Assessing the Strategic Value of European Defense and Security Firms Amid Geopolitical Uncertainty

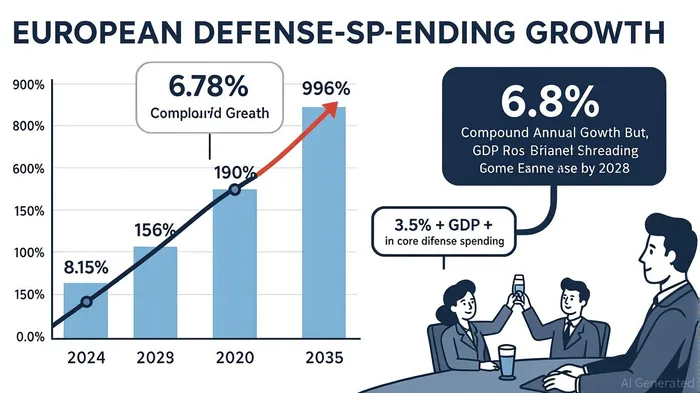

Geopolitical uncertainty has long been a double-edged sword for economies: it disrupts trade and investment but also spurs innovation and industrial retooling. In Europe, the invasion of Ukraine and the subsequent realignment of NATO have transformed defense spending from a political talking point into a structural economic force. According to a report by the European Commission, defense budgets across the continent are projected to grow at a compound annual rate of 6.8% from 2024 to 2035, outpacing the U.S., Russia, and China. This surge is not merely a reaction to immediate threats but a calculated shift toward strategic autonomy, with institutional investors increasingly viewing European defense infrastructure as a long-term asset class.

The Fiscal Catalyst: From Readiness 2030 to Industrial Revival

The European Union's Readiness 2030 initiative, which aims to raise defense spending to 1.5% of GDP by 2028, has been a pivotal catalyst. Backed by a €150 billion loan instrument, the program enables member states to procure critical systems like air defense and naval platforms. Germany, the bloc's largest economy, has committed to meeting the 3.5% core defense spending threshold by 2029, with a 2025 budget of $110 billion. This fiscal stimulus is not confined to military hardware; it is reshaping industrial ecosystems. For instance, Volkswagen's Osnabrück plant is being repurposed for defense production, signaling a broader trend of dual-use technologies—systems with both civilian and military applications—driving industrial revitalization.

The economic impact of this spending is already evident. Data from the European Central Bank indicates that increased defense and infrastructure investment could add 0.2–0.4 percentage points to euro-area GDP growth in 2025–2026. This growth is underpinned by a shift in institutional capital flows. Funds like the WisdomTreeWT-- Europe Defense Fund (WDEF) have positioned themselves to capture the “defense supercycle,” with European defense spending expected to account for 22% of global defense expenditures by 2030.

ESG Dilemmas: Can Defense Be Sustainable?

The surge in defense investment has sparked a contentious debate within the ESG (Environmental, Social, Governance) community. Proponents argue that military capability supports peace and democratic governance, aligning with the “social” pillar of ESG. Critics, however, warn of “peace-washing”—the practice of greenwashing defense investments as socially responsible. This tension reflects a broader challenge: how to reconcile the necessity of deterrence with the ethical imperatives of sustainability. For now, the EU's Green Deal and REPowerEU initiatives suggest a pragmatic approach, integrating decarbonization goals into defense infrastructure projects.

Institutional Investment: A New Frontier

Institutional investors are recalibrating their portfolios to reflect the new reality. According to CitigroupC--, planned European infrastructure allocations are set to rise by 5–7% by 2026, partly funded by trimming U.S. exposure. This shift is driven by both regulatory clarity and the allure of high-growth sectors. For example, non-traditional defense firms in software, aerospace, and logistics are expected to attract €500 billion in investment from 2026 to 2029. The EU's SAFE instrument, which provides EU-backed loans for common procurements, further reduces risk for institutional investors.

The Road Ahead: Geopolitical Risk as a Perpetual Engine

While the immediate catalysts—Russia's war in Ukraine and NATO's expansion—are undeniable, the long-term drivers of European defense spending are more structural. The Joint White Paper for European Defence Readiness 2030 emphasizes research and development in AI, robotics, and cybersecurity, ensuring that defense spending remains a vehicle for technological leadership. As geopolitical tensions persist, institutional investors are likely to treat European defense infrastructure as a “perpetual engine” of growth, akin to the post-World War II industrial boom.

In conclusion, the strategic value of European defense and security firms lies not just in their ability to mitigate risk but in their capacity to transform it into opportunity. For investors, the key is to distinguish between short-term volatility and long-term structural trends—a task that requires both analytical rigor and geopolitical foresight.

Comentarios

Aún no hay comentarios