AI-Driven Tech Stocks: Market Leadership, Valuation Dynamics, and the Rise of Wealth Concentration

The artificial intelligence (AI) revolution has reshaped the global tech landscape, creating unprecedented wealth and consolidating power among a handful of market leaders. As of September 2025, the AI-driven tech sector is dominated by a narrow group of companies whose valuations dwarf the sector's total market capitalization, raising critical questions about wealth concentration and investment risk.

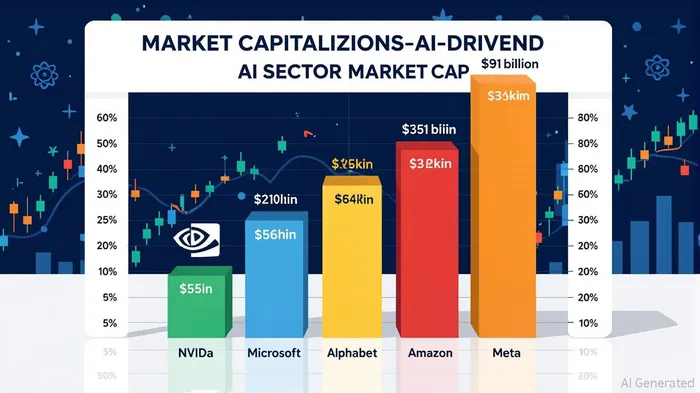

Market Leadership: The "Big Five" and Their Valuation Trajectories

Nvidia, MicrosoftMSFT--, AlphabetGOOGL--, AmazonAMZN--, and MetaMETA-- have emerged as the uncontested titans of the AI era. NvidiaNVDA--, the undisputed leader in AI chip development, commands a staggering $4.25 trillion market cap, driven by its Blackwell architecture and dominance in AI infrastructure[1]. Microsoft follows closely at $3.77 trillion, fueled by AI integration across Azure, Microsoft 365, and its strategic partnership with OpenAI[1]. Alphabet (Google) holds $2.58 trillion in value, leveraging AI in search, advertising, and cloud services[1], while Amazon and Meta round out the top five with $2.42 trillion and $1.85 trillion, respectively[1].

These valuations reflect explosive growth: Nvidia's revenue surged 94% year-on-year in Q4 FY25[3], and Meta's open-source AI models have driven record profits[3]. Collectively, these five companies account for over $15 trillion in market capitalization—a figure that dwarfs the entire AI sector's reported $391 billion total market cap[2]. This discrepancy underscores a critical nuance: the "Big Five" are not solely AI companies but tech conglomerates whose AI divisions now anchor their valuations[1].

Wealth Concentration: A Sector Built on a Few Giants

The concentration of wealth in the AI sector is staggering. If we isolate the AI-specific segments of these companies (e.g., Nvidia's chips, Microsoft's Azure AI, Alphabet's Gemini models), their combined value likely exceeds $391 billion—the sector's total market cap[2]. This suggests that the leading firms' AI operations represent the entire sector's value, with no room for smaller players or emerging innovators.

For context, U.S. private AI investment alone reached $109.1 billion in 2024[3], yet the lion's share of this capital has flowed into the ecosystems of the "Big Five." Startups and niche AI firms face an uphill battle, as the dominant players control critical infrastructure (e.g., cloud platforms, chip manufacturing) and data resources[1]. This dynamic mirrors the dot-com era, where a handful of companies captured the lion's share of the internet's value.

Valuation Dynamics: Justified or Overinflated?

The sky-high valuations of AI leaders are justified by their revenue growth and strategic positioning. Nvidia's Blackwell architecture has become the industry standard for AI training[3], while Microsoft's Azure AI and Amazon's AWS dominate cloud-based AI workloads[1]. Alphabet's Gemini models and Meta's open-source approach further cement their relevance in a rapidly evolving market[3].

However, skepticism persists. Critics argue that these valuations assume perpetual dominance in a sector prone to disruption. For instance, open-source AI models and alternative chip architectures could erode Nvidia's margins[3]. Similarly, regulatory scrutiny of Big Tech's AI monopolies may intensify, as seen in the EU's AI Act and U.S. antitrust debates[1].

The Road Ahead: Implications for Investors

The AI sector's trajectory is clear: it is projected to grow to $1.81 trillion by 2030[3], with the "Big Five" likely to capture the majority of this value. For investors, this presents a paradox. Diversifying across smaller AI firms carries high risk, while overexposure to the dominant players exposes portfolios to regulatory and technological shocks.

A balanced approach is advisable. Allocating to the "Big Five" for their growth potential while hedging with AI-focused ETFs or niche innovators could mitigate risk. Additionally, monitoring regulatory developments and supply chain dynamics (e.g., chip manufacturing bottlenecks) will be critical[1].

Conclusion

The AI-driven tech sector is a tale of two extremes: explosive growth and extreme concentration. While the "Big Five" have redefined innovation, their dominance raises concerns about market fairness and long-term sustainability. For investors, the challenge lies in balancing the allure of these titans with the need for diversification in a sector that promises to reshape the global economy.

Comentarios

Aún no hay comentarios