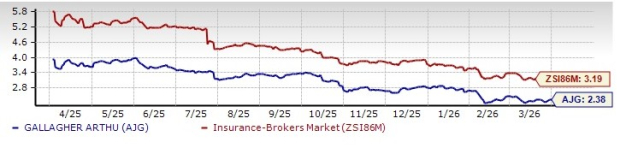

AJG Stock Trading at a Discount to Industry at 2.38X: Time to Hold?

Shares of Arthur J. Gallagher & Co. AJG are trading at a discount compared with the Zacks Brokerage Insurance industry. Its forward price-to-book value of 2.38X is lower than the industry average of 3.19X, the Finance sector’s 4.08X and the Zacks S&P 500 composite’s 7.73X.

Shares of other insurers like Erie Indemnity Company ERIE and Willis Towers Watson Public Limited Company WTW are trading at a multiple higher than the industry average, while Brown & Brown, Inc. BRO is trading at a discount.

Image Source: Zacks Investment Research

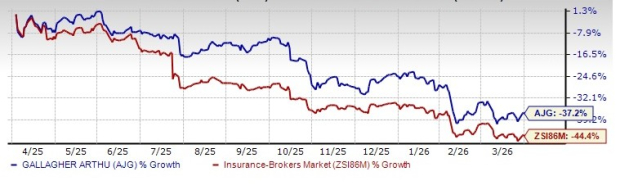

Shares of Arthur JAJG--. Gallagher have lost 37.2% in the past year compared with the industry’s decline of 44.4%.

Image Source: Zacks Investment Research

The insurer has a market capitalization of $55.62 billion. The average volume of shares traded in the last three months was 2.4 million.

AJG’s Growth Projection Encourages

The Zacks Consensus Estimate for Arthur J. Gallagher’s 2026 earnings per share indicates a year-over-year increase of 23.3%. The consensus estimate for revenues is pegged at $16.73 billion, implying a year-over-year improvement of 21.3%. The consensus estimate for 2027 earnings per share and revenues indicates an increase of 11.5% and 9.4%, respectively, from the 2026 estimates.

Earnings of Arthur J. Gallagher grew 18.1% in the last five years, better than the industry average of 13.9%. The long-term earnings growth is expected to be 15.2%, better than the industry average of 12.1%.

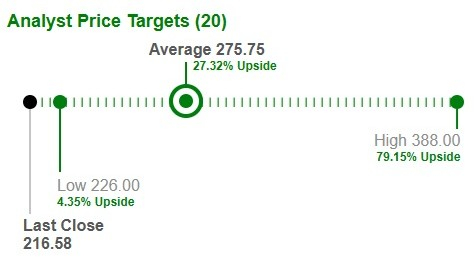

Target Price Reflects Potential Upside

Based on short-term price targets offered by 20 analysts, the Zacks average price target is $275.75 per share. The average indicates a potential 27.3% upside from the last closing price.

Image Source: Zacks Investment Research

Factors Impacting AJG

Arthur J. Gallagher remains focused on generating both organic (particularly international) and inorganic growth and is, thus, tapping into growth opportunities worldwide. This, coupled with solid retention and improving renewal premiums across all major geographies and most product lines, bodes well for growth.

In the Risk Management segment, AJGAJG-- expects about 7% organic growth for 2026. AJG expects the full-year adjusted EBITDAC margin to range from 21% to 22%, up slightly from December expectations. In the Brokerage segment, AJG expects organic growth of around 5.5% for 2026, with projected underlying margin expansion of 40-60 basis points.

AJG’s revenues are geographically diversified with strong domestic and international operations. International contributes about one-third of revenues. Given the number and size of its non-U.S. acquisitions, AJG expects international contributions to its total revenues to trend upward.

Its inorganic growth story is impressive. AJG completed approximately 780 acquisitions from Jan. 1, 2002, through Dec. 31, 2025. Revenue growth rates generally ranged from 5% to 18% for 2025 acquisitions. In 2025, AJG completed 33 acquisitions, representing around $3.5 billion of annualized revenues of businesses acquired in 2025. Looking at the pipeline, AJG has around 40 term sheets signed or being prepared, representing around $350 million of annualized revenues.

AJG’s Capital Deployment

A robust capital position over the years reflects its financial flexibility. Banking on its capital position, AJG distributes wealth to shareholders through dividend hikes and share repurchases. In the first quarter of 2026, the dividend was raised by 7.6%, witnessing a three-year CAGR (2020-2025) of 7.6%. Arthur J. Gallagher’s current dividend yield is 1% and has a $1.5 billion share buyback program in place.

Risk

Arthur J. Gallagher has been experiencing an increase in expenses due to higher compensation, depreciation, amortization and operating expenses that have been eroding margins.

Arthur J. Gallagher’s return on equity of 12.1% is lower than the industry average of 19.1%. Also, the trailing 12-month return on invested capital was 7.1%, lower than the industry average of 7.5%. This shows the company’s inefficiency in managing shareholders’ funds. Also, the debt level is significant, which raises interest payouts and results in low times interest earned.

Conclusion

AJG continues to benefit from solid retention, improving renewal premiums, and organic and inorganic growth. The Risk Management and Brokerage segments should continue to witness significant growth. A robust capital position over the years reflects its financial flexibility. Its impressive dividend history, as well as solid growth projections, are other positives.

Given the escalating expenses and unfavorable return on capital, it is better to stay cautious about this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Arthur J. Gallagher & Co. (AJG): Free Stock Analysis Report

Brown & Brown, Inc. (BRO): Free Stock Analysis Report

Erie Indemnity Company (ERIE): Free Stock Analysis Report

Willis Towers Watson Public Limited Company (WTW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios