Amber International's Financial Opacity and the Perils of Non-GAAP Alchemy

In the world of finance, numbers tell stories—but not always the truth. Amber International Holding Limited (Nasdaq: AMBR) has painted a picture of post-merger triumph, with Q1 2025 revenue surging to $14.9 million, driven by its Wealth Management Solutions segment and a $100 million Crypto Ecosystem Reserve[1]. Yet beneath the surface, the company's financial transparency remains murky, particularly around its non-GAAP metrics. This opacity raises critical questions for investors assessing the risks of a business that claims “zero Non-GAAP EPADS” while navigating volatile markets and unproven growth strategies.

The Illusion of Growth

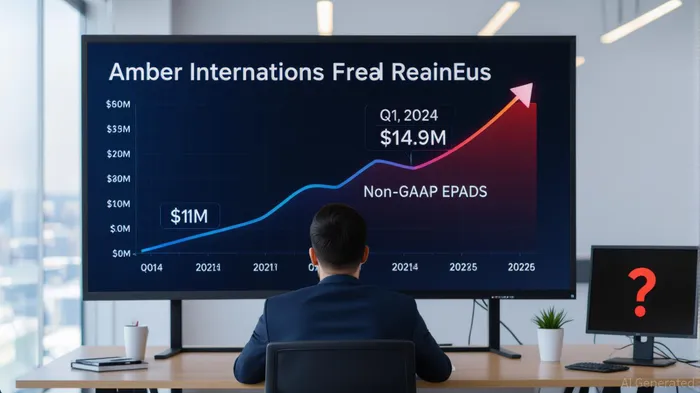

Amber's Q1 2025 results are undeniably flashy. Revenue jumped from $1 million in Q1 2024 to $14.9 million, with Wealth Management Solutions contributing $9.9 million—a 1,500% year-over-year increase[2]. Gross margins improved to 74%, and operating income turned positive at $0.8 million, reversing a $0.9 million loss in 2024[3]. These figures suggest a company on the rise. But such growth is largely attributable to the March 2025 merger with iClick, which added $6.6 million in Marketing and Enterprise Solutions revenue[4]. The question remains: Is this a sustainable transformation, or a one-time accounting trick?

The Non-GAAP Enigma

Amber's earnings call transcript reveals a GAAP EPADS of -$2.61 for Q1 2025[5], a stark contrast to its claims of “zero Non-GAAP EPADS.” While the company discloses that non-GAAP metrics like adjusted EBITDA and adjusted net income are available on its Investor Relations website[6], the absence of specific figures in public filings or press releases is troubling. Non-GAAP measures are meant to strip out one-time costs and provide a clearer view of operational performance, but without reconciliation details, investors are left to guess how Amber arrives at its “zero” figure.

This lack of transparency is not merely a technicality. It reflects a broader pattern: Amber's Q1 2025 10-Q filing, which should contain standardized disclosures, omits Non-GAAP EPADS data[7]. Meanwhile, the company's forward guidance for Q2 2025—$15.5 million to $17.5 million in revenue—rests on assumptions that remain unvalidated by auditable metrics[8]. For a firm operating in the high-risk crypto and wealth management sectors, such ambiguity is a red flag.

Revenue Trends and Segment Risks

While Amber's top-line numbers are impressive, its segment performance tells a more nuanced story. Execution Solutions revenue, for instance, fell from $29,000 in Q1 2024 to $2.7 million in Q1 2025—a 86% year-over-year decline[9]. This suggests that the company's core trading operations may be struggling, even as its wealth management arm benefits from the iClick merger. Similarly, the Q2 2025 results, though not yet filed, hint at uneven growth: while client assets rose 35.7% to $1.54 billion, Execution Solutions revenue in Q2 2025 is projected to remain volatile[10].

The company's reliance on speculative assets like BitcoinBTC-- and EthereumETH-- further compounds these risks. Amber's $100 million Crypto Ecosystem Reserve is a bold bet, but crypto markets are notoriously unpredictable. A single regulatory shift or price crash could erase gains made in wealth management, leaving investors with a hollow shell of a business.

A Call for Caution

Amber's narrative of post-merger success is compelling, but it is built on a foundation of incomplete data. The absence of Non-GAAP EPADS figures, coupled with declining performance in key segments, suggests a company more focused on hype than hard numbers. For investors, the lesson is clear: proceed with caution. Until Amber provides full reconciliation of its non-GAAP metrics and demonstrates consistent growth across all business lines, its stock remains a high-risk proposition.

Comentarios

Aún no hay comentarios