Assessing the Impact of Insider Selling at Alnylam Pharmaceuticals on Investor Confidence and Stock Performance

In recent months, Alnylam Pharmaceuticals (NASDAQ: ALNY) has drawn attention for its pattern of insider selling, most notably a $1,103,451 transaction by CFO Jeffrey V. Poulton in October 2025. This sale, disclosed via an SEC Form 4 filing, occurred as part of a mandatory "sell-to-cover" provision tied to the vesting of performance-based stock units (PSUs) granted in 2021 and 2024. While such transactions are often routine-executives liquidating shares to meet tax obligations-the broader context of Alnylam's insider activity raises questions about investor sentiment and near-term stock performance.

The Mechanics of the Recent Sale

Poulton's October 2025 sale involved shares priced between $446.19 and $457.64, reflecting the stock's volatility during the transaction window, the filing shows. The vesting of PSUs was linked to the company's achievement of clinical milestones, including the initiation of Phase 3 trials for RNAi therapeutics, the Form 4 indicates. However, the timing of the sale-amid a broader wave of insider selling-has sparked scrutiny. For instance, in August 2025 alone, executives like EVP Pushkal Garg and CEO Yvonne Greenstreet sold shares totaling over $2.1 million, according to MarketBeat insider trades.

Historical Insider Selling Trends

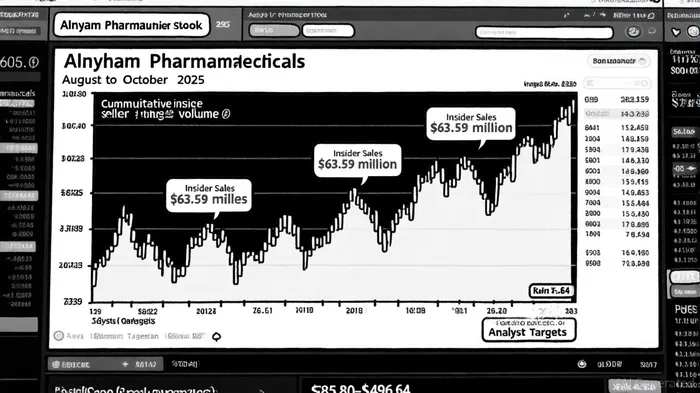

Alnylam's insider selling is not an isolated event. Over the past 12 months, insiders have offloaded $63.59 million worth of stock, with executives and directors frequently reducing holdings to cover taxes or diversify portfolios, according to Yahoo Finance insider transactions. For example, in Q1 2025, Greenstreet sold $698,041 in shares, while in Q4 2024, she liquidated $309,521 in holdings, per an InsiderTrades data. These patterns suggest a consistent, if not alarming, trend of insider disengagement. Analysts have noted that such activity can signal mixed messages. On one hand, selling to meet tax obligations is a neutral event. On the other, repeated large-scale transactions may erode investor confidence, particularly if they coincide with stock price declines. Between March and October 2025, ALNY's stock price fluctuated between $239.24 and $484.21, with insiders often selling at peaks, MarketBeat's data show.

Market Reaction and Analyst Outlooks

The October 2025 insider sales coincided with a 1.01% drop in ALNY's stock price, closing at $456.35 on October 3, according to a MarketBeat alert. While this decline could reflect broader market conditions, the timing of the sales-particularly by high-profile executives-may have amplified short-term pessimism. Analysts, however, remain divided. A consensus "buy" rating persists, with 69 buy ratings and 28 holds, per Markets Insider, but price targets vary widely, from $385.80 to $496.64.

Notably, UBS, Scotiabank, and JP Morgan recently upgraded their price targets, citing Alnylam's projected shift from losses to profitability and revenue growth to $3.5 billion in 2025, according to a Benzinga roundup. These upgrades counterbalance concerns about insider selling, emphasizing the company's pipeline advancements and financial resilience.

Investor Implications

For investors, the key question is whether insider selling reflects a lack of confidence or routine financial planning. In Alnylam's case, the latter appears more plausible. The PSUs vesting in October 2025 were tied to clinical milestones, indicating executives' alignment with long-term goals. Moreover, the company's recent drug approvals and corporate responsibility initiatives, per Alnylam investor relations, suggest a strategic focus on growth.

However, the sheer volume of insider sales-particularly by top executives-cannot be ignored. While analysts maintain a cautiously optimistic stance, investors should monitor future transactions and their correlation with stock price trends. A sudden spike in selling, especially during earnings periods or clinical trial announcements, could signal underlying concerns.

Conclusion

Alnylam Pharmaceuticals' insider selling in 2025 reflects a mix of routine tax-related transactions and broader portfolio adjustments. While the October 2025 sale by Poulton and others may temporarily dent investor confidence, the company's strong analyst ratings and projected financial turnaround offer a counterbalance. Investors should weigh these factors against Alnylam's pipeline progress and macroeconomic conditions, recognizing that insider activity alone is not a definitive indicator of future performance.

Comentarios

Aún no hay comentarios