Abercrombie & Fitch's Valuation Dilemma: Underperformance Amid Sector Rotation and Tariff Uncertainties

The stock market's love affair with high-growth tech and energy sectors has left traditional retailers like Abercrombie & Fitch (ANF) in the dust. Yet, beneath the surface of its 50% year-to-date underperformance lies a compelling valuation story, one that could benefit from a shifting tide in sector rotation and a reevaluation of retail's role in a post-AI economy.

A Tale of Two Sectors: Retail's Struggle and ANF's Resilience

Abercrombie & Fitch's Q3 2025 results were a masterclass in operational execution. Revenue surged 14% to $1.21 billion, net income jumped 37% to $132 million, and profit margins expanded to 11%-a stark contrast to the broader U.S. specialty retail industry, which saw a 5.78% year-over-year revenue decline in Q2 2025, according to Yahoo Finance. The company's Hollister brand, a key growth driver, delivered 21% comparable sales growth, underscoring its dominance in the teen market, per FinTool.

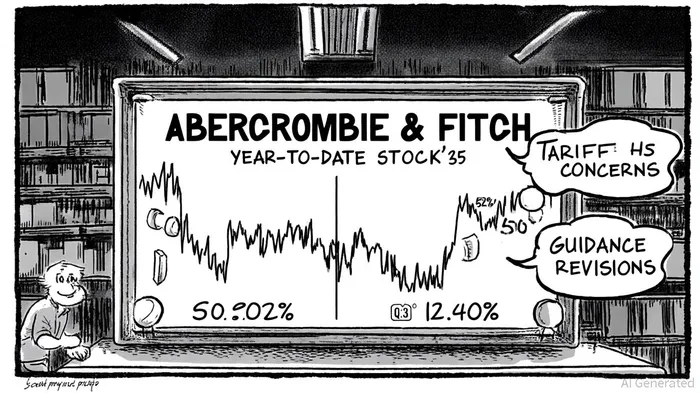

Yet, these fundamentals have done little to buoy its stock. ANF's YTD total return of -50.92% dwarfs the S&P 500's 12.40% gain, a disconnect that reflects broader investor skepticism toward retail amid trade tariff uncertainties and conservative guidance. The company's 2025 outlook-a projected 3%-5% sales growth and a potential operating margin contraction to 14%-15%-has left analysts wary, according to Trefis.

Valuation Metrics Suggest a Mispricing

ANF's valuation appears disconnected from its performance. With a trailing P/E of 6.94 and a forward P/E of 7.38, the stock trades at a steep discount to its peers' 16x average and the U.S. specialty retail industry's 16.7x multiple, per Simply Wall St. Analysts, led by a consensus price target of $119.30 (62.62% above the current price), see significant upside potential, according to Stock Analysis stats.

The PEG ratio, a critical metric for growth stocks, further highlights this mispricing. At 0.55, ANF's PEG ratio suggests it is undervalued relative to its 12.69% earnings growth over the trailing twelve months, per FinanceCharts. Meanwhile, the price-to-book ratio of 2.67 implies investors are paying less for every dollar of the company's book value compared to its historical averages, according to Stock Analysis ratios.

Sector Rotation: A Double-Edged Sword

The broader market's shift from tech to energy and industrials in 2025 has exacerbated retail's challenges. Capital flows into sectors with tangible assets-like ExxonMobil and Caterpillar-have left retailers like ANF struggling to attract attention, as noted by MarketMinute. However, this rotation may not be permanent. As AI-driven demand for energy infrastructure stabilizes, investors could pivot back to sectors offering durable cash flows and margin resilience.

For ANF, the key lies in navigating near-term headwinds. Tariff pressures, which have already dented its stock, remain a wildcard. Yet, the company's omnichannel strategy and brand revitalization efforts-contributing to a 155% surge in earnings per share since 2021-suggest it is well-positioned for a rebound, according to EasyTrader. A discounted cash flow analysis estimates its intrinsic value at $157 per share, implying an 82% upside, according to Yahoo Finance key statistics.

Conclusion: A High-Risk, High-Reward Proposition

Abercrombie & Fitch's underperformance is a symptom of macroeconomic forces and sector-specific risks, not operational failure. While trade tariffs and margin pressures linger, its valuation metrics and earnings trajectory present a compelling case for long-term investors. The question is whether the market will reprice retail's value in a world increasingly dominated by AI and energy transitions-or if ANF's current discount will persist as a cautionary tale of sector rotation.

For now, the stock remains a high-risk, high-reward opportunity. Those willing to bet on a retail rebound-and ANF's ability to adapt-may find themselves rewarded handsomely.

Comentarios

Aún no hay comentarios