Arista Networks: A Post-Analyst Day Valuation Re-Rating and Infrastructure Tailwinds Analysis

Arista Networks (ANET) has long been a bellwether for the networking sector, but its recent strategic pivot toward artificial intelligence (AI) and high-speed infrastructure has positioned it as a potential re-rating candidate. Following its 2025 Analyst Day on September 11, the company outlined an aggressive growth trajectory, emphasizing AI-driven demand, Ethernet dominance, and international expansion. This article examines the catalysts for a valuation re-rating and the infrastructure tailwinds that could propel Arista's long-term performance.

Valuation Re-Rating Catalysts: AI and Strategic Clarity

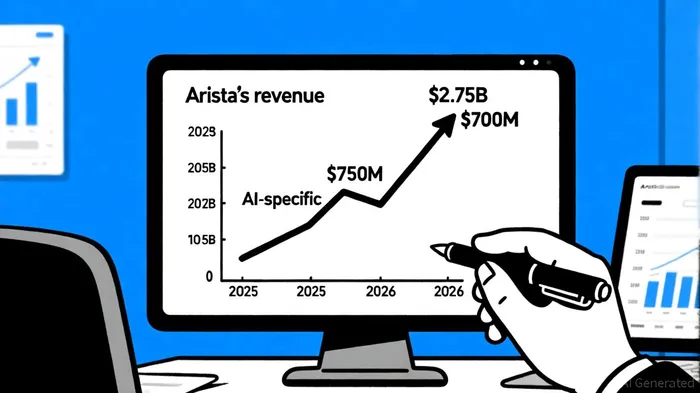

Arista's 2025 Analyst Day provided a roadmap for its AI-centric future. Management forecasted $2.75 billion in AI-related networking revenue by 2026, a 70% increase from current levels, and reiterated a $10.5 billion revenue target for 2026—a 20% year-over-year growth rate[2]. These figures align with the company's 2023 guidance, suggesting a consistent long-term vision. However, the stock's mixed post-event reaction—initially rising before reversing lower—highlighted investor skepticism about execution risks and competitive dynamics[2].

The re-rating potential hinges on Arista's ability to capitalize on AI infrastructure demand. According to a report by Skygrove Research, AI-related sales are expected to reach $750 million in 2025, with Ethernet benefits unfolding gradually as AI transitions from testing (2023) to full-scale production (2025)[3]. Arista's focus on 400G and 800G Ethernet solutions—critical for high-performance computing—positions it to benefit from this shift[3]. The company's recent product launches, such as the Ethalink 7700 and enhanced 800G offerings, underscore its technical readiness[4].

A further catalyst is the 4-for-1 stock split, announced in December 2024, which aims to broaden ownership and liquidity[1]. While splits are often symbolic, they signal management's confidence in future growth and could attract retail and institutional investors.

Infrastructure Tailwinds: AI, Cloud, and Enterprise Expansion

Arista's growth is underpinned by three macro trends:

AI-Driven Networking Demand:

The transition to AI workloads is accelerating. Arista's Q3 2024 results, which showed a 20% year-over-year revenue increase to $1.81 billion, were fueled by hyperscale partnerships like MetaMETA-- and the development of the 7700R4 Distributed Etherlink Switch[1]. AI's insatiable appetite for bandwidthBAND-- is driving a shift from 100G to 400G/800G infrastructure, a space where AristaANET-- has a first-mover advantage[3].Cloud and Enterprise Automation:

Arista's CloudVision platform, now enhanced with zero-trust security and automation tools, is gaining traction in enterprise markets[1]. This aligns with broader trends of hybrid cloud adoption and digital transformation, which require scalable, secure networking solutions.Ethernet's Dominance Over InfiniBand:

At the 2025 Analyst Day, management emphasized Ethernet's growing share in AI data centers, challenging InfiniBand's traditional dominance[2]. This is a critical differentiator, as Ethernet's ecosystem and cost advantages make it a natural fit for large-scale AI deployments.

Financial Health and Market Realism

Arista's financials reinforce its growth story. For 2025, the company expects $8 billion in total revenue (15–17% growth) and $1.5 billion in AI networking revenue[1]. Operating margins are projected to stabilize at 43–45%, reflecting scale and operational efficiency[2]. However, investors must balance optimism with caution. While Arista's AI ambitions are compelling, execution risks—such as supply chain constraints or slower-than-expected AI adoption—could delay re-rating.

Conclusion: A High-Conviction Play on AI Infrastructure

Arista Networks is uniquely positioned to benefit from the AI infrastructure boom. Its post-Analyst Day guidance, combined with robust Q3 2024 results and a clear product roadmap, suggests a compelling re-rating story. While near-term volatility is likely, the long-term tailwinds—AI adoption, cloud expansion, and Ethernet's rise—provide a durable foundation for growth. Investors who can stomach short-term noise may find Arista's stock increasingly attractive as the AI-driven networking market matures.

Comentarios

Aún no hay comentarios