Assessing the Impact of Political Instability on French Credit Default Swaps and European Sovereign Risk

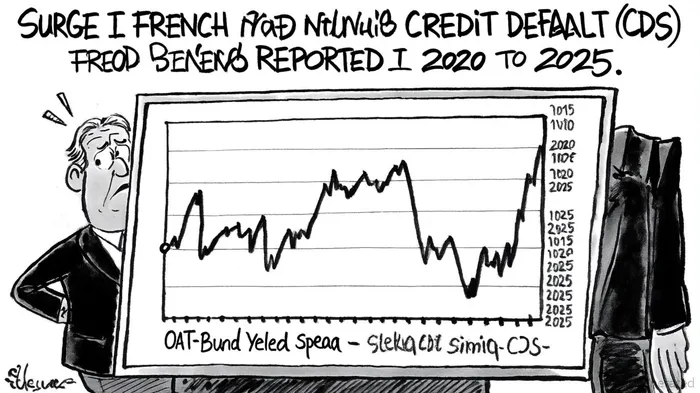

Political instability in France has emerged as a critical driver of risk in European fixed-income markets, with Credit Default Swaps (CDS) and sovereign bond spreads serving as early warning signals. From 2020 to 2025, France's CDS spreads have surged by 27% year-on-year and 15% in the last month alone, reflecting deepening concerns over fiscal sustainability and governance, according to a Samco analysis. This volatility is compounded by public debt reaching 112% of GDP (€3.346 trillion) in 2024, with interest payments projected to rise from 2.5% of GDP in 2025 to 3% by 2029, as noted in the Samco analysis. The collapse of the French government in September 2025 and the subsequent paralysis in parliament have further eroded investor confidence, widening the 10-year OAT-Bund spread to 80 basis points-a level not seen since the height of the Eurozone debt crisis, according to a Russell Investments note.

The implications extend beyond France's borders. As the second-largest economy in the eurozone, its fiscal and political challenges pose systemic risks to the bloc. A Greek-style debt crisis looms if austerity measures are imposed by the EU or IMF, potentially triggering social unrest and spillover effects in Germany and Italy, which are heavily exposed to French debt, as the Samco analysis warns. The European Central Bank (ECB) faces a delicate balancing act: while its Transmission Protection Instrument (TPI) could stabilize markets, uncertainty persists about its willingness to purchase French bonds amid ongoing Excessive Deficit Procedure (EDP) actions cited by Samco. This ambiguity has left investors bracing for a potential rise in French bond yields above 5%, which would exacerbate borrowing costs and strain the broader Eurozone's fiscal architecture, a risk highlighted by the Samco analysis.

For institutional investors, the evolving landscape demands a recalibration of risk management frameworks and asset allocation strategies. Traditional mean-variance optimization (MVO) models, which rely on historical correlations and volatilities, are increasingly challenged by the unpredictable nature of political shocks. Factor-based allocation, however, offers a more robust approach by decomposing portfolios into risk drivers such as duration, credit quality, and macroeconomic sensitivity, as outlined in a Resonanz guide. For instance, shorter-duration bonds are gaining favor as yields decline in a low-inflation, weak-growth environment, while investment-grade corporate bonds-backed by strong balance sheets-are seen as a hedge against sovereign risk, according to the AllianceBernstein outlook.

High-yield markets, though attractive for their 5.75% starting yields, require active management due to dispersion in credit performance. Investors must prioritize sectors with resilient cash flows and avoid overexposure to firms with weak liquidity profiles, guidance echoed in the AllianceBernstein outlook. Additionally, tools that integrate ESG metrics and quantitative analysis are becoming essential for identifying undervalued opportunities amid heightened uncertainty, a point also emphasized by AllianceBernstein.

The ECB's anticipated rate cuts in 2025 present a dual-edged sword. While they may support shorter-dated bonds, they also risk inflating asset bubbles in longer-duration instruments, particularly if fiscal consolidation falters. Strategic asset allocation must therefore remain agile, with regular rebalancing to reflect real-time political developments and fiscal adjustments, consistent with the Resonanz guide. For example, the recent dissolution of France's minority government and the rise of populist parties have prompted some investors to increase hedging against tail risks, such as a disorderly market correction or a hard fiscal austerity scenario, as discussed in the Russell Investments note.

In conclusion, France's political instability has transformed CDS spreads and sovereign risk into pivotal metrics for European fixed-income investors. The path forward requires a nuanced blend of proactive hedging, dynamic asset allocation, and close monitoring of both fiscal and political developments. As the ECB's policy stance and the EU's fiscal governance evolve, the ability to adapt to a rapidly shifting landscape will determine the resilience of portfolios in an era of heightened uncertainty.

Comentarios

Aún no hay comentarios