Apollo Global's Outperformance in Credit Strategies and Fee-Related Earnings Growth: A Strategic Analysis of Asset Origination and Risk-Adjusted Returns

Apollo Global Management's Q2 2025 results underscore its dominance in the private credit and asset management sectors, driven by a disciplined approach to strategic asset origination and risk-adjusted returns. With fee-related earnings (FRE) surging 22% year-over-year to $627 million and total assets under management (AUM) reaching $840 billion—a 20% increase from the prior year—the firm has demonstrated exceptional resilience amid macroeconomic volatility [1]. This outperformance is not merely a function of scale but a reflection of Apollo's ability to capitalize on high-conviction secular themes while maintaining rigorous credit discipline.

Fee-Related Earnings Growth: A Testament to Operational Excellence

Apollo's Q2 2025 FRE growth of 22% far exceeded industry benchmarks, fueled by robust inflows ($61 billion) and organic asset origination ($81 billion) [1]. Total revenues of $6.81 billion, a staggering 50% beat over the estimated $4.57 billion [2], highlight the firm's ability to monetize its expanding AUM base. This performance is particularly noteworthy given the broader market's challenges in balancing liquidity constraints with investor demand for alternative assets. Apollo's disciplined fee structure and diversified revenue streams—spanning credit, real estate, and alternatives—have insulated it from sector-specific downturns, ensuring consistent cash flow generation.

Credit Strategies: Delivering Consistent Risk-Adjusted Returns

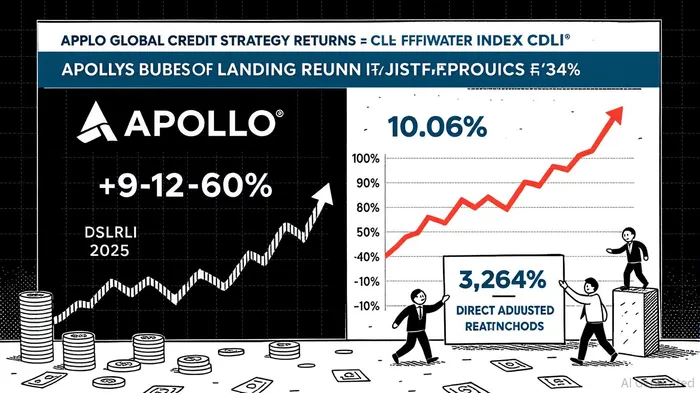

Apollo's credit strategies have been a cornerstone of its success, delivering 9–12% annualized returns over the past 12 months [1]. These figures outperform the Cliffwater Direct Lending Index (CDLI), which reported 10.06% annualized returns over the same period [3]. The firm's direct credit origination arm, which returned 12.0% trailing 12 months and 3.2% in Q2 2025 [2], exemplifies its ability to identify undervalued opportunities while maintaining a 350-basis-point spread over Treasury—a metric that underscores its risk mitigation capabilities. Apollo's focus on non-investment-grade borrowers, coupled with active portfolio management, has enabled it to capture higher yields without compromising capital preservation.

Strategic Asset Origination: A Differentiator in a Competitive Landscape

Apollo's organic origination of $81 billion in Q2 2025 [1] reflects its proactive approach to sourcing deals, particularly in high-growth sectors like AI infrastructure and energy transition. The firm's acquisition of Stream Data Centers, a strategic move to capitalize on AI-driven demand for digital infrastructure, further illustrates its alignment with long-term secular trends. This forward-looking strategy not only diversifies Apollo's asset base but also enhances its ability to generate alpha in an increasingly crowded private credit market.

Risk-Adjusted Returns: A Framework for Sustainable Growth

Apollo's risk-adjusted returns are among the most compelling in the industry. With credit losses controlled at 0.75% annually (in line with the CDLI's benchmark) [3], the firm has avoided the pitfalls of aggressive leverage or lax underwriting. Its emphasis on high-conviction themes—such as AI infrastructure, where it has secured a majority stake in Stream Data Centers—ensures that risk is allocated toward sectors with durable growth potential. This balance between risk and reward is further reinforced by Apollo's capital-efficient business model, which prioritizes shareholder returns through dividends and buybacks.

Conclusion: A Compelling Case for Immediate Investment

Apollo Global's Q2 2025 results present a compelling case for investors seeking exposure to a firm that excels in strategic asset origination and risk-adjusted returns. With FRE growth, AUM expansion, and credit strategy performance all outpacing industry benchmarks, ApolloAPO-- has positioned itself as a leader in the evolving alternative asset landscape. As macroeconomic uncertainties persist, its disciplined approach to credit investing and focus on secular growth themes make it a resilient long-term holding. For investors prioritizing both capital appreciation and income generation, Apollo's track record and forward-looking strategy offer a rare combination of stability and upside.

Comentarios

Aún no hay comentarios