Assured Guaranty's Financial Resilience: A Deep Dive into Balance Sheet Strength and Risk-Adjusted Returns

In the high-stakes world of bond insurance, Assured Guaranty Ltd.AGO-- (AGO) has long been a paragon of stability. Yet, as sustained premium declines challenge its top-line growth, investors must ask: Can AGO's financial resilience withstand prolonged pressure? The answer lies in its balance sheet fortitude, conservative leverage, and a track record of navigating market stress with discipline.

Balance Sheet Strength: A Fortress of Liquidity and Conservative Leverage

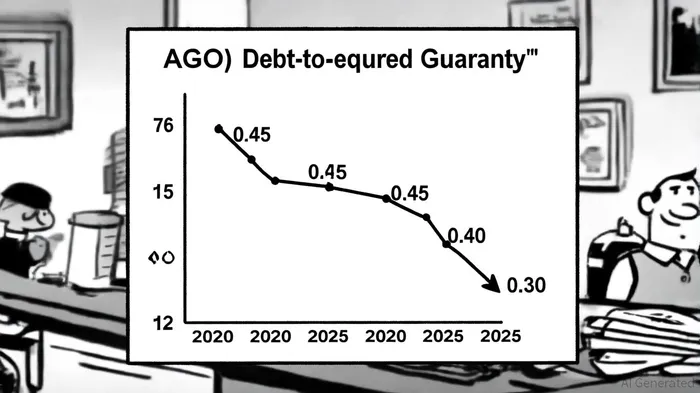

AGO's financial position in Q3 2025 reveals a company prioritizing prudence over aggressive expansion. Total assets stood at $12.10 billion, with liabilities at $6.37 billion, yielding a debt-to-equity ratio of 0.30-a figure that underscores its conservative capital structure[4]. This metric, calculated as total debt divided by shareholder equity, places AGO in a favorable position compared to its peers, who often operate with higher leverage in pursuit of growth[1].

The company's Asset Resilience Ratio-a measure of liquid assets (cash and short-term investments) as a percentage of total assets-fell to 15.30% in June 2025 from 19.70% in December 2024[2]. While this decline may raise eyebrows, it still positions AGO ahead of many insurers, which typically maintain resilience ratios below 10%. The reduction likely reflects strategic reinvestment in higher-yielding assets, a calculated trade-off to balance liquidity with returns in a low-interest-rate environment.

AGO's leverage management further reinforces its stability. Over the past six years, the company has maintained a leverage score of 3.90/5, outperforming the sector median[4]. This conservative approach is critical in an industry where over-leveraging can amplify losses during downturns.

Credit Ratings: A Vote of Confidence from Global Agencies

AGO's fortress balance sheet is mirrored in its stellar credit ratings, a cornerstone of its risk-adjusted returns. As of 2025, S&P Global Ratings affirmed AGO's AA financial strength rating with a stable outlook, noting that its capital adequacy exceeds the 'AAA' stress level[2]. Moody's and Fitch similarly assigned A1 and AA+ ratings, respectively, reflecting confidence in AGO's ability to absorb shocks[1].

These ratings are not mere formalities-they directly impact AGO's cost of capital and its capacity to underwrite risk. For instance, during the 2008 financial crisis, AGO reported a net income of $68.9 million in 2008 (after a $303.3 million loss in 2007), thanks to unrealized gains on credit derivatives and disciplined loss management[5]. Similarly, during the 2020 pandemic, AGO adapted swiftly to surging demand for bond insurance, maintaining strict underwriting standards while expanding into secondary markets[3].

Historical Performance: Stress-Tested Resilience

AGO's ability to thrive amid chaos is its true testament. In 2008, it navigated the collapse of mortgage-backed securities by absorbing $260 million in increased losses but still delivering positive net income[5]. During the 2020 pandemic, when public finance issuance halted, AGO pivoted to international infrastructure opportunities and secondary-market business, ensuring continuity in revenue streams[3].

This adaptability is embedded in its capital management practices. In Q2 2025, despite a 37.5% year-over-year drop in adjusted operating income (to $50 million), AGO returned $150 million to shareholders via dividends and share repurchases[1]. It further authorized an additional $300 million for buybacks, signaling confidence in its capital position. Such actions highlight AGO's commitment to rewarding shareholders even during periods of operational contraction.

Long-Term Risk-Adjusted Returns: A Calculated Proposition

While AGO's Return on Equity (ROE) of 0.40/5 lags behind its leverage metrics[4], this weakness is offset by its low-risk profile. In a market where volatility is the norm, AGO's focus on capital preservation and steady returns aligns with long-term risk-adjusted return goals. Its credit ratings, conservative leverage, and historical resilience during crises collectively suggest that AGO is more likely to outperform in downturns than in booms-a critical trait for defensive investors.

Moreover, AGO's recent share repurchase authorizations and strategic reinvestment of liquid assets indicate a proactive approach to capital optimization. These moves, coupled with its ability to maintain profitability during stress events, position it as a compelling long-term holding for portfolios prioritizing stability over speculative growth.

Conclusion

Assured Guaranty's financial resilience is not a product of luck but a result of disciplined capital management, conservative leverage, and a history of navigating crises with agility. While declining premiums pose a near-term challenge, AGO's fortress balance sheet and top-tier credit ratings provide a buffer against volatility. For investors seeking risk-adjusted returns in uncertain markets, AGO exemplifies the value of a company built to endure-not just thrive.

Comentarios

Aún no hay comentarios