Why S&P 500 Exclusion May Have Created a Buyable Inflection Point for MSTR

The recent exclusion of MicroStrategy (MSTR) from the S&P 500 has sparked a critical debate among investors: Is this a temporary setback, or does it signal a deeper mispricing of the company’s Bitcoin-driven strategy? For risk-tolerant investors, the answer may lie in the interplay of macroeconomic catalysts, crypto normalization, and the unique dynamics of high-conviction, volatile assets.

Strategic Mispricing and the S&P 500 Gatekeeping Effect

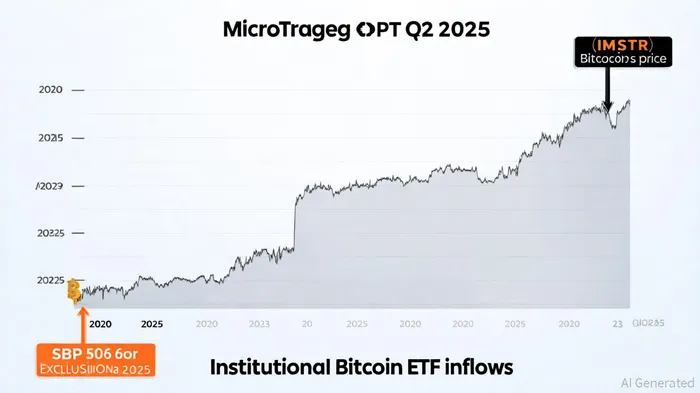

The S&P 500’s influence on institutional investment flows is well-documented. According to a report by Business Law Review, index inclusion often triggers demand from passive funds and benchmarked investors, while exclusion can reduce visibility and liquidity [3]. For MSTRMSTR--, its removal from the index in Q3 2025 coincided with a sharp decline in after-hours trading [1]. However, this exclusion does not negate the company’s core thesis: BitcoinBTC-- as a strategic treasury asset.

MicroStrategy’s Bitcoin holdings—valued at $71.2 billion as of Q2 2025—have generated a 55% return compared to a 14% cost of capital [2]. Yet, its stock has at times underperformed Bitcoin, creating a valuation gap. Steno Research notes that MSTR trades at a 300% premium to its Bitcoin stack, a mispricing unlikely to persist long-term [3]. This divergence highlights the challenges of valuing high-conviction assets in a market still grappling with crypto normalization.

Macro Tailwinds: Dovish Policy and Institutional Adoption

The Q3 2025 macroeconomic landscape has amplified the case for Bitcoin as a hedge. The Federal Reserve’s dovish pivot, signaled at Jackson Hole, has lowered the opportunity cost of holding risk assets [1]. Meanwhile, institutional adoption of Bitcoin has surged, with U.S. spot ETFs attracting $118 billion in Q3 2025 alone [1]. These ETFs have normalized Bitcoin’s role in conservative portfolios, with 59% of institutional investors now allocating to the asset [2].

For MSTR, this trend is a double-edged sword. While its exclusion from the S&P 500 limits passive fund inflows, the broader institutional embrace of Bitcoin could offset this. The company’s aggressive capital-raising—$6.8 billion via equity offerings in Q2 2025—has allowed it to accumulate 628,791 BTC, or 3% of all Bitcoin in existence [4]. This positions MSTR as a de facto leveraged proxy for Bitcoin, albeit with operational risks like dilution and volatility.

The Inflection Point: Mispricing as Opportunity

Historical precedents suggest that strategic mispricing in high-conviction assets often corrects over time. For example, the Russell 2000’s inclusion/exclusion dynamics show that excluded firms typically underperform, while included ones see price surges [1]. However, MSTR’s case is unique: Its exclusion may have created a liquidity discount, making its Bitcoin holdings relatively undervalued.

Analysts at Tiger Research argue that Bitcoin’s 30-day volatility index has fallen below 80%, a sign of maturing institutional demand [5]. This stability, combined with MSTR’s $13.2 billion BTC gain in Q2 2025 [4], suggests the company’s Bitcoin strategyMSTR-- is gaining traction. If Bitcoin reaches $190,000 as projected [4], MSTR’s intrinsic value could far outstrip its current stock price.

Risks and Considerations

Critics caution that MSTR’s valuation hinges on Bitcoin’s continued ascent and macroeconomic stability. A Fed reversal or regulatory crackdown could erode its premium. Additionally, the company’s reliance on capital markets—convertible bonds, equity sales—introduces dilution risks [2].

Yet, for investors with a multi-year horizon, these risks may be outweighed by the potential rewards. As BlackRock notes, diversification is increasingly challenging in a concentrated market dominated by the “Magnificent Seven” [3]. MSTR’s Bitcoin strategy offers an alternative path, leveraging crypto’s anti-correlation with traditional assets.

Conclusion: A Case for Strategic Conviction

MicroStrategy’s S&P 500 exclusion is a short-term headwind, but it may also be a catalyst for long-term value creation. In a world of rising inflation, dollar devaluation, and crypto normalization, the company’s Bitcoin holdings represent a strategic mispricing that could correct sharply. For risk-tolerant investors, this inflection point—driven by macroeconomic tailwinds and institutional adoption—presents a compelling case to reevaluate MSTR’s role in a diversified portfolio.

**Source:[1] What will drive crypto in Q3 2025 [https://www.blockscholes.com/research/bybit-x-block-scholes-quarterly-report-what-will-drive-crypto-in-q3-2025][2] Bitcoin's Institutional Adoption and Scarcity: A Catalyst for [https://www.bitget.com/news/detail/12560604938747][3] The (Mis)uses of the S&P 500 [https://businesslawreview.uchicago.edu/print-archive/misuses-sp-500][4] Strategy Announces Second Quarter 2025 Financial Results [https://www.strategy.com/press/strategy-announces-second-quarter-2025-financial-results_07-31-2025][5] Why Institutional Bitcoin Adoption Is Rising And What It ... [https://www.chainup.com/blog/institutional-bitcoin-adoption-what-it-means/]

Comentarios

Aún no hay comentarios