ACM Research: Navigating the Tension Between Short-Term Volatility and Long-Term Semiconductor Growth

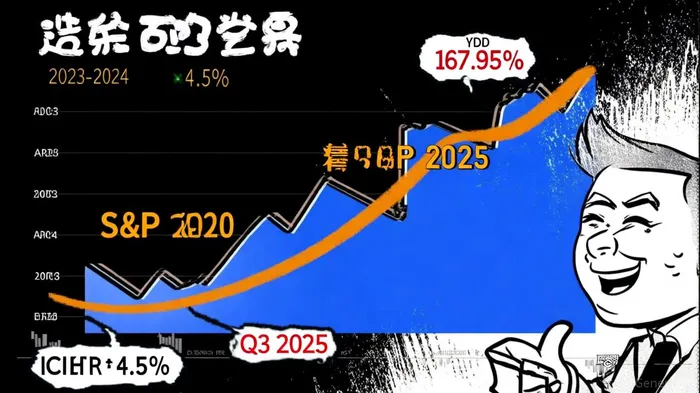

The semiconductor sector has long been a battleground for investors balancing near-term noise against long-term innovation. ACM ResearchACMR-- (ACMR), a key player in wafer processing equipment, exemplifies this tension. While the stock has surged 167.95% year-to-date (YTD) as of October 2025-far outpacing the S&P 500's 4.5% gain[1]-recent volatility has sparked debates about whether the market is overcorrecting to short-term risks or undervaluing its long-term potential.

The Short-Term Headwinds: Earnings Misses and Valuation Concerns

ACMR's recent performance has been a mixed bag. In Q2 2025, the company reported earnings per share (EPS) of $0.54, falling short of the $0.62 forecast[2]. While revenue hit $215.4 million-6.4% above the prior year-missing the $223.4 million estimate[2]-investors grew cautious. This led to a 1.33% single-day decline in October 2025, pushing the stock below its recent peak of $41.07 to $38.11[3]. Analysts now peg ACMR's fair value at $35.36, suggesting the stock is currently overvalued by ~12%[4].

Compounding concerns is ACMR's exposure to China's semiconductor market, which accounts for a significant portion of its revenue. While the CHIPS Act and global demand for AI-driven manufacturing should bolster long-term growth[5], U.S. export controls and potential retaliatory tariffs remain a wildcard[6]. This has led to a Zacks Rank of #3 (Hold), reflecting analysts' neutral stance[3].

The Long-Term Case: A Semiconductor Sector Powerhouse

Despite these near-term jitters, ACMR's fundamentals remain robust. The company's advanced cleaning and plating solutions-such as its N2 bubbling and SPM tools-are critical for next-generation semiconductor nodes, including 3D NAND and logic chips[1]. With global foundries ramping up investments in AI and advanced manufacturing, ACMRACMR-- is positioned to capture a growing share of this demand.

Revenue projections underscore this optimism. The company expects 2025 sales between $850 million and $950 million-a 18% year-over-year increase[5]-and analysts forecast $1.4 billion in revenue by 2028[6]. Its profitability metrics also stand out: an 18.6% margin and a forward P/E of 19.3x, significantly lower than the industry average of 38x[4]. This suggests ACMR is trading at a discount to peers, even as it outperforms the S&P 500 by a staggering margin[1].

The Misalignment: Sentiment vs. Substance

The core issue lies in investor sentiment. While ACMR's long-term growth drivers-semiconductor innovation, AI adoption, and expanding international operations-are compelling[5], short-term earnings volatility and geopolitical risks have created a valuation gap. For instance, despite a 164% YTD gain, the stock's recent dip has raised questions about whether the market is overreacting to near-term challenges[7].

However, this misalignment could present an opportunity. ACMR's P/E ratio of 21.05[1] and its ability to maintain full-year guidance despite Q2 hiccups[2] suggest the company's fundamentals are resilient. Moreover, its expansion into the U.S., Korea, and Europe-aiming to generate half its revenue outside China by 2026[5]-could mitigate some of its geopolitical risks.

Conclusion: A Stock for the Patient Investor

ACMR's recent underperformance relative to the broader market is a classic case of short-term noise clouding long-term potential. While near-term earnings misses and valuation concerns are valid, they fail to account for the company's dominant position in a sector poised for decades of growth. For investors with a 3–5 year horizon, ACMR's discounted valuation and strong revenue trajectory make it a compelling buy. However, those focused on quarterly volatility may want to wait for a clearer resolution of its earnings trajectory.

In the end, the semiconductor story is one of cycles and innovation. ACMR, with its cutting-edge technology and strategic diversification, is well-positioned to thrive in both.

Comentarios

Aún no hay comentarios