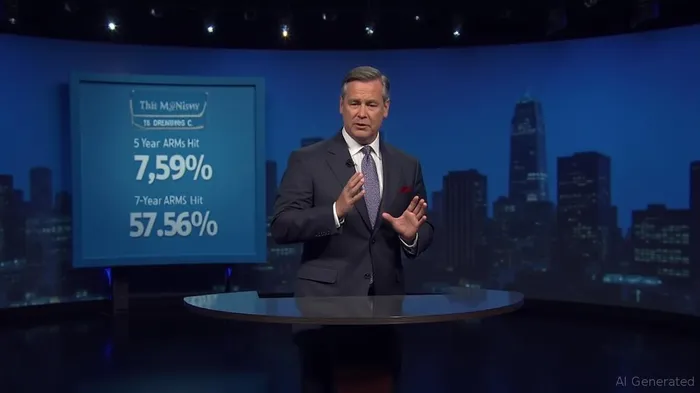

5-Year ARMs Hit 7.59% 7-Year ARMs at 7.56%

On June 23, 2025, the average rate for 5-year adjustable-rate mortgages (ARMs) stood at 7.59%, while the 7-year ARM rate was 7.56%. These rates are based on data from a popular real estate marketplace. ARMsARM-- offer a fixed interest rate for an initial period, after which the rate can fluctuate based on various factors, including benchmark rates, margins, and rate caps.

ARMs can be advantageous for certain homebuyers, such as those purchasing temporary or "starter homes," real estate investors, and buyers during periods of high interest rates. For temporary homebuyers, ARMs allow them to take advantage of the low fixed-period interest rate and sell the home before the adjustment period hits. Investors can secure a low interest rate upfront and adjust the rent or flip the property as the adjustment period approaches. During high interest rate periods, ARMs offer a lower rate upfront and potentially on the back end, assuming interest rates cool off by the time the fixed period expires.

ARMs typically start with a low, fixed interest rate for a set period, such as three, five, seven, or ten years. After this fixed period, the adjustment period begins, during which the interest rate can fluctuate. The rate is often based on the Secured Overnight Financing Rate (SOFR), a benchmark published by the U.S. Treasury. Lenders add a fixed margin to the SOFR to determine the ARM interest rate. Rate caps limit how much the rate can rise throughout the loan's duration.

Common ARM lengths include the 5/1, where the loan has a fixed interest rate for five years and then adjusts annually for the remaining 25 years, and the 10/6, where the fixed period is ten years and the adjustment period is 20 years with semi-annual adjustments. Other variations include 3/1, 7/1, and 10/1 ARMs.

Refinancing from an ARM to a fixed-rate mortgage is possible and may be advantageous for homeowners who decide to stay in their homes long-term. The process involves applying with multiple lenders, providing necessary documentation, closing on the new loan, and paying off the old loan.

ARMs come with both pros and cons. On the positive side, they offer the possibility of a lower interest rate upfront, lower borrower requirements, and the potential for decreasing monthly payments if interest rates drop. However, monthly payments can increase once the fixed rate expires, making it difficult to rate shop and providing less peace of mind compared to fixed-rate mortgages.

Comentarios

Aún no hay comentarios