AppLovin's Recent Wall Street Momentum: Sustainable Growth or Speculative Hype?

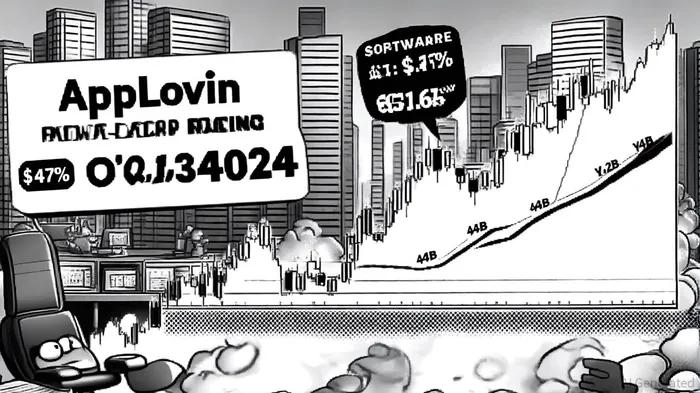

AppLovin (NASDAQ: APP) has captured Wall Street's attention in late 2024, with its stock surging 47% following Q3 results that defied expectations[1]. The company's revenue hit $1.2 billion, a 38.6% year-over-year increase, while its Software Platform revenue grew at a blistering 65.6% pace to $835.19 million[2]. Adjusted EBITDA of $721.6 million exceeded forecasts by 11.8%, and the board raised its Q4 revenue guidance to $1.24–$1.26 billion, surpassing the $1.18 billion consensus[3]. Analysts like Stifel have raised price targets to $250, citing the Software Platform's dominance, while Morgan Stanley cautions that sustaining such growth may prove challenging[4]. But is this valuation driven by AppLovin's strategic reinvention—or is it a speculative bet on a fading star?

The Case for Sustainable Growth

AppLovin's transformation from a gaming-centric company to an AI-driven adtech leader underpins its recent momentum. In 2024, the firm sold its mobile gaming division for $900 million, freeing resources to focus on its advertising business[5]. This pivot has paid off: advertising revenue soared 75% YoY to $3.2 billion in 2024, with an impressive 58% adjusted EBITDA margin[6]. The Axon 2.0 AI platform, which optimizes ad targeting and performance, has been a key driver. Early forays into e-commerce advertising have also shown promise, with pilot programs reporting nearly 100% incrementality in user engagement[7].

The company's competitive positioning further supports its growth narrative. AppLovinAPP-- holds a 7.88% market share in mobile ad networks, ranking third behind URX and Google AdMob[8]. Its AI-powered MAX mediation platform has become a critical tool for developers, enabling them to maximize ad revenue across in-app and omnichannel environments[9]. Strategic acquisitions, including MoPub and Adjust, have expanded its ecosystem, while the Wurl acquisition in 2025 is accelerating its push into connected TV (CTV) advertising[10].

Risks and Speculative Concerns

Despite these strengths, AppLovin faces headwinds that could temper its valuation. The company's reliance on AI-driven ad optimization exposes it to rapid technological obsolescence. While Axon 2.0 is a current differentiator, competitors like Meta and Google are investing heavily in AI, potentially eroding AppLovin's edge[11]. Regulatory pressures also loom large: Apple's App Tracking Transparency (ATT) and GDPR restrictions limit data access, constraining ad targeting capabilities[12].

Moreover, AppLovin's aggressive expansion into e-commerce and CTV introduces execution risks. While pilot programs show high incrementality, scaling these initiatives will require significant capital and advertiser buy-in. The gaming division's sale, though strategic, has reduced revenue diversification, leaving the company more vulnerable to sector-specific downturns[13]. Morgan Stanley's cautious stance reflects concerns that AppLovin's 70% 2025 earnings growth projections[14] may be overly optimistic in a macroeconomic climate marked by inflation and potential ad spend cuts.

Valuation: A Tug-of-War Between Optimism and Caution

AppLovin's market capitalization now exceeds $125 billion, a valuation that implies continued high-margin growth. While its 25% Q1 2025 revenue growth and $2.1 billion in free cash flow for 2024[15] justify optimism, the stock's 47% post-earnings surge raises questions about overvaluation. Stifel's $250 price target assumes the company can maintain its AI-driven ad monetization and successfully scale into e-commerce and CTV. However, Morgan Stanley's skepticism highlights the challenge of sustaining 75% ad revenue growth in a competitive landscape where Google and Meta dominate[16].

Conclusion: A High-Stakes Bet on AI-Driven Adtech

AppLovin's recent performance reflects a compelling mix of strategic reinvention and operational execution. Its AI-powered ad platforms, expanding market share, and robust cash flow position it as a leader in the $1.2 trillion mobile advertising sector[17]. However, the stock's valuation hinges on its ability to navigate regulatory hurdles, sustain AI innovation, and scale into new verticals. For investors, the key question is whether AppLovin's current momentum is a reflection of its transformative potential—or a speculative overreach in a sector prone to disruption.

Comentarios

Aún no hay comentarios