AI-Driven Growth in Asia-Pacific Tech Services: A Strategic Buy Opportunity in Q3 2025

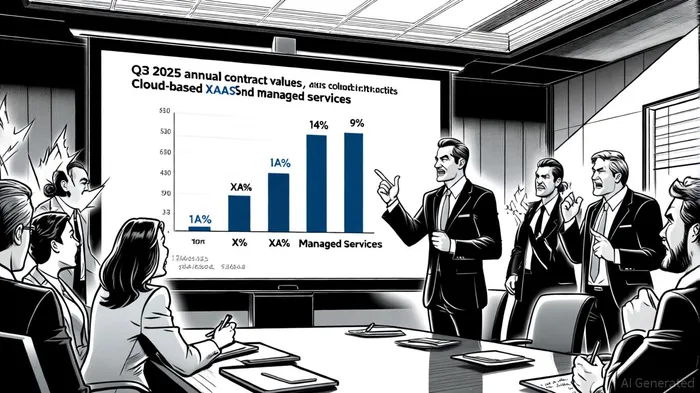

The Asia-Pacific technology services sector is undergoing a seismic shift in Q3 2025, driven by AI adoption and cloud infrastructure expansion. According to the ISG Index™, the region's combined market for cloud-based XaaS and managed services surged 10% year-over-year, with XaaS spending alone jumping 14% to $4.9 billion [1]. This growth is fueled by enterprises migrating workloads to GPU-rich cloud environments to support AI development, with infrastructure-as-a-service (IaaS) and software-as-a-service (SaaS) leading the charge. IaaS ACV rose 13% to $4.3 billion, while SaaS ACV grew 18% to $563 million [1].

In contrast, managed services ACV contracted 9% to $849 million in Q3 2025, reflecting macroeconomic caution and geopolitical uncertainties [1]. However, smaller managed services contracts ($5 million–$10 million) increased by 39%, signaling a potential rebound in discretionary spending [1]. This divergence underscores a critical investment opportunity: tech services firms with strong AI and cloud exposure are outpacing peers, while undervalued leaders in these high-growth segments offer compelling entry points.

AI and Cloud: The Twin Engines of Growth

The Asia-Pacific region's AI infrastructure spending is accelerating at an unprecedented pace. According to IDC, public cloud services in the region are projected to grow at a 19.8% CAGR from 2025 to 2029, reaching $250 billion by 2029 [3]. This surge is driven by governments mandating "cloud-first" strategies and enterprises adopting hybrid cloud architectures to balance data sovereignty with AI scalability. For instance, Malaysia's MyGovCloud initiative and South Korea's AI-driven smart city projects are reshaping regional demand [5].

The ISG Index™ forecasts 25% growth for cloud-based XaaS in 2025, dwarfing the 1.3% projected for managed services [1]. This trend is further amplified by the Asia-Pacific's $1.4 trillion ICT spending target for 2025, with AI and machine learning accounting for a significant share [6]. As businesses prioritize AI-driven productivity and customer experience, cloud platforms are becoming the backbone of digital transformation.

Identifying Undervalued Leaders

While the ISG Index™ does not explicitly name undervalued companies, financial metrics and market positioning reveal actionable insights. For example, firms with low price-to-earnings (P/E) ratios relative to their cloud/AI revenue growth are prime candidates. In Q4 2024, the Asia-Pacific tech services market generated a record $19.7 billion in ACV, with XaaS contributing $15.3 billion-a 13% increase from 2023 [2]. Companies that allocate capital to AI infrastructure provisioning, such as GPU-accelerated cloud instances, are likely to outperform in this environment.

Key indicators to watch include:

1. Revenue Growth in AI/Cloud Segments: Firms with double-digit growth in IaaS/SaaS, like those highlighted in the ISG Index™, are better positioned to capitalize on AI workloads.

2. P/E Ratios Below Industry Averages: Undervalued leaders often trade at discounts to peers, offering margin of safety despite robust growth.

3. Geographic Diversification: Companies with exposure to high-growth markets like India, Indonesia, and Southeast Asia are poised to benefit from rising smartphone penetration and startup ecosystems [4].

Risks and Mitigation

Challenges such as fragmented data-residency laws and a shortage of certified cloud talent could slow adoption [5]. However, these risks are mitigated by long-term tailwinds, including government incentives for AI innovation and the proliferation of 5G-enabled edge computing. For instance, Japan's Ministry of Economy, Trade, and Industry (METI) has allocated $2 billion to AI infrastructure in 2025, while China's State Council is prioritizing AI-driven manufacturing [6].

Strategic Outlook

Investors should prioritize tech services firms with:

- High AI Infrastructure Exposure: Those offering GPU-optimized cloud solutions or AI model training platforms.

- Scalable XaaS Portfolios: Companies with recurring revenue streams from SaaS and IaaS.

- Strong Balance Sheets: Firms with low debt and high cash reserves to fund R&D in AI and cloud.

The Asia-Pacific tech services sector is at an inflection point. As AI adoption accelerates and cloud demand outpaces managed services, undervalued leaders with strategic AI/cloud exposure are set to deliver outsized returns. For investors, Q3 2025 presents a rare window to capitalize on this transformation before broader market recognition inflates valuations.

Comentarios

Aún no hay comentarios