Aetna and Humana's Retreat from Medicare Advantage: Sector Ripple Effects and Valuation Opportunities

The Medicare Advantage (MA) sector is undergoing a seismic shift in 2025, driven by the strategic retreats of industry giants Aetna and HumanaHUM--. These exits, fueled by unsustainable financial pressures and regulatory headwinds, are reshaping the competitive landscape and creating valuation opportunities for investors. As the sector consolidates, the ripple effects on beneficiaries, insurers, and the broader healthcare economy demand careful analysis.

The Drivers of Retreat: Financial Pressures and Regulatory Shifts

Aetna and Humana's exits from Medicare Advantage are emblematic of a broader industry reckoning. According to a Prepare for Medicare report, Aetna is closing nearly 90 MA plans across 34 states in 2026, citing rising medical costs and reduced government reimbursements as key factors. Similarly, Humana's decision to exit 13 markets in the Southeast-impacting 560,000 members-reflects a strategic pivot toward profitability over growth, as detailed in PolicyGuide coverage on Humana exits. These moves are not isolated; UnitedHealthcare, the sector's largest player, has also pulled back from 16 U.S. counties, affecting 180,000 members, according to a Reuters report.

The financial pressures are multifaceted. The Inflation Reduction Act (IRA) has reduced reimbursement rates for insurers, while the transition to the v28 Risk Adjustment model has strained revenue streams, as noted in an Oliver Wyman analysis. Additionally, medical utilization rates have surged, with UnitedHealthcare CEO Tim Noel admitting that 2025 pricing assumptions were "well short of actual medical costs," leading to an additional $3.6 billion in losses from its MA segment, as reported in a Fierce Healthcare article. These challenges have forced insurers to prioritize sustainable operations over aggressive expansion.

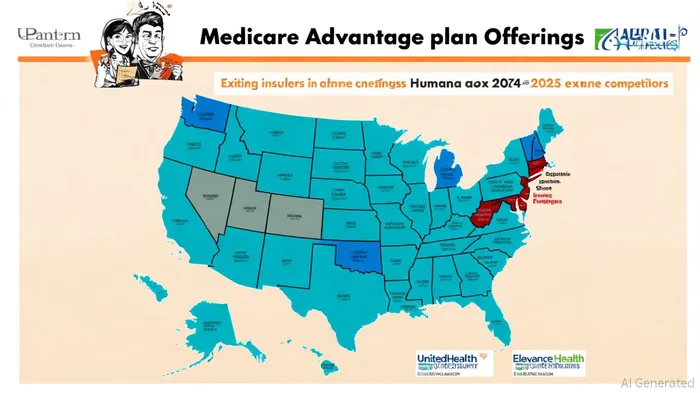

Market Concentration and Competitive Reconfiguration

The MA market is already highly concentrated, with UnitedHealthcare and Humana dominating 59% of enrollment in 2024, according to a KFF analysis. Aetna and Humana's exits are accelerating this trend, creating a vacuum that remaining players are poised to fill. UnitedHealthcare, for instance, is leveraging its scale to expand in exiting markets, while Elevance HealthELV-- (formerly Anthem) is refocusing on HMO and dual-special needs plans, as covered in a Fierce Healthcare report on Elevance.

Data from a HealthWorks AI analysis reveals that the total number of MA plans has declined for the first time, from 5,805 in 2024 to 5,682 in 2025, signaling a period of consolidation. Smaller insurers like Cigna and Centene have taken a more cautious approach, with Cigna selling its entire MA portfolio to Health Care Service Corp, according to a DistilInfo report. This reconfiguration is likely to reduce beneficiary choice and increase premiums, as insurers shift to more restrictive HMO networks and higher out-of-pocket costs, a trend documented by Healthcare Finance News.

Valuation Impacts and Investment Opportunities

The strategic exits are creating both challenges and opportunities for investors. UnitedHealth GroupUNH--, the sector's bellwether, has seen its stock face short-term volatility due to its $3.6 billion MA-related losses reported earlier. However, analysts remain cautiously optimistic, with a "Moderate Buy" consensus and a price target of $355.77 (up 3.61% from its current price) mentioned in coverage of the company. This optimism stems from UnitedHealthcare's focus on managed care products and vertical integration with Optum clinics, which could offset MA headwinds.

Elevance Health, the fourth-largest MA insurer, has also seen its stock dip by 4% following its decision to exit standalone Part D and underperforming MA markets; the company's pivot to high-margin HMO and dual-eligible special needs plans (D-SNPs) positions it to capture growth in high-need populations. For investors, the key is to differentiate between insurers that are strategically retrenching and those that are merely reacting to short-term pressures.

The market exits also present opportunities for niche players and regional insurers. Devoted Health, for example, has expanded its MA plan offerings by 62% in 2025, targeting high-need populations through specialized D-SNPs, according to the HealthWorks AI analysis cited above. Similarly, for-profit insurers are capturing 56% of the sector's year-over-year growth, suggesting that agility and specialization may outperform traditional scale in the new MA landscape (as reported by DistilInfo).

Looking Ahead: A Sector in Transition

The MA market is entering a phase of structural transformation. While enrollment growth has slowed to 4% in 2025 (down from 7% in 2023), the sector remains resilient due to its favorable economics compared to other healthcare segments, a trend highlighted by Healthcare Finance News. However, the focus is shifting from growth-at-all-costs to profitability and sustainability. Insurers that can optimize risk-based strategies, leverage vertical integration, and navigate regulatory changes will emerge stronger.

For beneficiaries, the trade-off is clear: reduced plan options and higher costs in exchange for insurer stability. For investors, the challenge lies in identifying companies that can navigate this transition without sacrificing long-term value. The exits of Aetna and Humana are not the end of the MA story-they are a catalyst for a new era of consolidation, innovation, and strategic repositioning.

Comentarios

Aún no hay comentarios