Amkor Technology's Underperformance Amid Semiconductor Industry Turbulence: Structural Risks and Strategic Crossroads

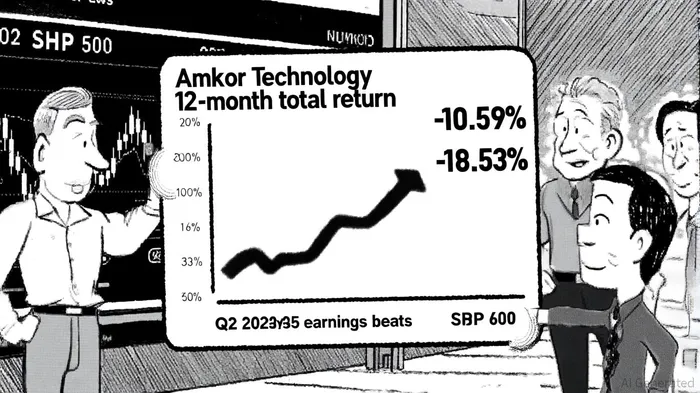

Amkor Technology (AMKR) has underperformed the broader market in 2025, with its stock posting a 12-month total return of -10.59% compared to the S&P 500's 18.53% gain, according to AMKR's performance history. This divergence raises questions about the company's ability to translate strong quarterly earnings into sustained shareholder value. While Amkor's Q2 2025 results-$1.51 billion in revenue and $0.22 earnings per share-exceeded analyst expectations, as shown in the company's Q2 2025 results, its stock price has struggled to keep pace with the broader market. Historical backtests of similar earnings-beat events since 2022 show mixed short-term reactions, with shares dipping immediately after announcements but recovering to gain approximately 9% over 30 trading days compared to a 2% gain for the benchmark. However, with only two such events in the sample, these results are not statistically significant. This underperformance reflects deeper structural risks in the semiconductor packaging and testing industry, including shifting demand dynamics, competitive pressures, and capacity constraints.

Structural Risks in Semiconductor Packaging: A Perfect Storm

The semiconductor packaging and testing sector is navigating a complex landscape of growth and vulnerability. According to an industry outlook, demand for advanced packaging technologies-driven by AI accelerators, high-performance computing (HPC), and automotive electronics-is surging. However, this growth is accompanied by critical challenges. For instance, packaging technologies for AI chips, such as those used in NVIDIA GPUs and HBM (high-bandwidth memory), are already experiencing supply tightness, and the outlook warns that underinvestment in mature nodes (40nm and above) has created a supply imbalance, with shortages expected to emerge by late 2025.

The memory market further complicates the outlook. While HBM3 and HBM3e demand is rising, Morgan Stanley warns of a potential 66.7% surplus in HBM production from 2024, which could spill over into 2025. This imbalance, coupled with weak demand for DRAM and NAND flash, introduces volatility. Additionally, sustainability concerns-such as water scarcity in Taiwan, a key manufacturing hub-threaten to disrupt production. These structural risks highlight the fragility of the industry's supply chain, even as demand for advanced packaging accelerates.

Competitive Pressures: ASE and JCET's Aggressive Expansion

Amkor's underperformance also stems from intensifying competition. As of Q2 2025, Amkor holds a 4.64% market share in semiconductor packaging, trailing industry leader ASE Technology (44.6% share) and JCET Group (12% share), according to market share data. Both rivals are aggressively expanding capacity in advanced packaging, a critical area for AI and HPC. ASE, for example, has invested $2.8 billion in Q1–Q2 2025 to expand machinery and automation for advanced packaging, per the ASE investment, while JCET reported record Q2 revenue of RMB 9.27 billion and increased R&D spending by 20.5% year-on-year in its JCET interim report.

Amkor's response includes a $7 billion investment in an Arizona-based advanced packaging campus, as noted in the Arizona campus announcement. While this aligns with U.S. reshoring initiatives like the CHIPS Act, the facility is not expected to begin production until early 2028. In the interim, competitors like ASE and JCET are capturing market share with faster capacity expansions. For instance, ASE's new $300 million plant in Malaysia and JCET's automotive-focused manufacturing base in Shanghai underscore their agility in addressing regional and sector-specific demand.

Amkor's Strategic Gambit: Balancing Short-Term Pressures and Long-Term Growth

Amkor's leadership acknowledges the dual challenges of margin compression and long-term growth. The company's Q2 2025 gross margin of 12.0% and operating income of $92 million reflect operational efficiency reported in the Q2 release, but these metrics mask structural vulnerabilities. For example, Amkor's top five customers account for 65% of revenue, according to a SWOT analysis, exposing it to client-specific risks during market downturns. Additionally, its manufacturing base is 85% concentrated in Asia, heightening exposure to geopolitical tensions.

To mitigate these risks, Amkor is diversifying its supply chain with a $1.6 billion facility in Vietnam (market data show this move) and accelerating R&D in heterogeneous integration and 3D packaging, per the SWOT analysis. However, these efforts require significant capital and time to yield returns. The Arizona campus, while transformative, will not alleviate immediate pressures from competitors or address short-term margin challenges.

Conclusion: A Tenuous Path Forward

Amkor's underperformance relative to the S&P 500 underscores the semiconductor packaging industry's structural fragility. While the company's strategic investments in the U.S. and Vietnam aim to secure its long-term position, near-term challenges-including supply chain bottlenecks, competitive overcapacity, and margin pressures-pose significant headwinds. Investors must weigh Amkor's leadership in AI packaging against its reliance on cyclical markets and the rapid expansion of rivals. For now, the stock's underperformance reflects a sector in transition, where only the most agile players will thrive.

Comentarios

Aún no hay comentarios