Amphenol Drops 5% Year to Date: Buy, Sell or Hold the Stock?

Amphenol APH shares have dropped 5.1% year to date, outperforming the Zacks Computer and Technology sector’s decline of 7.5%. The underperformance can be attributed to macroeconomic challenges, geopolitical volatility and headwinds related to AI-related capital expenditure spending. APHAPH-- investors were also spooked by rising integration risks post the acquisition of CommScope’s Connectivity and Cable Solutions (CCS) business and the lower initial margin of the acquired business. Constrained supply chain and rising commodity prices are a concern for Amphenol’s prospects.

Amphenol expects commercial air and automotive end-market sales to moderate sequentially. Mobile devices are expected to decline in the 30% range due to seasonality. This guidance is expected to remain an overhang on the stock. So, what should APH investors do with the stock? Let’s dig deep to find out.

APH Shares Are Overvalued

Amphenol has a stretched valuation as suggested by a Value Score of D.

In terms of the forward 12-month price-to-earnings (P/E), APH is trading at 27.87X compared with the broader sector and peers, including TE Connectivity TEL, Corning GLW and Belden BDC. The broader sector is trading at 22.17X while TE ConnectivityTEL--, CorningGLW-- and BeldenBDC-- trade at 18.14X, 41.79X and 13.75X, respectively.

APH Stock’s Valuation

Image Source: Zacks Investment Research

Acquisitions & Diversified End-Markets Aid APH’s Growth

Amphenol ended 2025 with orders of $25.4 billion, up 51% from 2024, which resulted in a book-to-bill ratio of 1.1:1. APH’s strategy of expanding its portfolio as well as end-markets through acquisitions has been a key catalyst over the trailing 12-month period. Amphenol’s expanding portfolio of fiber optic, power, antenna and sensor technologies continues to gain traction across datacom, aerospace and defense markets. Acquisitions added roughly $2 billion to revenues in 2025, while the CCS business is expected to contribute roughly $4.1 billion in revenues for 2026.

Amphenol has expanded its portfolio and market reach through targeted acquisitions across communications, medical and defense verticals. Plethora of acquisitions — Trexon, Rochester sensors, CIT, Lutze, CommScope’s Andrew business, LifeSync, Narda-MITEQ, XMA, Q Microwave, and others — have been driving Amphenol’s prospects. The CCS buyout enhanced Amphenol’s competitive positioning by enhancing its ability to offer fiber optics at scale. The company can now offer a complete end-to-end interconnect solution, and the acquisition positions APH as an important partner across the entire system architecture design decisions.

Moreover, a diversified end-market bodes well for APH’s top-line growth prospects. IT datacom now contributes 36-38% of sales, while industrial, automotive, defense, mobile and communications networks all contributed meaningfully to 2025 revenues. This reduces APH’s reliance on any single end market.

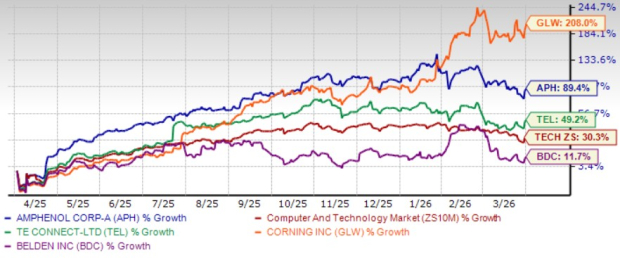

These factors have helped APH outperform peers, including TE Connectivity and Belden in the past year, but lagged Corning. Shares of TE Connectivity, Corning and Belden have returned 49.2%, 208% and 11.7%, respectively, over the same time frame.

APH Stock’s Price Performance

Image Source: Zacks Investment Research

Strong Liquidity to Boost APH’s Growth Trajectory

Amphenol generates solid cash flow, which allows management the opportunity to invest in product innovations, acquisitions and business development. In 2025, operating cash flow was $5.4 billion, whereas the free cash flow was $4.4 billion. The company returned nearly $1.5 billion to shareholders.

Total liquidity at the end of the fourth quarter was $17.5 billion, including cash and short-term investments on hand of $11.4 billion plus availability under Amphenol’s existing credit facilities. The figure also included $3.1 billion of term loan facilities put in place in anticipation of the CCS acquisition.

APH’s 1Q’26 Earnings Estimate Revision Shows Steady Trend

Amphenol expects first-quarter 2026 earnings between 91 cents and 93 cents per share, indicating growth between 44% and 48% year over year. Revenues are anticipated between $6.90 billion and $7 billion, suggesting growth in the 43-45% range. CCS is expected to contribute $900 million in sales and a couple of cents in earnings.

The Zacks Consensus Estimate for first-quarter 2026 earnings is pegged at 94 cents per share, unchanged over the past 30 days and indicating 49.21% growth over the year-ago quarter’s reported figure. The consensus mark for first-quarter 2026 revenues is pegged at $7 billion, suggesting 45.54% growth from the year-ago quarter’s reported figure.

Amphenol Corporation Price and Consensus

Amphenol Corporation price-consensus-chart | Amphenol Corporation Quote

Conclusion

Amphenol’s diversified end-market exposure, expanding interconnect portfolio and strong acquisition execution continue to support solid growth visibility. Investors already holding the stock should stay put. However, a challenging macroeconomic environment and stretched valuation make the stock risky for potential investors.

APH currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to start accumulating the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amphenol Corporation (APH): Free Stock Analysis Report

Corning Incorporated (GLW): Free Stock Analysis Report

Belden Inc (BDC): Free Stock Analysis Report

TE Connectivity Ltd. (TEL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios