Assessing the Impact of a 0.3% MoM PCE Price Surge on Equity Valuations and Inflation Dynamics

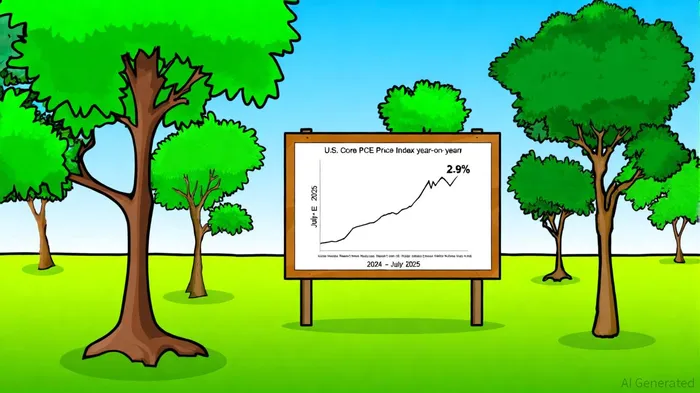

The U.S. Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve's preferred inflation gauge, has remained stubbornly elevated, with the core PCE index—the measure excluding volatile food and energy—posting a 0.3% month-over-month (MoM) increase in July 2025, consistent with June's reading[2]. On an annual basis, core PCE inflation accelerated to 2.9% in July, up from 2.8% in June, marking the highest level in five months[2]. This persistence in inflation, particularly in services sectors like housing and recreation[2], has forced the Fed into a delicate balancing act: addressing inflationary pressures while responding to a softening labor market.

Inflation Dynamics: A Mixed Picture

The 0.3% MoM surge in core PCE prices underscores the stickiness of inflation, even as headline PCE inflation (which includes food and energy) remained flat at 2.6% YoY[4]. Services inflation, which accounts for nearly two-thirds of the PCE basket, has proven resilient. Prices for services rose 0.3% in July, driven by housing costs and healthcare, while goods prices fell 0.1% due to declining energy and food prices[4]. This divergence highlights the challenge of disentangling transitory from persistent inflationary forces.

Data from the Bureau of Economic Analysis (BEA) indicates that the core PCE index is expected to remain near 0.3% MoM in August 2025, translating to an annualized 3.02% reading[3]. Such figures, while below the long-term average of 3.23%[4], still exceed the Fed's 2% target, complicating the central bank's path toward normalization.

Fed Policy: A Cautious Pivot

The Federal Reserve's September 2025 rate cut—its first since January—reflects this tension. After cutting the federal funds rate by 25 basis points to 4.00%-4.25%, the Fed emphasized a “data-dependent” approach, acknowledging that inflation remains “moderately above” its target[1]. The decision was influenced by a weakening labor market, where August job gains came in at just 22,000, and the unemployment rate rose to 4.3%[1].

However, the Fed's pivot is not a full-throated easing. Officials have signaled that further cuts will depend on whether inflation shows “sustained progress” toward 2%. With core PCE inflation at 2.9%, the path for additional cuts remains conditional. As one official noted in a recent speech, “The next move will hinge on whether services inflation begins to decelerate meaningfully”[5].

Growth Stocks: A Tailwind or a Headwind?

For growth stocks, particularly in technology and consumer discretionary sectors, the rate cut offers a near-term tailwind. Lower borrowing costs reduce the discount rate for future cash flows, boosting valuations for companies reliant on long-term financing. For example, tech firms with high R&D expenditures or ambitious expansion plans stand to benefit from cheaper capital[1].

The housing market, another growth stock beneficiary, may also see a boost as mortgage rates decline in response to the Fed's easing. Homebuilders and real estate investment trusts (REITs) could experience increased demand, though this depends on how quickly rate cuts translate to lower mortgage rates.

That said, the outlook is not uniformly positive. Sectors like banking face headwinds as net interest margins compress. With the Fed's rate cuts reducing the spread between lending and deposit rates, regional banks and mortgage lenders may see profitability pressured[1].

Conclusion: A Delicate Equilibrium

The 0.3% MoM core PCE surge underscores the Fed's dilemma: inflation remains a drag on accommodative policy, yet labor market weakness demands action. For investors, the key takeaway is that growth stocks will likely outperform in this environment, but the magnitude of gains will depend on the pace of inflation moderation and the Fed's follow-through on rate cuts. As the September 26 PCE data release looms[1], markets will be watching for signs that the Fed's cautious pivot is justified—or if further tightening remains on the table.

Comentarios

Aún no hay comentarios