Atebimetinib + mGnP in Pancreatic Cancer: How Phase 2a OS Data Could Reshape Biotech Valuation and M&A Dynamics

In the high-stakes arena of oncology drug development, phase 2a trials often serve as the first glimpse into a therapy's potential to disrupt the market. For ImmuneeringIMRX-- Corporation's Atebimetinib in combination with modified gemcitabine/nab-paclitaxel (mGnP) for first-line pancreatic cancer, the latest phase 2a data has not only exceeded expectations but also positioned the asset as a prime candidate for valuation surges and M&A activity. With 94% overall survival (OS) at six months and 86% at nine months—far outpacing historical benchmarks—this trial underscores the transformative power of robust clinical outcomes in driving investor sentiment and strategic interest.

Atebimetinib + mGnP: Redefining Survival Benchmarks

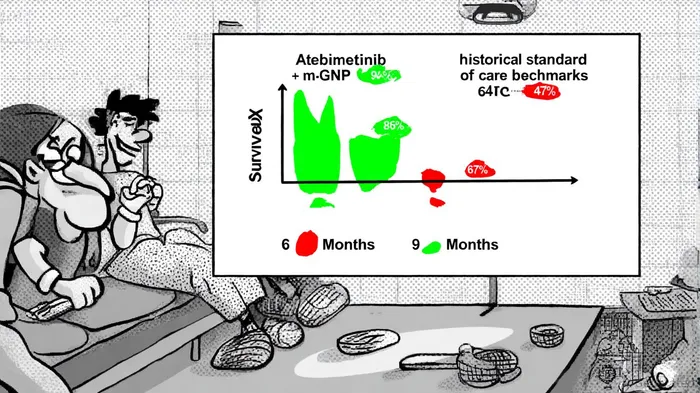

The phase 2a trial of Atebimetinib + mGnP has delivered results that defy the grim prognosis typically associated with pancreatic cancer. At six months, the 94% OS rate surpasses the 67% benchmark set by the MPACT trial's standard-of-care regimen (gemcitabine/nab-paclitaxel) [1]. By nine months, the OS rate of 86% remains significantly higher than the historical 47% for standard care [2]. Progression-free survival (PFS) also shows marked improvement, with 72% at six months and 53% at nine months, compared to 44% and 29% for conventional therapies [3]. These outcomes are further bolstered by a high disease control rate (81%) and an overall response rate (39%), with some patients achieving undetectable lesions [4].

The tolerability profile adds to the therapy's appeal. While grade 3+ adverse events such as anemia (18%) and neutropenia (15%) were observed, no grade 5 toxicities were reported, and the safety profile was deemed favorable relative to existing options [5]. This combination of efficacy and safety has already triggered a 400% surge in Immuneering's stock price over six months [6], illustrating how phase 2a data can catalyze immediate market reactions.

Historical Precedents: OS Data as a M&A Catalyst

The market-moving potential of phase 2a OS data is not unique to Atebimetinib. Historical case studies reveal a clear pattern: therapies demonstrating survival improvements in pancreatic cancer often attract M&A interest. For instance, OSE Immunotherapeutics' Tedopi, a therapeutic vaccine, reported a 65% 12-month OS rate in a phase 2 trial, sparking discussions about its potential as a neo-epitope-based treatment and elevating the company's valuation [7]. Similarly, Purple Biotech's CM24, an anti-CEACAM1 antibody, showed a 2.1-month OS extension in metastatic pancreatic cancer, leading to a 2024 acquisition that underscored the sector's appetite for differentiated assets [8].

These precedents highlight a broader trend: biotech valuations are increasingly tied to clinical milestones, particularly in areas with unmet medical needs like pancreatic cancer. According to a 2025 McKinsey report, later-stage assets in oncology commanded premium valuations, with pancreatic cancer therapies showing the highest potential due to their ability to address a $10 billion market [9]. Atebimetinib's data aligns with this trajectory, offering a compelling case for both standalone valuation growth and acquisition interest.

Valuation Multiples and the Road to Pivotal Trials

Biotech valuation multiples in 2025 have been driven by future potential, with companies leveraging clinical success to command higher price tags. For example, therapies with strong phase 2a OS data have historically traded at 12–15x revenue multiples, compared to 6–8x for earlier-stage assets [10]. Atebimetinib's performance could push Immuneering into the upper end of this range, especially as the company prepares for a pivotal phase 3 trial. Regulatory feedback on trial design is expected by Q4 2025, with dosing slated for mid-2026 [11]. Such milestones are critical for de-risking the asset and attracting larger pharma partners.

The broader biopharma M&A landscape also favors Immuneering's trajectory. In 2024, deals like Novartis' $2.9 billion acquisition of MorphoSys and AstraZeneca's $2.4 billion purchase of Fusion Pharmaceuticals demonstrated a preference for assets with late-stage clinical data [12]. With pancreatic cancer therapies commanding a 20–30% premium in M&A deals due to their high unmet need [13], Atebimetinib's phase 2a results position it as a strategic acquisition target for companies seeking to bolster their oncology pipelines.

Conclusion: Atebimetinib as a Market Disruptor

The phase 2a data for Atebimetinib + mGnP represents more than a clinical breakthrough—it is a catalyst for redefining pancreatic cancer treatment and reshaping biotech valuation dynamics. By outperforming historical benchmarks and demonstrating a favorable safety profile, the therapy has already triggered investor enthusiasm and set the stage for a pivotal trial. Historical precedents, from Tedopi to CM24, suggest that such data can drive valuation multiples and M&A activity, particularly in a sector where survival improvements are rare. As Immuneering advances toward phase 3, the asset's potential to become a new standard of care—and a lucrative acquisition target—remains a compelling story for investors and industry players alike.

Comentarios

Aún no hay comentarios