Assessing Ethos's Market Potential and IPO Readiness in a Fragmented Industry

Ethos Technologies, a San Francisco-based insurtech startup, has filed for a U.S. initial public offering (IPO) under the ticker symbol “LIFE,” signaling its readiness to capitalize on a rapidly evolving insurance technology landscape. The company's decision to go public in 2025 aligns with a broader industry trend of digital transformation and a robust IPO market, as highlighted by Deloitte's forecast of $45–$50 billion in IPO proceeds for the year[1]. This analysis evaluates Ethos's market potential, IPO readiness, and strategic positioning within a fragmented insurtech sector.

Market Potential: A Digital-First Disruptor in a High-Growth Industry

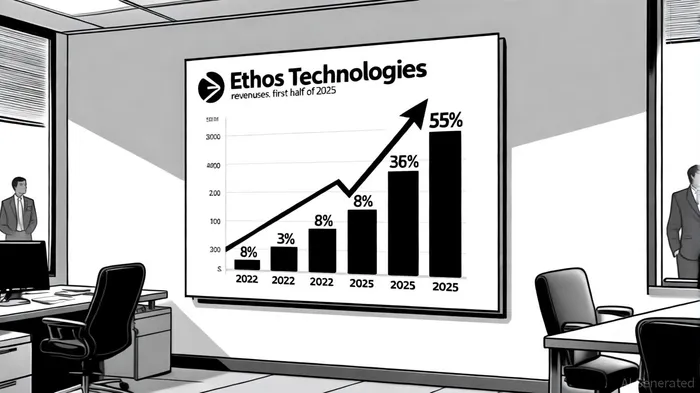

The global insurtech market is projected to grow at a staggering 36% compound annual growth rate (CAGR), reaching $132.9 billion by 2034[2]. Ethos's AI-powered underwriting and digital-first distribution model position it as a key player in this expansion. The company reported a 55% revenue surge in the first half of 2025, driven by a 70% increase in activated policies to 94,405[3]. Its 8% share of the U.S. term life insurance market in 2025—up from 3% in 2022—reflects its ability to leverage automation and data analytics to streamline operations[4].

Ethos's competitive edge lies in its ability to reduce underwriting time by 75% through machine learning algorithms and its focus on embedded insurance models. By integrating coverage into broader financial services, the company taps into a $50.2 billion U.S. insurtech market expected to grow at 6.05% annually[5]. Strategic partnerships with financial advisors, employers, and affinity groups further amplify its reach, enabling cost-effective customer acquisition while addressing gaps in traditional insurance distribution[6].

IPO Readiness: Financial Strength and Favorable Market Conditions

Ethos's financial performance underscores its IPO readiness. The company posted net income of $30.7 million on $183.7 million in revenue during the first half of 2025, demonstrating profitability amid a sector that has historically struggled with margins[3]. Its partnership with underwriters Goldman Sachs and J.P. Morgan—a move that signals institutional confidence—positions it to navigate the complexities of public market scrutiny[1].

The timing of the IPO is also strategically advantageous. The 2025 IPO market, particularly in technology and healthcare, is buoyed by a recovering economy and investor appetite for innovation-driven companies[1]. With the broader insurtech sector valued at $50.2 billion in 2025[5], Ethos's public listing could attract capital from both traditional insurance investors and tech-focused funds seeking exposure to AI-driven disruption.

Competitive Landscape: Navigating Challenges in a Fragmented Sector

Despite its strengths, Ethos operates in a highly competitive and volatile environment. The insurtech sector faces challenges such as unaffordable premiums, insurance deserts in high-risk regions, and the need for sustainable growth models[2]. Startups like BlockRisk and Driverly are also vying for market share by targeting niche segments, such as risk mitigation and AI-powered auto insurance[7].

Ethos's response to these challenges includes diversifying its product portfolio to include simplified issue whole life insurance and critical illness riders, which are expected to boost customer lifetime value by 25%[4]. Additionally, its focus on prevention services—such as telematics for auto insurance—aligns with industry trends toward loss reduction[2]. However, the company must also address regulatory complexities and data privacy concerns, which remain critical hurdles for insurtech firms[6].

Risks and Strategic Considerations

While Ethos's IPO prospects are strong, several risks warrant attention. The insurance sector's exposure to climate-related risks and social inflation could pressure margins, necessitating cautious underwriting practices[7]. Furthermore, the on-premises deployment model, which dominates 60% of the insurtech market due to security concerns[5], may require Ethos to invest in hybrid solutions to balance innovation with compliance.

The company's reliance on strategic partnerships also introduces execution risks. Maintaining relationships with financial advisors and employers will be crucial to sustaining its 200% growth in direct-to-consumer sales[4]. Additionally, the IPO's success will depend on Ethos's ability to demonstrate long-term profitability in a sector where many peers have yet to achieve consistent margins[3].

Conclusion: A Promising but Cautious Bet

Ethos Technologies' IPO filing reflects its emergence as a formidable player in the insurtech industry, leveraging AI, digital distribution, and strategic partnerships to capture market share. With a 55% revenue surge and a 8% U.S. term life insurance market share, the company is well-positioned to capitalize on the sector's projected $132.9 billion valuation by 2034[2]. However, its success in the public markets will hinge on its ability to navigate regulatory, economic, and competitive challenges while maintaining its innovation-driven ethos. For investors, Ethos represents a compelling opportunity in a high-growth sector—but one that demands careful scrutiny of both its technological advantages and the broader risks inherent in insurtech's fragmented landscape.

Comentarios

Aún no hay comentarios