Algoma Steel's Q3 Adjusted EBITDA Forecast and Implications for the Steel Sector

Algoma Steel Group Inc. has released its Q3 2025 guidance, projecting total steel shipments of 415,000–420,000 net tons and an Adjusted EBITDA range of negative $80 million to negative $90 million, according to Algoma's guidance. This forecast underscores the company's struggle against trade headwinds, including the U.S.'s 50% tariffs on Canadian steel, while simultaneously advancing its transition to low-carbon steelmaking. The results reflect a broader industry narrative of volatility, where operational resilience and strategic adaptation are critical for survival.

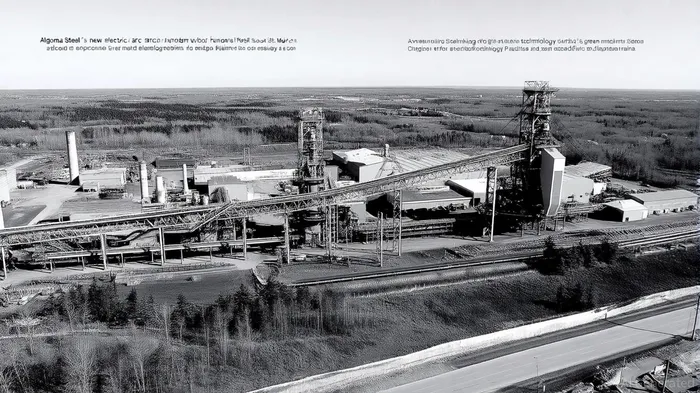

Operational Resilience: A Strategic Shift to Green Steelmaking

Algoma's recent operational milestone-the first arc and steel production from its electric arc furnace (EAF) in July 2025-marks a pivotal step in its transformation, as noted in the E3G scorecard. The EAF project, supported by CA$500 million in federal and provincial funding, according to the OECD Outlook, aims to reduce carbon emissions by up to 70%, a figure highlighted by the E3G scorecard. This shift aligns with global decarbonization goals but comes at a cost: the company's Q3 2025 EBITDA forecast remains negative, highlighting the financial strain of transitioning from traditional blast furnace operations to EAF-based production.

The EAF's integration of two Danieli Digimelter furnaces underscores Algoma's commitment to efficiency and sustainability. However, the immediate financial impact of this transition is evident. As stated by the company, "These developments are part of Algoma's broader strategic initiatives to improve operational efficiency and align with environmental goals, despite ongoing trade challenges," per Algoma's guidance. The reliance on government support to fund this transformation raises questions about long-term financial independence but also signals a pragmatic approach to navigating a carbon-constrained future.

Sector-Wide Headwinds: Trade Policies and Excess Capacity

The steel industry in 2025 is grappling with a perfect storm of trade policies and excess capacity. According to the OECD Steel Outlook 2025, global steel demand is projected to grow at a modest 0.7% annually until 2030, with regional disparities driven by China's declining demand and growth in ASEAN and MENA regions. Meanwhile, China's subsidies have distorted global competition, enabling overcapacity and triggering a surge in anti-dumping investigations. In 2024 alone, 81 antidumping cases were initiated, a five-fold increase from 2023, with 80% targeting Asian producers, as reported in the OECD Outlook.

The U.S.'s recent rollback of green steel initiatives and imposition of tariffs further complicate the landscape. For AlgomaASTL--, these policies have accelerated its focus on domestic demand and EAF steelmaking. Yet, the sector-wide reliance on blast furnace technology-accounting for over 40% of new capacity added between 2025–2027, per the OECD Outlook-suggests that decarbonization remains uneven. Algoma's EAF project, while ambitious, is an outlier in a sector still heavily dependent on carbon-intensive methods.

Implications for the Steel Sector: Balancing Sustainability and Profitability

Algoma's Q3 forecast and operational progress highlight a critical tension in the steel industry: the need to balance sustainability with profitability. While the company's EAF transition is a model for green steelmaking, its negative EBITDA underscores the financial risks of such a shift. The E3G scorecard notes that near-zero emissions projects are progressing slowly, with policy coordination lagging behind technological innovation. Algoma's experience mirrors this trend, as it navigates the dual pressures of trade barriers and decarbonization.

For investors, the key question is whether Algoma's strategic investments will yield long-term value. The company's ability to leverage government support and align with global sustainability frameworks-such as the EU's Green Deal-could position it as a leader in the low-carbon steel market. However, the sector's structural challenges, including overcapacity and protectionist policies, remain significant headwinds.

Historical data on ALGO's earnings performance from 2022 to 2025 provides additional context for investors. For instance, in Q3 2022, ALGO reported a narrower-than-expected loss of 58 cents per share, yet its shares fell 1.6% post-earnings, underperforming the S&P 500; these outcomes are reflected in the backtest results. While analysts remain cautiously optimistic about a potential breakout, the mixed historical response to earnings underscores the importance of aligning strategic investments with both operational resilience and market sentiment.

Conclusion

Algoma Steel's Q3 2025 forecast is a microcosm of the steel sector's broader struggles and opportunities. While the company's EAF project demonstrates operational resilience and a commitment to sustainability, its financial performance reflects the sector's vulnerability to trade policies and excess capacity. For investors, the path forward hinges on Algoma's ability to scale its green steel initiatives, secure stable domestic demand, and navigate a fragmented global regulatory environment. As the industry grapples with decarbonization and protectionism, Algoma's journey offers both cautionary lessons and a blueprint for adaptation.

Comentarios

Aún no hay comentarios