Amazon: It's Never Too Late To Buy

In the ever-shifting landscape of global commerce and technology, AmazonAMZN-- remains a paradox: a company that has grown from an online bookseller into a $2.166 trillion colossus, yet still faces skepticism about its valuation and long-term prospects. For investors willing to look beyond short-term volatility, however, the case for Amazon is compelling. The company's financial resilience, strategic dominance in cloud computing, and aggressive reinvestment in artificial intelligence (AI) infrastructure position it as a rare blend of stability and growth.

The Engine of Growth: AWS and AI-Driven Margins

Amazon Web Services (AWS) continues to be the crown jewel of the empire. In Q2 2025, AWS reported $30.9 billion in revenue, a 17.5% year-over-year increase, and contributed $10.2 billion in operating income—nearly one-third of Amazon's total operating profit for the quarter[1]. While its 18% growth rate lagged behind MicrosoftMSFT-- Azure's 39% and GoogleGOOGL-- Cloud's 32%, AWS's 32.9% operating margin in Q2 (despite a slight contraction from 39.5% in Q1 2025) underscores its profitability edge[2].

The real story lies in AWS's AI investments. With $100 billion in 2025 capital expenditures—70% allocated to AI infrastructure—Amazon is betting big on the next frontier of cloud computing[3]. New EC2 instances powered by NVIDIANVDA-- Grace Blackwell Superchips, coupled with custom silicon like Trainium and Inferentia, are positioning AWS to dominate generative AI workloads[4]. As enterprises scramble to integrate AI into their operations, AWS's first-mover advantage in scalable, secure AI deployment could widen its margins further.

Valuation: A Discounted Premium

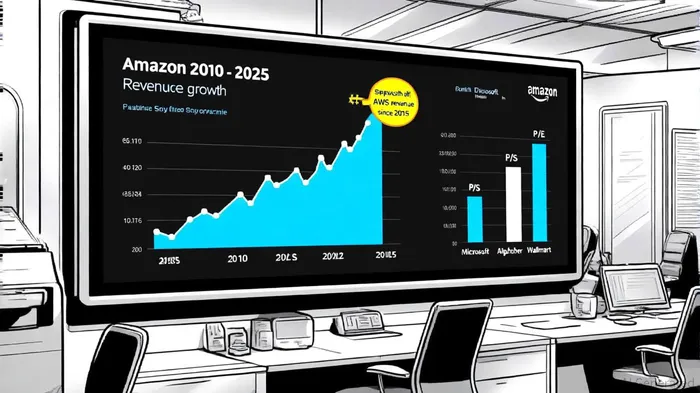

Amazon's valuation metrics suggest it is neither overpriced nor undervalued, but rather trading at a discount relative to its historical premiums and peers. Its current P/E ratio of 35.32 is 73% below its 10-year average of 131.62[5], yet it remains above Alphabet's 25.64 and Microsoft's 37.39[6]. This discrepancy reflects diverging investor sentiment: while Microsoft and AlphabetGOOGL-- are seen as stable cash cows, Amazon is still perceived as a growth stock, albeit one with maturing segments.

The P/S ratio of 3.76, though higher than the 12-month average of 3.45, is justified by Amazon's expanding revenue base and AWS's high-margin contributions[7]. By comparison, Walmart's P/S ratio of 1.21 highlights the stark difference between retail and tech valuations[8]. For Amazon, the P/S ratio reflects not just e-commerce dominance but also the intangible value of AWS's enterprise client base and AI-driven advertising tools, which drove a 22-23% surge in ad revenue in Q2 2025[9].

Historical Resilience and Competitive Positioning

Amazon's 13% year-over-year revenue growth in Q2 2025—bringing total revenue to $167.7 billion—continues a 15-year trend of compounding at an average rate of 24.4% in its cloud segment[10]. Even during the 2022 downturn, when AWS posted a $2.7 billion loss, the company's long-term vision prevailed, leading to a $39.8 billion operating profit in 2024[11]. This resilience stems from its dual-engine model: e-commerce, which still accounts for 82% of revenue, and AWS, which drives profitability.

In the cloud market, AWS's 30% share remains unmatched, though Microsoft's 20% and Google's 13% are closing the gap[12]. Yet AWS's profitability—32.9% operating margin versus Azure's 35% and Google Cloud's 28%—suggests it can sustain margins even as competition intensifies[13]. The key differentiator is AWS's AI infrastructure, which is already powering tools like Kiro (an agentic IDE) and Bedrock AgentCore, creating sticky, high-margin offerings[14].

The Case for Long-Term Investors

Critics argue that Amazon's stock is expensive given its P/E and P/S ratios. But this overlooks the company's reinvestment strategy. With $100 billion in 2025 CAPEX—focused on AI data centers, custom silicon, and networking—Amazon is building the infrastructure to capture the next decade of digital transformation[15]. For context, Microsoft and Alphabet are investing heavily in AI too, but Amazon's scale in cloud infrastructure gives it a unique advantage.

Moreover, Amazon's balance sheet is robust. Its debt-to-equity ratio of 0.44 is healthier than the industry average, and its $36.48 billion EBITDA dwarfs peers like WalmartWMT-- ($11.88 billion) and JDJD--.com ($11.88 billion)[16]. As AI adoption accelerates, AWS's ability to monetize enterprise demand for large language models and generative AI could drive operating income to $40 billion annually, further justifying its valuation.

Conclusion: A Stock for the Patient

Amazon is not a flash-in-the-pan growth story—it is a mature company with a proven ability to reinvent itself. Its AWS division is a cash-generating machine, its e-commerce business remains a fortress, and its AI investments are laying the groundwork for the next phase of growth. At a P/E of 35.32 and a P/S of 3.76, it trades at a discount to its historical premiums and offers a compelling risk-rebalance for investors who can look beyond quarterly earnings.

As Andy Jassy noted, AWS is in the midst of a “once-in-a-lifetime opportunity” with AI[17]. For those willing to hold for the long term, Amazon's combination of resilience, innovation, and valuation discipline makes it a stock that is never too late to buy.

Comentarios

Aún no hay comentarios