from Jeffreys Find[1]), provides a strong foundation for reinvestment and shareholder returns.

Looking ahead, Auric's EPS growth is underpinned by three key factors:

1. Gold Price Tailwinds: With gold trading near record highs and central banks increasing purchases, Auric's all-in-sustaining-cost (AISC) model ensures margin expansion as prices rise[1].

2. Production Scaling: The Munda Gold Deposit is expected to contribute meaningfully to 2025 and 2026 earnings, with early production anticipated to add $3–$4 million in incremental cash flow[1].

3. Capital Efficiency: The recent $6.66 million raise[3] has de-risked project timelines, allowing Auric to avoid dilutive financing and maintain a high proportion of equity ownership.

Conclusion: A High-Margin, High-Growth Play

Auric Mining's combination of operational discipline, strategic acquisitions, and exposure to rising gold prices creates a rare value proposition in the junior mining sector. The company's EBIT margin expansion from 29% to 49% over 12 months is not an anomaly but a reflection of its ability to execute in a high-cost environment. As it transitions to full ownership of Munda and leverages its newly acquired infrastructure, Auric is well-positioned to deliver outsized EPS growth—a critical metric for investors prioritizing capital appreciation in a volatile market.

For those seeking a high-margin, junior gold producer with clear catalysts and a track record of execution, Auric Mining represents a compelling opportunity.

Comentarios

Aún no hay comentarios