ADG126: A Game-Changer in MSS Colorectal Cancer Immunotherapy and Its Implications for Adagene’s Valuation

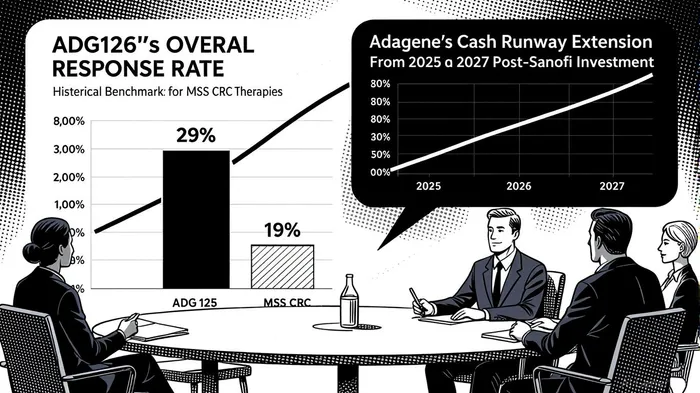

The biotech sector has long been a high-stakes arena for innovation, but few developments in recent years have captured investor attention like Adagene’s ADG126 (muzastotug). This masked anti-CTLA-4 antibody, currently in Phase 1b/2 trials for microsatellite stable colorectal cancer (MSS CRC), has emerged as a potential breakthrough in a disease landscape historically resistant to immunotherapy. With a confirmed overall response rate (ORR) of 29% in MSSMSS-- CRC patients and a median overall survival (OS) of 19.4 months in the 10 mg/kg cohort, ADG126 is not just a clinical milestone—it’s a valuation catalyst for AdageneADAG-- (NASDAQ: ADAG).

Clinical Progress: A Durable Safety-Efficacy Balance

ADG126’s mechanism of action—conditional activation in the tumor microenvironment—sets it apart from traditional CTLA-4 inhibitors. By masking the antibody until it reaches the tumor site, Adagene has engineered a drug that blocks CTLA-4 with precision while minimizing systemic toxicity. According to a report by Adagene, the 20 mg/kg dose administered every six weeks (Q6W) demonstrated less than 20% Grade 3 adverse events, a stark contrast to the higher toxicity profiles of approved CTLA-4 inhibitors like ipilimumab [1].

The Phase 1b/2 trial results are equally compelling. At the 20 mg/kg dose, six responders have remained on treatment for over 40 weeks, with a median OS not yet reached in this cohort [1]. For context, historical benchmarks for MSS CRC therapies typically report median OS between 10.8 and 12.1 months [2]. ADG126’s ability to extend survival while maintaining safety is a rare combination in oncology, particularly for a disease where immunotherapy has historically failed.

Market Potential: MSS CRC as a $19B Opportunity

The MSS CRC market is a $19.4 billion segment within the broader $30 billion global colorectal cancer (CRC) market, driven by an aging population and rising incidence rates [3]. Adagene’s alignment with the FDA on Phase 2 and Phase 3 trial designs positions ADG126 to capture a significant share of this market. The drug’s favorable therapeutic index—demonstrated by its 29% ORR and 8.5-month median progression-free survival (PFS) in patients without liver metastases—suggests it could outperform existing therapies [4].

Moreover, the MSS CRC segment is highly competitive but underserved. While Merck’s pembrolizumab (KEYTRUDA) and Roche’s atezolizumab dominate the PD-1/PD-L1 space, their efficacy in MSS CRC remains limited. A recent study on botensilimab plus balstilimab (anti-CTLA-4 and anti-PD-1) reported a mere 17% ORR and 7.4-month median OS in MSS mCRC patients [5]. ADG126’s superior outcomes, combined with its unique mechanism, position it as a best-in-class candidate.

Strategic Partnerships and Financial Resilience

Adagene’s partnership with SanofiSNY--, which includes a $25 million investment and a Phase 1b/2 trial in over 100 advanced solid tumor patients, underscores the drug’s potential [2]. This collaboration not only validates ADG126’s clinical promise but also extends Adagene’s cash runway into 2027, a critical factor for a clinical-stage biotech. As of June 30, 2025, Adagene reported $62.8 million in cash, with R&D expenses declining 18% year-over-year to $12.0 million, reflecting operational efficiency [6].

Valuation metrics further highlight Adagene’s appeal. The company trades at a price-to-book (PB) ratio of 2.7x, below its peer average of 2x, and is undervalued at $2.2 per share compared to an estimated fair value of $53.33 [7]. While its credit risk remains elevated (probability of default: 2.152 as of August 2025), this has improved markedly from a peak of 6.227 in early 2023, reflecting growing confidence in its pipeline [8].

Conclusion: A Strategic Investment in Next-Gen Immuno-Oncology

ADG126 represents more than a clinical advancement—it’s a strategic inflection pointIPCX-- for Adagene. With Phase 2 enrollment set to begin in late 2025 and a robust cash runway, the company is well-positioned to capitalize on a $19.4 billion market. For investors, the combination of a best-in-class therapeutic profile, favorable safety data, and a de-risked financial outlook makes Adagene a compelling play in next-generation immuno-oncology.

Source:

[1] Adagene Announces Updated Data from Phase 1b/2 Study of ADG126 [https://investor.adagene.com/news-releases/news-release-details/adagene-announces-updated-data-phase-1b2-study-muzastotug-adg126/]

[2] Adagene Reports Six Months 2025 Financial Results [https://www.globenewswire.com/news-release/2025/08/12/3132109/0/en/Adagene-Reports-Six-Months-2025-Financial-Results-and-Provides-Corporate-Updates.html]

[3] Global Colorectal Cancer Market Size Report [https://www.custommarketinsights.com/report/colorectal-cancer-market/]

[4] Adagene Presents Results at ESMO Congress [https://www.stocktitan.net/news/ADAG/adagene-presents-results-at-esmo-congress-that-show-best-in-class-9950fnd5aveh.html]

[5] Botensilimab plus Balstilimab in MSS mCRC [https://www.nature.com/articles/s41591-024-03083-7]

[6] Adagene 2025 Financial Results [https://finance.yahoo.com/news/adagene-reports-six-months-2025-200500552.html]

[7] Adagene Valuation Analysis [https://simplywall.st/stocks/us/pharmaceuticals-biotech/nasdaq-adag/adagene/valuation]

[8] Adagene Credit Risk Profile [https://martini.ai/pages/research/Adagene-fdca23adf095e62e7f5ec65a3e49162f]

Comentarios

Aún no hay comentarios