Assessing the Long-Term Viability of the Nuclear Energy Sector Amid Cooling Enthusiasm

The nuclear energy sector, once heralded as a cornerstone of the clean energy transition, now faces a reckoning. While its market size stood at $35.42 billion in Q3 2025, growing at a modest 2.3% compound annual rate to $44.38 billion by 2035, according to a Business Research Insights report, the sector has experienced a contraction in 2024, with an annual growth rate of -3.19%, per a StartUs Insights report. This cooling enthusiasm raises critical questions about its long-term viability, particularly when evaluated through the lenses of valuation metrics and risk-adjusted returns.

Valuation Metrics: A Tale of Two Trajectories

The nuclear sector's valuation multiples tell a mixed story. In 2025, the EV/EBITDA multiple for nuclear energy reached 61.4x, a stark contrast to the broader "Utilities" sector's weighted average of -142.14x, per Multiples.vc data. However, this high valuation is not uniformly applied. For instance, Nano Nuclear EnergyNNE-- (NNE) reported a negative EBITDA of -$26.1 million and a net loss of -$43.9 million in 2025, per MarketScreener, while companies like Constellation EnergyCEG-- (CEG) outperformed expectations, with revenue exceeding forecasts by $1.2 billion, according to a MarketBeat analysis. This divergence underscores the sector's fragmentation: innovators in small modular reactors (SMRs) and advanced designs attract investment, but legacy firms struggle with profitability.

However, historical backtesting of CEG's earnings beats since 2022 reveals mixed signals for investors. While the stock has occasionally outperformed expectations, the average cumulative excess return relative to the S&P 500 peaks at around +4 percentage points by day 15 but fades thereafter, with no statistically significant outperformance across most horizons-the MarketBeat analysis shows this pattern. Directional hit rates also fluctuate-below 50% in the first week, improving to 80% between days 12–19, then settling to 60% by day 30-suggesting that earnings beats alone are not a reliable short-term catalyst, as noted in the MarketBeat analysis.

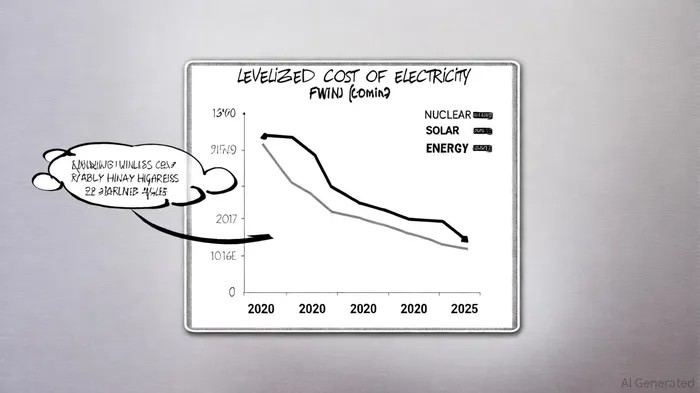

Comparatively, renewables have leveraged declining costs to secure investor confidence. The Levelized Cost of Electricity (LCOE) for solar photovoltaics is projected to drop from $55/MWh in 2023 to $25/MWh by 2050, per a Forbes analysis, dwarfing nuclear's stable but higher LCOE of $110/MWh, according to a Forbes piece. This cost gap, coupled with renewables' shorter deployment timelines, has skewed capital flows. By 2025, global investment in renewables reached $780 billion, per a Visual Capitalist chart, far outpacing nuclear's $80 billion, according to the IEA report.

Risk-Adjusted Returns: Navigating Volatility and Dividend Yields

Risk-adjusted returns further complicate the nuclear sector's appeal. The VanEck Vectors Uranium+Nuclear Energy ETF (NLR) demonstrated a Sharpe ratio of 1.62 over the past year, per PortfoliosLab data, outperforming many traditional energy assets. However, individual stocks like NNENNE-- lagged, with a Sharpe ratio of 0.20 on the PortfoliosLab NNE page, reflecting their volatility and unprofitability. In contrast, renewable energy firms such as Brookfield Renewable Partners offer dividend yields of 5.49%, according to a Motley Fool list, significantly higher than nuclear's Utilities sector average of 3.54%, per Siblis Research data.

Fossil fuels, though increasingly scrutinized, maintain a unique position. Their lower LCOE-$56/MWh for natural gas and $70/MWh for coal in 2024-is highlighted in a PlanetaryPL analysis, and their established infrastructure provides returns with lower perceived risk, despite regulatory headwinds. Yet, their Sharpe ratios remain unmeasured in the provided data, highlighting a gap in comparative analysis.

Macroeconomic and Regulatory Headwinds

The sector's challenges extend beyond financial metrics. Regulatory risks loom large: the U.S. Nuclear Regulatory Commission's (NRC) Standard Design Approval for NuScale's 77 MWe reactor is a rare bright spot in an otherwise slow approval process, noted in a Callan guide. Geopolitical tensions, such as the Russia-Ukraine war, have also disrupted uranium supply chains, according to the IEA review, while public opposition to nuclear waste management persists.

Conversely, macroeconomic factors like inflation and interest rates amplify the sector's capital intensity. With nuclear projects averaging $8,765–$14,400 per kilowatt in 2024, as reported in the Forbes piece, high borrowing costs deter new entrants. Meanwhile, renewables benefit from declining technology costs and policy tailwinds, such as the Inflation Reduction Act's tax credits, discussed in an IEA analysis.

Conclusion: A Sector at a Crossroads

The nuclear energy sector's long-term viability hinges on its ability to reconcile high capital costs with technological innovation. While SMRs and advanced reactor designs offer scalable solutions, as highlighted in a PortfoliosLab portfolio, their commercialization remains unproven at scale. Institutional investors are cautiously optimistic, as evidenced by the U.S. DOE's $1.2 billion investment in advanced reactors, reported by Business Research Insights, but this pales against the $546 billion China allocated to renewables in 2022 (per the Visual Capitalist chart).

For nuclear to reclaim its place in the energy transition, it must demonstrate not only technical feasibility but also financial resilience. Until then, the sector will remain a high-risk, high-reward proposition-competing not just with renewables, but with its own historical inertia.

Comentarios

Aún no hay comentarios