Astrazeneca's Underperformance Relative to the Market: A Case for Value Re-Rating Amid Strategic Reinvention

AstraZeneca (AZN) has underperformed relative to broader market indices in 2025, despite a robust pipeline and disciplined cost management. This divergence presents a compelling case for value re-rating, driven by strategic shifts in R&D and operational efficiency. By analyzing the company's evolving business model, valuation metrics, and peer comparisons, investors can assess whether the market is underappreciating its long-term potential.

Strategic Reinvention: R&D as a Growth Engine

AstraZeneca's 2025 R&D strategy is anchored in innovation, with a focus on transformative therapies such as antibody-drug conjugates (ADCs), radioconjugates, and gene therapy. The company aims to launch 20 new medicines by 2030, targeting oncology, respiratory, and rare diseases[4]. This ambition is supported by a pipeline of 196 R&D programs, including 19 new molecular entities (NMEs) in late-stage development[4]. Analysts highlight that seven of these NMEs are poised for Phase III readouts in 2025, including pivotal trials like DESTINY-Breast09 and MATTERHORN, which could redefine cancer treatment paradigms[3].

The company's oncology segment, contributing 43% of total revenue, is a key growth driver. Flagship drugs like Tagrisso, Imfinzi, and Enhertu are protected by patents extending into the 2030s, mitigating near-term revenue erosion[4]. Furthermore, AstraZenecaAZN-- is expanding into high-growth areas such as obesity treatments and gene therapy, diversifying its therapeutic footprint and reducing reliance on any single product line[4].

Cost-Cutting and Financial Discipline

AstraZeneca's 2024–2025 cost-cutting measures have bolstered profitability without compromising innovation. The company achieved an 80% gross profit margin in Q4 2024, reflecting efficient cost management[4]. This operational discipline translated into 5% year-over-year revenue growth and 6% earnings per share (EPS) growth, outpacing many peers[4]. A debt-to-equity ratio of 0.75 underscores its balanced capital structure, while free cash flow reached $5 billion, providing flexibility for R&D and shareholder returns[4].

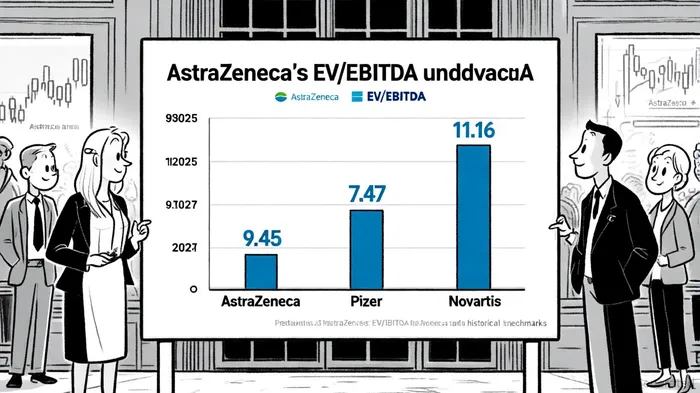

These efforts have improved valuation metrics. AstraZeneca's EV/EBITDA ratio stands at 9.45, significantly below its 5-year average of 12.19[1]. Meanwhile, its forward P/E ratio of 18–20 exceeds both Pfizer's (~8.3) and Novartis's (~12.7), suggesting the market is discounting its growth prospects[4]. This discrepancy may reflect skepticism about its R&D pipeline or short-term challenges, such as ongoing investigations in China[3].

Undervaluation and Re-Rating Potential

AstraZeneca's valuation appears attractive when compared to industry peers. While its EV/EBITDA of 9.45 lags behind Novartis's 11.16[3], it outperforms Pfizer's 7.47[5]. This suggests the market is pricing AstraZeneca closer to a mid-tier innovator than a top-tier growth stock, despite its ambitious revenue target of $80 billion by 2030[4]. Analysts argue that the company's “catalyst-rich” 2025—driven by Phase III trials and new molecule approvals—could catalyze a re-rating[3].

Moreover, AstraZeneca's strategic investments in AI-driven drug discovery and real-world data analytics are streamlining R&D, reducing costs, and accelerating time-to-market[3]. These innovations position the company to capitalize on the $1.2 trillion global pharma market, where demand for novel therapies is surging[4].

Risks and Mitigants

While AstraZeneca's long-term prospects are strong, near-term risks persist. Regulatory scrutiny in China and potential delays in ADC development could pressure revenue[3]. However, the company's $3.5 billion investment in U.S. R&D and manufacturing[5] and geographic diversification are mitigating these risks. Additionally, its robust cash flow generation provides a buffer against volatility.

Conclusion: A Case for Re-Rating

AstraZeneca's underperformance relative to the market appears to be a temporary dislocation rather than a reflection of its intrinsic value. With a $226.78 billion market cap and a forward P/E of 15.20[2], the stock is trading at a discount to its growth trajectory. As the company executes on its 2030 vision—driven by innovation, cost discipline, and strategic diversification—investors may soon witness a re-rating that aligns its valuation with its industry-leading potential.

Comentarios

Aún no hay comentarios