Amphenol vs. Teradyne: Which AI Chip Stock Should You Buy Now?

Amphenol APH designs and manufactures electronic connectors, sensors and interconnect systems used across data centers, telecom, automotive and industrial markets. Teradyne TER provides semiconductor test equipment and industrial automation solutions essential for validating advanced chips.

Both companies serve as critical enablers of the semiconductor ecosystem, with strong exposure to AI infrastructure growth. AmphenolAPH-- supports expanding data center buildouts, while TeradyneTER-- benefits from rising demand to test increasingly complex AI processors and GPUs.

With AI-driven capital spending accelerating and chip architectures becoming more complex, both stocks are positioned to benefit from sustained semiconductor investment. Comparing them now helps investors assess which offers stronger leverage to the ongoing AI boom.

A deeper examination of their growth, durability, profitability trends and valuation will help determine which stock stands out as the smarter buy today.

The Case for APHAPH-- Stock

Amphenol has strengthened its position as a key player in the AI semiconductor ecosystem by leading in high-speed copper, power and expanding fiber interconnect solutions. In the fourth quarter of 2025, the company reported record sales of $6.44 billion, a 49% increase year over year, with IT datacom representing 38% of total revenues and growing 110% organically amid strong AI-driven data center demand. The significant growth in IT datacom sales underscores Amphenol’s expanding role in supporting next-generation GPU, server and advanced rack infrastructure for AI workloads.

Strategically, the January 2026 acquisition of CommScope’s CCS business meaningfully expands Amphenol’s fiber optic portfolio, enhancing its high-speed copper franchise and positioning the company as a comprehensive interconnect provider across AI clusters and hyperscale data center networks. The deal is expected to contribute approximately $4.1 billion in 2026 revenues and will help drive earnings growth, strengthening Amphenol’s growth. Additionally, the Trexon acquisition deepens its presence in high-reliability defense interconnect solutions, further diversifying its end-market exposure and reinforcing its long-term competitive positioning.

However, challenges include integration risks tied to large-scale acquisitions, elevated leverage following recent transactions, tax uncertainties in China and cyclical softness across select end markets. Nonetheless, Amphenol’s diversified end-market exposure, automation capabilities and strong AI-driven backlog create a compelling long-term growth runway within the semiconductor infrastructure value chain.

The Zacks Consensus Estimate for the first quarter of 2026 earnings is currently pegged at 94 cents per share, an increase of 9.3% over the past 30 days. This indicates a 49.21% decrease from the figure reported in the year-ago quarter.

Image Source: Zacks Investment Research

The Case for TERTER-- Stock

Teradyne is solidifying its role as a critical enabler of the AI semiconductor ecosystem, directly benefiting from accelerating AI-driven data center investments. In the fourth quarter of 2025, revenues climbed 44% year over year to $1.08 billion, led by $883 million in Semiconductor Test sales fueled by robust demand across AI compute, networking and memory applications. Notably, AI-related customers represented more than 60% of quarterly revenues and are projected to approach 70% in the first quarter of 2026, highlighting Teradyne’s growing concentration in next-generation AI infrastructure.

Momentum is most pronounced in SoC and memory, where AI-driven demand is reshaping Teradyne’s revenue mix. SoC test revenues delivered strong growth in 2025, supported by expanding networking and high-value compute applications, while memory performance benefited from share gains in HBM and DRAM tied to AI acceleration. The portfolio continues to tilt toward compute-centric opportunities as next-generation workloads scale. Further strengthening its AI data center presence, Teradyne formed a joint venture with MultiLane to advance high-speed interconnect testing, broadening its capabilities from wafer-level validation to rack-scale system test solutions.

Financially, Teradyne generated $450 million in free cash flow and closed the fourth quarter with $448 million in cash and marketable securities, underscoring solid liquidity and balance sheet strength. The company is strategically positioned to outpace broader market growth, supported by expanding exposure to high-growth AI-driven end markets. Its mid-term earnings framework targets $6 billion in revenues within an ATE total addressable market of $12-$14 billion, highlighting substantial runway for scalable, above-market expansion in the years ahead.

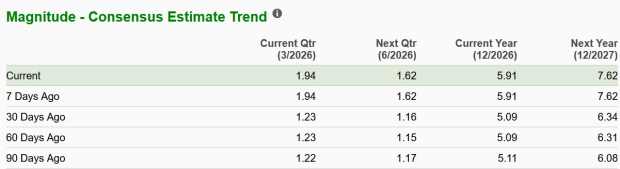

The Zacks Consensus Estimate for TER’s first-quarter 2026 earnings is pegged at $1.94 per share, reflecting a sharp 57.7% upward revision over the past 30 days and implying a robust 158.7% year-over-year increase.

Image Source: Zacks Investment Research

Stock Performance & Valuation: APH vs. TER

Over the past six months, Teradyne shares have surged 177.4%, significantly outperforming Amphenol’s 37.8% gain. Teradyne’s rally has been driven by immediate, high-volume demand for AI chip testing equipment, where the company holds a leading position in validating advanced semiconductors used in AI, cloud and networking applications.

APH vs. TER Stock Performance

Image Source: Zacks Investment Research

Both Amphenol and Teradyne trade at premium valuations as suggested by a Value Score of D and F, respectively. On a forward 12-month Price/Sales basis, Amphenol appears relatively more reasonable at 5.86X, compared with Teradyne’s steeper 12.27X, suggesting investors are assigning a higher growth premium to Teradyne.

APH vs. TER Valuation

Image Source: Zacks Investment Research

TER Looks Stronger Than APH Now

While both Amphenol and Teradyne are well positioned for AI infrastructure growth, Teradyne offers stronger near-term earnings momentum, higher AI revenue concentration, accelerating estimate revisions and superior stock performance. Despite its richer valuation, TER’s direct leverage to AI chip complexity and testing demand makes it the stronger pick right now.

With Teradyne sporting a Zacks Rank #1 (Strong Buy) at present and Amphenol carrying a Zacks Rank #2 (Buy), TER stands out as the more compelling choice right now. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amphenol Corporation (APH): Free Stock Analysis Report

Teradyne, Inc. (TER): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios