Assessing the iShares 4% Bond ETF for Retirees: A Value Investor's View

The iShares iBonds Dec 2026 Term Corporate ETF (IBDR) operates on a fundamentally different principle than the perpetual bond funds that dominate the market. This is a finite asset, designed to liquidate and return principal to shareholders in December 2026. Unlike traditional bond ETFs that constantly buy and sell holdings, IBDRIBDR-- holds its portfolio of corporate bonds until each one matures. This structure mimics owning individual bonds, providing a clear endpoint and a predictable return of capital, which is a critical feature for retirees planning their cash flows.

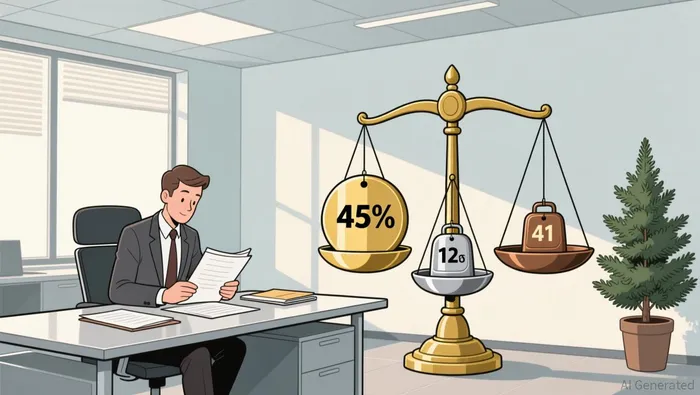

The fund's current yield is 4.12%, supported by a conservative portfolio of investment-grade bonds. Its credit breakdown shows a focus on quality, with 45% A-rated, 41% BBB-rated, and 12% AA-rated securities. This high-quality mix, combined with the fact that bonds are approaching maturity, typically reduces default risk as companies prioritize debt repayment. The fund has delivered consistent monthly distributions, averaging $0.084 per share throughout 2025, translating to roughly $1.01 in annual income.

From a cost perspective, IBDR is efficient, with a 0.10% expense ratio. This low fee, which costs just $10 annually per $10,000 invested, is a notable advantage. The fund's structure also leads to low portfolio turnover, minimizing taxable events for investors. Its 5-year price volatility has been remarkably low, trading in a tight range that underscores its stability-a key trait for preserving principal in retirement.

The investment thesis here is straightforward: safety depends on credit quality and the absence of defaults before the December 2026 maturity. The fund's finite lifespan is not a flaw but the core of its design. Investors know exactly when their principal will be returned, allowing them to plan for reinvestment. As the market faces a wave of maturing fixed income assets, IBDR offers a disciplined, low-cost vehicle to capture a defined yield with a clear exit strategy.

Evaluating the Margin of Safety: Credit Quality and Interest Rate Risk

For a value investor, the core question is always about the margin of safety. With IBDR, this safety is built on two pillars: exceptional credit quality and negligible interest rate exposure. The fund's portfolio is overwhelmingly composed of investment-grade bonds, with 98% classified as such. The specific breakdown shows a conservative mix: 45% A-rated, 12% AA-rated, and 41% BBB-rated securities. This concentration in high-quality debt is the first line of defense. The primary credit risk here is the BBB segment, which represents the largest single bucket. However, the fund's structure mitigates this risk significantly. As bonds approach their December 2026 maturity, companies have a strong incentive to meet their obligations, which typically improves credit quality and reduces default risk. This is the essence of a margin of safety-investing in assets where the downside is capped by the quality of the underlying issuers.

The second pillar is interest rate risk, which is effectively zero. With less than one year until maturity for its entire portfolio, the fund's duration is minimal. This means the value of the underlying bonds is not sensitive to changes in prevailing interest rates. The fund's design ensures that the principal will be returned at a known date, regardless of what happens in the broader bond market. This is a stark contrast to long-duration bond funds, which can see significant capital volatility from rate swings. For a retiree, this stability is paramount. It guarantees that the income stream and the return of principal are not subject to the whims of monetary policy.

This combination of high credit quality and minimal interest rate exposure translates directly into the fund's remarkable price stability. Over the past five years, IBDR has exhibited just 5.3% total variation in its share price, trading in a tight range. This low volatility is a tangible measure of the margin of safety in action. It shows that the market has priced in the fund's predictable cash flows and minimal risks. The result is a vehicle where the investor's capital is protected, and the yield is captured without meaningful capital loss, as demonstrated by its 1-year total return of 4.99%.

The bottom line is that IBDR's safety is not theoretical. It is a product of its finite, target-maturity structure, which forces a portfolio of high-quality, soon-to-mature bonds. This setup creates a wide moat against both credit and interest rate shocks, providing the kind of stable, predictable return that aligns with a retiree's need for principal preservation.

The Path to Principal Return and Reinvestment Risk

The mechanics of IBDR's principal return are straightforward and its structure provides a clear advantage over holding individual bonds. Because the fund is designed to liquidate in December 2026, it holds its portfolio of corporate bonds until each one matures. This eliminates the need for active management and the reinvestment risk that plagues traditional bond funds. For the income stream, the fund's monthly distributions are backed by the coupon payments of these bonds. Since the portfolio is fixed and held to maturity, there is no risk that the fund will be forced to reinvest those cash flows at lower prevailing rates. The retiree's income is locked in for the life of the fund.

However, this structure also means the portfolio's credit quality is locked in. The fund's safety depends entirely on the issuers of the bonds it currently holds. The primary risk to principal is not interest rate swings, but rather credit deterioration or default among these corporate issuers before their December 2026 maturity. The fund's investment-grade focus and the fact that companies have a strong incentive to repay debt as it nears maturity provide a margin of safety. Yet, the BBB segment, which makes up 41% of the portfolio, represents the most significant credit exposure. If a company in that bucket defaults, the principal returned to shareholders would be less than the initial investment.

For a retiree, IBDR offers a direct, low-cost alternative to constructing and managing a personal bond ladder. It provides instant diversification across hundreds of corporate issuers through a single ticker, which is difficult and expensive to replicate with individual bonds. It also offers superior liquidity compared to holding individual bonds, which can be harder to sell quickly without a price concession. The fund's 0.10% expense ratio and low turnover further enhance its appeal as a passive vehicle.

The bottom line is that IBDR trades one set of risks for another. It removes the uncertainty of reinvestment and interest rate volatility, but it concentrates the credit risk of its current portfolio. For a retiree seeking a predictable, stable income stream with a defined end date, this trade-off is often acceptable. The fund delivers the safety of a bond ladder without the hassle of managing it, making it a disciplined tool for a specific phase of retirement planning.

Valuation, Alternatives, and the Broader Portfolio Context

The final piece of the puzzle is assessing IBDR's value relative to its promised outcome and its place in a retiree's broader plan. The fund's current price is not a guarantee of a $1.00 return at maturity. The final distribution will be the sum of principal returned from maturing bonds minus any defaults or credit losses that occur before December 2026. While the fund's high-quality portfolio provides a wide margin of safety, the ultimate return depends on the creditworthiness of its underlying issuers. For a value investor, this is a known, finite risk. The price paid today should reflect the probability of that outcome, not just the stated yield.

Compared to similar finite-maturity options, IBDR offers a straightforward choice. The iShares iBonds Dec 2027 Term Corporate ETF (IBDS) is a direct alternative, mirroring IBDR's structure but with a one-year extension. Both funds target investment-grade corporate bonds and offer similar yields, providing a comparable safety profile for a longer time horizon. The decision between them hinges on the retiree's specific cash flow needs and their view on the credit cycle over the next two years. IBDS trades the immediate principal return for an additional year of income, a trade-off that may be acceptable for those seeking to delay reinvestment.

More broadly, the environment makes durable income sources like IBDR increasingly relevant. With central banks cutting rates, money-market yields are falling, eroding the income available from cash alternatives and making it harder to preserve purchasing power. This shift creates a potential inflection point for retirees. As cash loses its edge, the appeal of a vehicle that locks in a 4%+ yield with a defined end date grows. IBDR provides a disciplined, low-cost way to capture that yield without the volatility of longer-duration bonds or the reinvestment risk of traditional bond funds.

In a retiree's portfolio, IBDR serves as a precise, time-bound building block. It is not a core holding for a lifetime, but a strategic allocation for a specific phase. It can be used to generate predictable income while planning for the next reinvestment, much like a bond ladder. Its low cost, stability, and defined maturity make it a tool for managing cash flow with minimal friction. For a retiree, the value here is not in speculation, but in execution-a way to convert today's higher yields into tomorrow's certainty.

Catalysts, Risks, and What to Watch

The investment thesis for IBDR is straightforward and time-bound. The main catalyst is the fund's liquidation in December 2026. At that point, shareholders will receive the principal returned from the maturing bonds. This is the entire purpose of the investment: a guaranteed, predictable return of capital after a defined period. The monthly income stream is the reward for waiting, and the final distribution is the payoff.

The primary risk to this payoff is credit loss. While the fund's portfolio is overwhelmingly investment-grade, the BBB-rated bonds make up 41% of the holdings. If any of these issuers default before their maturity, the principal returned to shareholders will be less than the initial investment. The fund's structure provides a margin of safety by holding these bonds to maturity, but it does not eliminate the risk. Retirees must monitor the broader economic environment, as a recession could increase default rates, particularly among the more speculative end of the investment-grade spectrum.

For a retiree, the decision to invest in IBDR is also a bet on the path of interest rates. The fund's current 4%+ yield is attractive, but it is fixed. If short-term yields fall further, as they have with the Fed cutting rates, cash alternatives become less competitive. This makes IBDR's locked-in yield more valuable. However, it also means that the reinvestment opportunity after December 2026 will likely be at lower rates. The fund's finite lifespan creates a clear inflection point: the retiree must plan for that next step.

The bottom line is that IBDR is a disciplined, low-cost tool for a specific goal. Its success depends entirely on the creditworthiness of its current portfolio and the timing of its liquidation. Retirees should watch the economic cycle and Fed policy, as these will influence the default risk and the attractiveness of the final principal return. For those seeking a defined, stable income stream with a known end date, the catalyst is clear, the risks are known, and the watchpoints are manageable.

Comentarios

Aún no hay comentarios