Here's Why You Should Add Cardinal Health Stock to Your Portfolio Now

Cardinal Health CAH is well positioned for continued growth, thanks to the expansion of its speciality portfolio. The firm delivered strong fiscal second-quarter results, fueled by robust demand in pharmaceutical distribution and accelerating specialty services. Growth in theranostics, at-home solutions and logistics businesses, alongside improving medical segment performance, continues to strengthen CAH’s long-term earnings outlook.

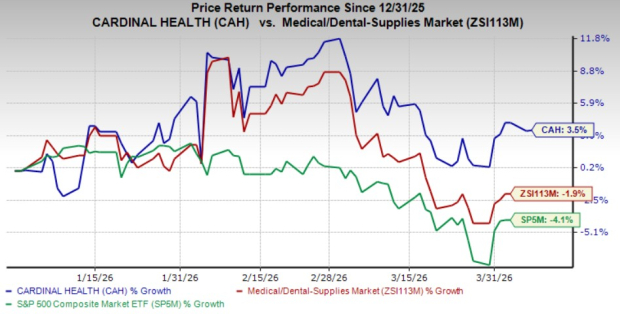

This Zacks Rank #2 (Buy) company’s shares have gained 3.5% so far this year against the industry’s1.9% decline. The S&P 500 has decreased 4.1% during the same time frame.

Image Source: Zacks Investment Research

The leading provider of healthcare services and products has a market capitalization of $50.03 billion. It projects 15% growth over the next five years and expects to witness continued improvement in its business going forward. Cardinal Health’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 9.3%.

Let’s delve deeper.

Positive Drivers

Strong Specialty and Pharmaceutical Segment Momentum: Cardinal Health delivered robust performance in its Pharmaceutical and Specialty Solutions segment, with 19% revenue and 29% profit growth, supported by strong demand across brand, specialty and generics. Specialty remains the key structural driver, with revenues expected to exceed $50 billion in fiscal 2026.

Growth is further supported by MSO platforms, biopharma services, and continued expansion in oncology and urology. This diversified specialty ecosystem enhances margin mix and positions the company to capitalize on high-growth therapeutic areas with stronger pricing and service charges.

Broad-Based Segment Performance Reflecting Strength: All five operating segments delivered double-digit profit growth, underscoring the resilience and balance of Cardinal Health’s portfolio. Beyond pharma, strong contributions from Nuclear and Precision Health, at-Home Solutions and OptiFreight Logistics highlight multiple growth engines supported by favorable secular trends, such as site-of-care shifts and precision medicine adoption. This diversification reduces reliance on core drug distribution, enabling more stable earnings growth and providing multiple levers for expansion across varying healthcare demand cycles.

Operating Leverage and Cost Discipline: Cardinal Health demonstrated strong operating leverage, with gross profit rising 24% compared with 16% SG&A growth, resulting in a 38% increase in operating earnings.Organic SG&A growth remained in the low single digits, reflecting disciplined cost control despite ongoing investments. Efficiency initiatives across distribution, digital infrastructure and supply-chain optimization continue to enhance productivity. This cost discipline, combined with favorable product mix (especially specialty), supports sustained margin expansion even as the company continues to invest for long-term growth.

Downsides

Dependence on Specialty Growth: While specialty is a key growth driver, Cardinal Health’s increasing reliance on this segment introduces concentration risk. A significant portion of profit expansion is tied to specialty distribution, MSOs and biopharma services. Any disruption in specialty drug pricing, reimbursement dynamics or manufacturer relationships could disproportionately impact growth. Competitive intensity in specialty services is rising, requiring continued investment to maintain differentiation, which could pressure margins if growth moderates.

Regulatory and Pricing Pressures: Cardinal Health remains exposed to evolving policy frameworks, including Inflation Reduction Act-related pricing changes, which may reduce drug list prices (WAC) over time.

While management expects to offset margin impacts through contractual adjustments, revenues could still be affected due to lower pricing pass-through. This creates a structural headwind for top-line growth and introduces uncertainty around long-term revenue visibility, particularly as additional policy changes emerge in the coming years.

GMPD Segment Recovery Still Fragile: Although the GMPD segment showed improvement, with profit increasing to $37 million, growth remains modest (3% revenue growth) and partially influenced by timing-related inventory restocking.

Tariffs continue to exert pressure on profitability, and normalization of distributor buying patterns could impact near-term performance. While operational improvements are evident, the segment’s recovery is still in progress and vulnerable to external cost pressures and demand variability.

Estimate Trend

Cardinal Health has been witnessing an improving estimate revision trend for 2026. Over the past 60 days, the Zacks Consensus Estimate for earnings per share (EPS) has improved 1.6% to $10.31.

The Zacks Consensus Estimate for third-quarter fiscal 2026 revenues is pegged at $62.42 billion, indicating a 13.7% improvement from the year-ago reported number. The Zacks Consensus Estimate for EPS is pinned at $2.80, implying a year-over-year gain of 19.2%.

Other Stocks to Consider

Some better-ranked stocks from the same medical industry are Pacific Biosciences of California PACB, Globus Medical GMED and Biodesix BDSX.

Pacific Biosciences of California, currently flaunting a Zacks Rank #1 (Strong Buy), reported a fourth-quarter 2025 adjusted loss per share of 12 cents, which surpassed the Zacks Consensus Estimate by 36.8%. Revenues of $45 million beat the Zacks Consensus Estimate by 9.4%. You can see the complete list of today’s Zacks #1 Rank stocks here.

PACB has an estimated earnings decline rate of 1.9% against the industry’s 11.4% improvement. The company beat earnings estimates in each of the trailing four quarters, with the average surprise being 27.7%.

Globus Medical, carrying a Zacks Rank #2 (Buy) at present, reported fourth-quarter 2025 adjusted EPS of $1.28, which outpaced the Zacks Consensus Estimate by 20.8%. Revenues of $826 million surpassed the Zacks Consensus Estimate by 4.9%.

GMED has an estimated long-term earnings growth rate of 9.6% compared with the industry’s 14% rise. The company beat earnings estimates in each of the trailing four quarters, with the average surprise being 13.2%.

Biodesix, currently carrying a Zacks Rank of 2, reported a fourth-quarter 2025 adjusted loss per share of 49 cents, which beat the Zacks Consensus Estimate by 53.33%. Revenues of $29 million beat the Zacks Consensus Estimate by 14.1%.

BDSX has an estimated earnings growth rate of 22.5% for 2026 compared with the industry’s 12% rise. The company beat earnings estimates in two of the trailing four quarters, missed in one and met in the other, with the average surprise being 16.64%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Pacific Biosciences of California, Inc. (PACB): Free Stock Analysis Report

Biodesix, Inc. (BDSX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios