Actelis Networks' Aggressive Capital-Raising Strategy: Strategic Implications and Shareholder Dilution Risks

Actelis Networks, Inc. has embarked on an aggressive capital-raising campaign in 2025, culminating in a series of equity transactions that collectively approach the 15.2 million share threshold. These moves, while critical for sustaining operations, raise significant questions about the company's strategic direction and the long-term value for shareholders.

Strategic Implications: A Race to Stabilize Liquidity

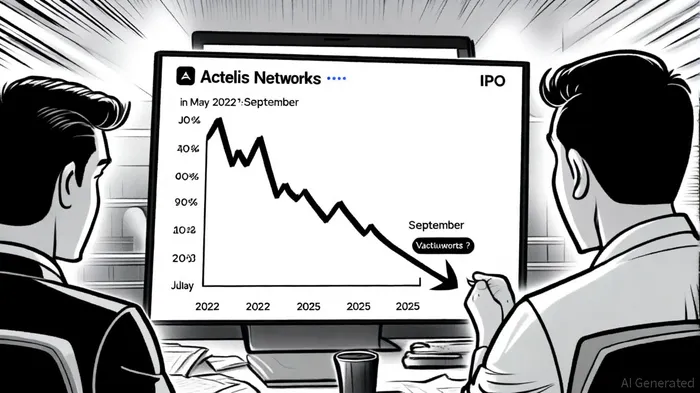

Actelis' recent transactions include the exercise of existing warrants for 4,270,197 shares at $0.37 per share and the issuance of new warrants for 6,405,296 shares at the same price, generating $1.6 million in gross proceeds, according to a GlobeNewswire release. Separately, the company secured a $30 million equity line of credit (ELOC) with White Lion Capital, issuing 3.999 million shares and pre-funded warrants at $0.2125 per share, raising $30.8 million in total proceeds, according to a MarketScreener report. These actions suggest a desperate attempt to address liquidity constraints, particularly given the stark contrast between the May 2022 IPO price of $4.00 per share and the current offerings priced at deep discounts (as reported by MarketScreener).

The strategic rationale appears to center on maintaining operational flexibility. According to the SEC filings, proceeds will be allocated to "general corporate purposes," a broad category that could include debt servicing, R&D, or market expansion, per the GlobeNewswire release. However, the lack of specificity raises concerns about whether these funds will directly address core business challenges or merely serve as a short-term bandage.

Shareholder Impact: Dilution and Erosion of Value

The most immediate consequence of Actelis' capital-raising efforts is dilution. The ELOC with White Lion alone could issue up to 19.99% of the company's outstanding shares, with a $750,000 commitment fee also paid in stock, according to an SEC filing. Compounding this, the July 2025 private placement-priced at $0.615 per share-offered additional dilution risks through exercisable warrants, as noted in the GlobeNewswire release. For context, the cumulative issuance of 15.2 million shares (across all 2025 transactions) represents a potential 50%+ increase in the company's float, depending on pre-offering share counts.

Such dilution pressures intrinsic value, particularly for long-term holders. As noted by financial analysts, "deep discount equity financings often signal distress and can erode investor confidence," a dynamic evident in Actelis' 80%+ share price decline since its IPO (per MarketScreener). Furthermore, the issuance of pre-funded warrants with near-zero exercise prices (e.g., $0.0001) creates a scenario where future shareholders could acquire stock at negligible costs, further devaluing existing stakes (as reported by MarketScreener).

Broader Industry Context and Risk Assessment

Actelis' reliance on at-the-market offerings and ELOCs mirrors trends among struggling tech firms seeking to avoid traditional debt financing. However, the company's repeated need for capital-four major transactions in 2025 alone-highlights structural weaknesses. A report by Bloomberg, summarized in a Panabee article, indicates that firms with similar financing patterns often face regulatory scrutiny and reduced M&A appeal, limiting exit options for ActelisASNS--.

Investors must also weigh the role of financial advisors. Rodman & Renshaw and H.C. Wainwright, who facilitated the September 2025 warrant inducement, received compensation for their services, raising questions about alignment with shareholder interests (per the GlobeNewswire release).

Conclusion: A High-Risk, High-Stakes Scenario

Actelis Networks' 2025 capital-raising efforts underscore a critical juncture. While the company has secured immediate liquidity, the strategic trade-off involves significant dilution and a weakened balance sheet. For shareholders, the priority should be monitoring how these funds are deployed and whether they catalyze meaningful growth or merely delay insolvency. As the market watches, the question remains: Can Actelis transform these short-term fixes into a sustainable value proposition, or will they become a cautionary tale of over-leveraged equity financing?

Comentarios

Aún no hay comentarios