Assessing RiverNorth Flexible Municipal Income Fund's Dividend Appeal Amid 2025's Shifting Interest Rates and Tax-Advantaged Yields

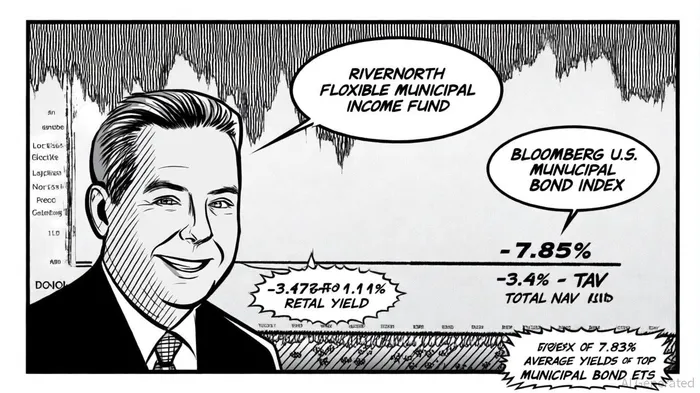

The RiverNorth FlexibleRFM-- Municipal Income Fund (RFM) has long positioned itself as a high-yield option for investors seeking tax-advantaged income. Its recent $0.094 monthly dividend, translating to a 7.83% annual yield as of October 2025, appears enticing in a market where municipal bond ETFs like the Vanguard Tax-Exempt Bond ETF (VTEB) and Invesco National AMT-Free Municipal Bond ETF (PZA) offer yields of 3.8% and 4.2%, respectively, according to the RFM dividend history. However, the fund's performance and structural risks-particularly in a shifting interest rate environment-demand closer scrutiny.

A High Yield, But at What Cost?

RFM's 7.83% yield outpaces the average of the top 25% of U.S. financial services sector dividend payers (7.42%), a gap that is also reflected in the RFMRFM-- dividend history. Yet this yield is built on a fragile foundation. Over the past year, the fund's dividend has contracted by 1.47%, according to CEFConnect, and its total return on net asset value (NAV) for the fiscal year ending June 30, 2025, was -3.45%, lagging behind the Bloomberg U.S. Municipal Bond Index's 1.11% return, per the RFM NAV report. The fund's market price total return was even worse at -7.16%, reflecting a 9.04% discount to NAV, according to the Municipal Bond Outlook.

This underperformance stems from a combination of leverage and high expenses. RFM employs 41.99% effective leverage to amplify returns, but this comes at a cost: management fees of 2.30% and interest expenses of 2.70%, as CEFConnect reports. These expenses, coupled with a $6.74 million unrealized depreciation on its portfolio noted in the RFM NAV report, have eroded returns. For investors, this raises a critical question: Is the fund's yield sustainable, or is it being propped up by return of capital or capital gains rather than net investment income, as the RFM NAV report suggests?

Historical backtesting of RFM's dividend announcements from 2022 to 2025 reveals limited predictive power. Only two of four dividend-related events fell within the valid price-history window, and cumulative abnormal returns remained within ±1.3% over a 30-day post-event horizon, with no statistically significant outperformance versus the benchmark. The backtest, conducted by the author using public price data and event-study methodology, showed that while the win rate improved to 50% after day 14, the magnitude of outperformance remained marginal and non-significant. This suggests that RFM's dividend announcements have not historically generated a tradable edge for investors, further complicating the case for relying on its yield as a reliable income source.

Interest Rates and Municipal Bonds: A Double-Edged Sword

The municipal bond market in 2025 is navigating a complex landscape. The Federal Reserve has signaled potential rate cuts in the second half of the year, which could benefit longer-duration municipal bonds as their prices rise, as noted in the Municipal Bond Outlook. However, RFM's portfolio is not immune to the volatility of this environment. Its focus on both municipal bonds and closed-end funds (CEFs) introduces dual exposure: while municipal bonds may gain from falling rates, CEFs are often sensitive to liquidity and discount compression, per the Schwab municipal outlook.

Moreover, the fund's leverage amplifies risk. In a rising rate scenario, the cost of borrowing increases, squeezing returns. Conversely, in a falling rate environment, the fund's fixed-rate debt could become more expensive relative to new, lower-cost financing. This duality underscores the need for active duration management-a challenge for RFM given its current underperformance.

Tax Advantages and Credit Fundamentals: A Silver Lining

Despite these risks, RFM's tax-exempt structure remains a compelling draw. The muni tax exemption, preserved by the "One Big Beautiful" tax bill, ensures that investors in high-tax states (e.g., New York, California) can access yields that are tax-equivalent to 7.3% for a 4% tax-exempt bond if the top federal tax rate returns to 39.6%, as discussed in the Municipal Bond Outlook. This makes RFM particularly attractive for those in higher tax brackets, though the fund's discount to NAV complicates the math.

Credit quality in the broader municipal market also remains robust, with 72% of bonds rated AAA/Aaa or AA/Aa-a level not seen in two decades, according to the Schwab municipal outlook. However, RFM's portfolio includes sectors like healthcare and higher education, which face fiscal headwinds noted in the Municipal Bond Outlook. While defaults remain rare (only 59 monetary defaults in a market of 37,000+ issuers through December 2024, per Schwab), investors must weigh the fund's exposure to these vulnerable sectors against its yield.

Conclusion: A High-Yield Gamble?

RFM's 7.83% yield is undeniably appealing, especially in a low-yield world. Yet its structural weaknesses-leverage, high expenses, and underperformance-pose significant risks. For investors willing to tolerate volatility and prioritize tax-advantaged income, RFM could be a viable option, particularly if the Federal Reserve's rate cuts boost municipal bond prices. However, the fund's discount to NAV and its reliance on non-income sources for dividends suggest caution.

In the shifting 2025 landscape, RFM exemplifies the trade-offs inherent in high-yield municipal strategies. While its dividend offers a compelling headline, investors must scrutinize the sustainability of that yield and the fund's ability to navigate a market where credit dispersion and interest rate volatility are likely to persist.

Comentarios

Aún no hay comentarios