Assessing Credit Risk Exposure in UK Retail Banking: Lloyds' GBP800 Million Motor Finance Provision and Sector-Wide Implications

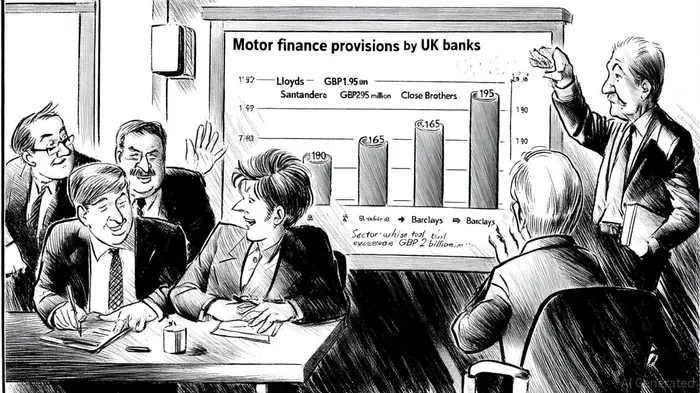

Lloyds Banking Group's recent GBP800 million increase in its motor finance provision-raising the total to GBP1.95 billion-has reignited scrutiny over credit risk exposure in the UK retail banking sector. This move, announced on October 13, 2025, reflects the bank's reassessment of liabilities tied to the Financial Conduct Authority's (FCA) proposed redress scheme for historical motor finance mis-selling, according to Motor Finance Online. The FCA estimates the industry-wide cost of the scheme could reach GBP8.2 billion, with an average payout of GBP700 per affected customer, the article adds. However, analysts suggest the final bill may exceed GBP11 billion when operational costs are included, according to Reuters.

Lloyds' Strategic Reassessment and Sector-Wide Trends

Lloyds' provision increase underscores the evolving nature of the redress scheme. The bank cited the FCA's consultation proposals, which suggest a higher likelihood of broader eligibility for redress and larger compensation than previously anticipated, as reported by Motor Finance Online. While LloydsLYG-- disputes the FCA's methodology-arguing it does not fully reflect actual customer loss-the bank has prudently set aside GBP1.95 billion as its best estimate, according to the same Motor Finance Online piece. This aligns with sector trends: Santander UK, Close Brothers Group, Barclays, and others have provisioned GBP295 million, GBP165 million, and GBP90 million respectively, as reported by Yahoo Finance. Collectively, UK banks' provisions now exceed GBP2 billion, with Fitch Ratings noting that large institutions like Lloyds have robust capital buffers to absorb these costs, while medium-sized lenders face greater vulnerability, Motor Finance Online noted.

The FCA's focus on "widespread failings" in disclosing discretionary commission arrangements (DCAs) between lenders and dealers has further complicated risk assessments, the Yahoo Finance coverage observed. A Supreme Court ruling in August 2024 broadened the scope of eligible claims, creating uncertainty over final liabilities, the same Yahoo Finance report added. For instance, Bank of Ireland, with a 2% market share, may need to increase its GBP143 million provision to GBP220 million, according to The Irish Times.

Implications for UK Retail Banking Stability

The sector's resilience hinges on its ability to manage these provisions without compromising capital adequacy. According to Motor Finance Online, major banks like Lloyds and Barclays are well-positioned due to strong profitability and high capital ratios. However, medium-sized lenders such as Close Brothers-already grappling with lower margins-face heightened risks, Motor Finance Online observed. The Bank of England's 2025 stress test guidelines emphasize the need for banks to incorporate counterparty and liquidity risks into their capital strategies, a challenge exacerbated by the motor finance scandal, as set out in Bank of England guidance.

Regulatory scrutiny is intensifying. The Prudential Regulation Authority (PRA) has prioritized improvements in risk governance and data aggregation, critical for accurate credit risk modeling, a point also underscored in Bank of England guidance. Deloitte highlights that robust data frameworks are essential for Basel 3.1 compliance, which is now delayed until 2027. Meanwhile, the FCA's extended consultation on redress reforms aims to streamline claims processing, though this may delay final cost clarity, Yahoo Finance reported.

Investor Considerations and Market Reactions

Despite the financial hit, Lloyds' share price rose 6% post-announcement, driven by confidence in its cost management and GBP1.7 billion share buyback plan, Motor Finance Online reported. However, investors remain cautious. RBC analysts note that Barclays and Close Brothers may need additional provisions if the FCA's proposals harden, according to Yahoo Finance. The sector's stability will also depend on the Supreme Court's April 2025 ruling, which could redefine the scope of redress and trigger further provisioning, The Irish Times warned.

In conclusion, while the UK retail banking sector demonstrates resilience through strong capital buffers and regulatory oversight, the motor finance scandal underscores systemic vulnerabilities. Investors must weigh the sector's capacity to absorb costs against evolving regulatory and legal uncertainties. For Lloyds and its peers, the path forward requires balancing prudence with strategic capital allocation to maintain long-term stability.

Comentarios

Aún no hay comentarios