Here's Why You Should Add Merit Medical Stock to Your Portfolio Now

Merit Medical Systems, Inc. MMSI is well-poised for growth in the coming quarters, courtesy of its strong product portfolio. The optimism, led by a solid performance in 2025 and its continued spending on research and development (R&D), is expected to contribute further. However, tariffs and trade policy headwinds, and China macro pressure persist.

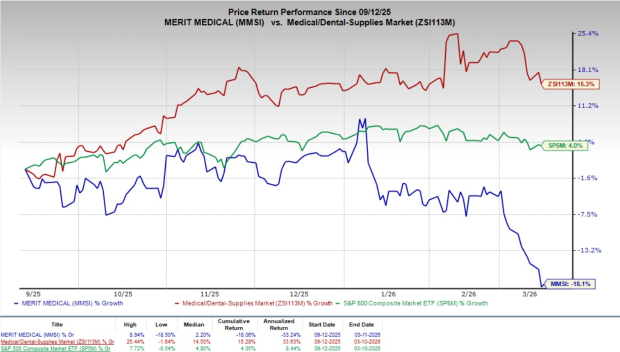

This Zacks Rank #2 (Buy) company’s shares have declined 18.1% over the past six months against the industry’s 15.3% growth. The S&P 500 has climbed 4% during the same time frame.

The renowned medical device provider has a market capitalization of $4.14 billion. The company projects 9.5% growth for the next five years and expects to maintain its strong performance going forward. It delivered an average earnings surprise of 13.2% for the past four quarters.

Image Source: Zacks Investment Research

Let us delve deeper.

MMSI’s Growth Drivers

Momentum in Cardiovascular & Peripheral Intervention Devices: The cardiovascular segment continues to be the primary engine of growth for Merit MedicalMMSI--, delivering strong performance, led by cardiac intervention and peripheral intervention products. In fourth-quarter 2025, cardiac intervention sales increased 21%, supported by strong demand for electrophysiology, cardiac rhythm management, angiography and vascular access products, including the Prelude SNAP, Ventrax delivery system and Prelude radial sheath platforms.

Peripheral intervention products delivered double-digit growth of 13%, with radar localization and delivery systems increasing more than 25% year over year, reflecting broad-based adoption across embolotherapy, drainage, angiography and access product categories. These trends highlight strong procedural demand and the strength of the company’s cardiovascular portfolio.

For 2026, management expects continued growth, driven by rising cardiovascular procedure volumes globally, with cardiovascular solutions remaining a central contributor to the company’s projected 5-7% constant-currency revenue growth and portfolio expansion across interventional procedures.

Expansion of Higher-Growth Therapeutic Products & Innovation:Merit Medical highlighted strong momentum from its therapeutic product portfolio, which represents a faster-growing segment of the business compared with its foundational procedural products. Management explained that the company’s portfolio is broadly divided into two groups: foundational products used primarily for vascular access, and enabling procedures and therapeutic products designed to treat disease.

Foundational products account for two-thirds of total revenues and saw a 6% CAGR over the last three years. In contrast, therapeutic products represent about one-third of revenues but have grown significantly faster, witnessing a 19% CAGR over the same period and seeing a 11% CAGR on an organic basis.

These therapeutic offerings include devices used in embolotherapy, tumor treatment, vascular therapies and radar localization systems, many of which address large and expanding treatment markets. This category has been an important contributor to the company’s overall growth and reflects increasing physician adoption of devices that treat disease rather than simply enable procedures.

For 2026, the company intends to continue prioritizing innovation and investment in these therapeutic platforms while combining them with its foundational product portfolio to strengthen its position as a full-line supplier and support sustained revenue growth.

Product Innovation & Strategic Acquisitions: Merit Medical continued to drive growth through a combination of product innovation and acquisitions in 2025. Internally developed products remain a consistent contributor to performance, noting 10% of revenue growth in the company’s two largest categories, Cardiac Intervention and Peripheral Intervention.

Several recently launched devices supported demand in 2025, including the Prelude SNAP system, Ventrax Delivery System, Prelude radial sheath and the SCOUT radar localization system, which have been gaining adoption across the procedural markets.

Alongside internal innovation, MMSIMMSI-- benefited from contributions from recent acquisitions. In fourth-quarter 2025, total revenues included $10.8 million in inorganic sales from acquired products, including lead management products from Cook Medical, BioLife Delaware LLC and the C2 CryoBalloon device from PENTAX of America.

Management expects these acquisitions to contribute $13-$15 million in revenues in 2026, while relying on internally developed product innovation and disciplined M&A to expand its product portfolio and support growth across its key procedural platforms.

Key Challenges for MMSI Stock

Tariffs & Trade Policy Pressuring Margins: Tariffs were a headwind to the gross margin performance in fourth-quarter 2025, representing a 112-bps year over year incremental impact. Management expects this pressure to prevail in 2026. In its guidance for 2026, management said that non-GAAP EPS assumptions include a 12-month tariff impact of $15 million, or 19 cents per share, compared with $9 million, or 12 cents per share, realized during the last eight months of 2025.

The company addressed the expected near-term impacts, stating that tariffs would create an 80-bps or $3-million gross margin impact in first-quarter 2026. The tariff assumptions are based on tariff policies that were in place prior to the recent U.S. Supreme Court decision and do not include the potential impacts of new tariffs, creating uncertainty around cost pressures and margin performance.

OEM Weakness & China Macro Pressure: Merit Medical experienced notable weakness in its OEM business, particularly in fourth-quarter 2025. OEM product sales declined 15% year over year in fourth-quarter 2025, significantly below the low-single-digit rise that the company had expected. Management attributed the softer United States performance to customer inventory destocking, which reduced near-term order volumes from OEM partners. Outside the United States, demand was affected by broader macro-economic pressures, particularly in China, where market conditions and healthcare policy changes weighed on growth.

China revenues declined in 2025 due to the ongoing impacts of the country’s volume-based procurement program, which continues to pressure pricing across medical device categories. Despite this near-term weakness and quarter-to-quarter volatility, management emphasized that the OEM segment remains strategically important as it provides manufacturing scale and capacity utilization. The company expects the OEM business to return to its normalized growth profile in the mid- to high-single-digit range, although management acknowledged that short-term fluctuations may continue as inventory levels normalize and macro conditions in international markets stabilize.

Merit Medical Systems, Inc. Price

Merit Medical Systems, Inc. price | Merit Medical Systems, Inc. Quote

Estimate Trend

MMSI is witnessing a positive estimate revision trend for 2026. In the past 60 days, the Zacks Consensus Estimate for earnings per share (EPS) has moved 1.25% north to $4.05.

The Zacks Consensus Estimate for the company’s first-quarter 2026 revenues is pegged at $376.8 million, suggesting a 6.03% rise from the year-ago reported number. The consensus mark for EPS is pegged at 85 cents, implying a 1.2% decline from the prior-year reported figure.

Other Stocks to Consider

Some other top-ranked stocks from the broader medical space are Intuitive Surgical ISRG, Cardinal Health CAH and The Cooper Companies COO.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term earnings growth rate of 15.7%. ISRG’s earnings surpassed estimates in the trailing four quarters, the average surprise being 13.2%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Intuitive Surgical’s shares have gained 9.6% against the industry’s 4.7% decline over the past six months.

Cardinal Health, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 15%. CAH’s earnings surpassed estimates in the trailing four quarters, the average surprise being 9.3%.

Cardinal Health’s shares have gained 41.5% compared with the industry’s 15.3% growth over the past six months.

The Cooper Companies, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 8.4%. COO’s earnings surpassed estimates in the trailing four quarters, the average surprise being 4.1%.

The Cooper Companies’ shares have gained 10.6% compared with the industry’s 15.3% growth over the past six months.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI): Free Stock Analysis Report

The Cooper Companies, Inc. (COO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios