Assessing BBVA's Q3 Earnings Decline: A Buying Opportunity Amid Currency Headwinds?

A Mixed Earnings Picture: Growth Amid Regional Headwinds

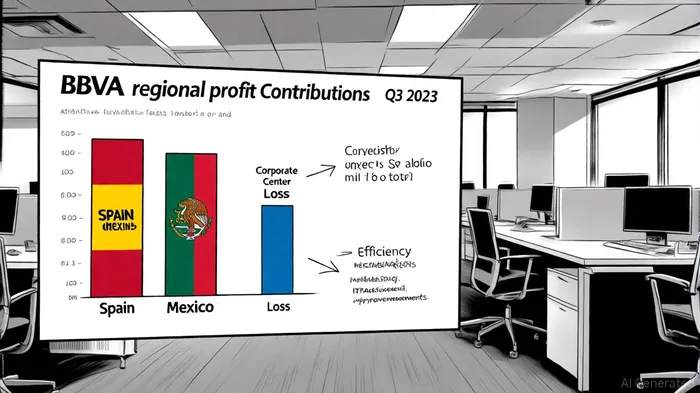

BBVA reported a net attributable profit of €5,961 million for the first nine months of 2023, a 24.3% increase compared to the same period in 2022, driven by a 29.4% rise in net interest income, according to a Freedom Investment filing. However, this growth was not uniform across regions. Spain emerged as a standout performer, with a 61.9% year-on-year profit surge to €2,110 million, while Mexico's results were tempered by weaker core revenue and currency-related pressures, as shown in BBVA's Q3 highlights. The Corporate Center, meanwhile, reported a loss of €1,321 million, primarily due to negative contributions from exchange rate hedges, as noted in the Freedom Investment filing.

The bank's operating expenses rose by 18.1%, reflecting inflationary trends in its operating regions, yet its efficiency ratio improved to 41.8%, a 328-basis-point improvement year-on-year, according to the same Freedom Investment filing. This suggests that BBVABBVA-- is managing cost discipline effectively, even as external pressures mount.

Valuation Metrics: Attractive Multiples Amid Currency Risks

BBVA's valuation appears compelling for long-term investors. As of the latest data, the stock trades at a price-to-earnings (P/E) ratio of 10.34 and a PEG ratio of 1.03, indicating a relatively low valuation relative to earnings growth, according to a Yahoo Finance article. Analysts have also noted the bank's strong capital position, with a fully loaded CET1 ratio of 12.73% as of September 30, 2023, which was highlighted in the Freedom Investment filing.

Despite currency headwinds, BBVA has demonstrated historical resilience. For instance, during the 2025 Q1 period, the bank reported a net profit of €2.7 billion, a 23% year-over-year increase, even as Mexico and Turkey faced economic challenges, as reported in an Investing.com report. This resilience is underpinned by a hedging strategy that covers 70% of subsidiaries' capital excess and 40–50% of expected net attributable profit over 12 months, as detailed in the 1Q25 risk report.

Strategic Value Investing Considerations

For value investors, BBVA's recent actions-including a €1,000 million share buyback program and a 33.3% increase in its interim dividend-signal confidence in its capital structure, as noted in the Freedom Investment filing. Institutional investors have also shown growing interest, with entities like Freedom Investment Management Inc. acquiring new stakes in the bank, according to that filing.

Barclays analyst Cecilia Romero has reiterated a "Buy" rating with a €18 price target, citing BBVA's potential to reward shareholders through capital returns and operational efficiency, according to an InsiderMonkey report. Morgan Stanley, while more cautious, has assigned an "Equal Weight" rating with a €19 target, as described in that InsiderMonkey report. These divergent views reflect both optimism about BBVA's long-term prospects and caution regarding short-term currency risks.

Risks and Mitigants

Currency fluctuations remain a key risk, particularly in emerging markets like Mexico and South America, where provisions for impairment rose by 35.5% year-on-year, as reported in the Freedom Investment filing. However, BBVA's liquidity buffers-such as a Liquidity Coverage Ratio (LCR) of 138% and a Net Stable Funding Ratio (NSFR) of 127% in Q1 2025-demonstrate its capacity to weather such volatility, according to the 1Q25 risk report.

Conclusion: A Calculated Bet for Value Investors

While BBVA's Q3 earnings reflect the challenges of a volatile macroeconomic environment, its strong capital position, efficient cost management, and strategic hedging practices position it as a potential value opportunity. For investors willing to navigate currency risks, the bank's attractive valuation metrics and institutional confidence make it a compelling case study in strategic value investing.

Comentarios

Aún no hay comentarios