5 Stocks on the Move: A Tactical Breakdown of This Week's Catalysts

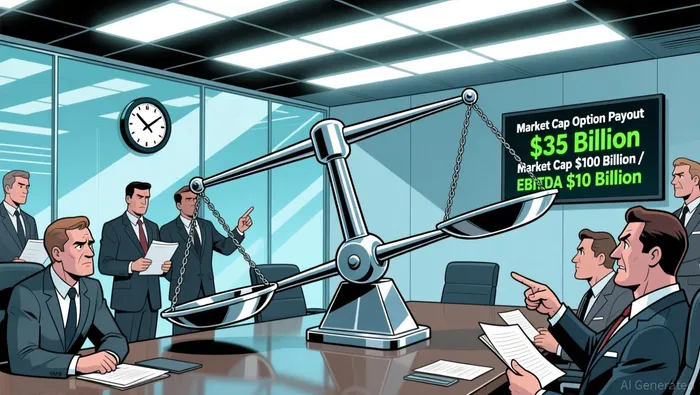

The buzz around GameStopGME-- is no longer about retail trading memes. It's about a high-stakes compensation plan. The catalyst is CEO Ryan Cohen's new stock option award, which could vest for a staggering potential payout of around $35 billion if the company hits two specific targets: a market capitalization milestone of $100 billion and a cumulative EBITDA milestone of $10 billion.

This creates a classic binary setup. The award's structure ties Cohen's personal fortune directly to a massive re-rating of the stock. For the payout to materialize, GameStop's market cap would need to multiply roughly tenfold from its current level of about $9.3 billion. That's a distant target, making the award a pure bet on the stock's ability to re-rate, not just grow earnings.

The current technical picture reflects skepticism. Despite a rise of over 600% in market cap since Cohen joined the board, the stock is under pressure, trading below key moving averages and near its 52-week lows. The recent RSI at 48.95 and bearish MACD signal mixed momentum, while analyst consensus remains a Hold with a price target of just $13.50.

The bottom line is that Cohen's award is a powerful, if extreme, catalyst. It crystallizes the high-risk, high-reward wager that GameStop's story is far from over. The stock's path now hinges on whether it can generate the kind of explosive growth and valuation shift required to make that $35 billion option award a reality.

Nvidia: Navigating the AI Spending Pause

The AI spending pause is hitting Nvidia where it hurts. Shares are down about 8% since hitting a record on Oct. 29, a notable pullback that has underperformed the broader market. This move crystallizes growing investor concerns about the sustainability of the massive AI investment cycle that fueled the stock's historic rally.

The immediate catalyst is a shift in the competitive landscape. While Nvidia still commands over 90% of the AI chip market, the pressure is mounting. The company is facing more competition than ever before from rivals like Advanced Micro Devices Inc., as well as from its own biggest clients. Tech giants like Alphabet and Amazon are actively building their own chips to reduce reliance on Nvidia's expensive accelerators, which can cost over $30,000 apiece. This dual threat-from external rivals and internal decoupling-creates a tangible risk to Nvidia's pricing power and growth trajectory.

The bottom line is a classic event-driven tension. The recent 8% drop is a direct reaction to near-term risks: spending fatigue and encroaching competition. But the high analyst targets suggest the long-term growth story-driven by a massive order backlog, new chip launches like Rubin, and a potential return to the Chinese market-remains intact. For now, the stock is caught between a pause in the AI spending cycle and the powerful momentum that could resume.

MicroStrategy: Bitcoin's Bullish Bet on the Balance Sheet

The immediate catalyst for MicroStrategy is a clear, aggressive bet on bitcoin's price. In early January, the company added 1,287 bitcoin for just over $116 million, boosting its total holdings to a massive 673,783 BTC. This move, funded by common stock sales, is a direct signal from Executive Chairman Michael Saylor that the company sees value in accumulating at current levels.

The accumulation is not just about bitcoinBTC--. MSTR also added $62 million to its cash reserves, bringing the total to $2.25 billion. This cash is earmarked for dividend payments, providing a buffer that could support the stock through volatility. The market's reaction was swift and positive: MSTR shares rose 4.5% in premarket action alongside a weekend rise in bitcoin to about $92,900.

Viewed as a tactical setup, this event is a bullish signal that aligns the company's balance sheet with its core thesis. By buying more bitcoin while also strengthening its cash position, MSTR is betting that the asset's price will continue its upward trajectory. The stock's move higher suggests investors are buying that bet for now.

The Memory Shortage Play: Micron's Supply Chain Edge

The buzz around Micron is driven by a hard, physical constraint: a severe memory shortage this year. The catalyst is the massive demand for AI chips, which are consuming memory at a rate that the industry cannot match. As Micron's business chief Sumit Sadana told CNBC, demand has "far outpaced our ability to supply that memory and, in our estimation, the supply capability of the whole memory industry."

This structural shortage is set to push prices sharply higher. Industry researcher TrendForce expects average DRAM memory prices to rise between 50% and 55% this quarter versus the fourth quarter of 2025. That kind of increase is described as "unprecedented."

Micron is positioned to benefit directly from this dynamic. The company is a key supplier to both Nvidia and AMD, the leading GPU makers. The new Rubin GPU, for example, comes with up to 288 gigabytes of next-generation HBM4 memory per chip. Because HBM production uses a "three-to-one basis" where one bit of HBM means forgoing three bits of conventional memory, Micron is prioritizing these high-growth, high-margin AI applications over other markets. This strategic shift, including the recent discontinuation of a consumer PC memory business, ensures its limited supply goes to the highest-demand clients.

The bottom line is a classic supply-demand squeeze playing out in real time. With prices expected to more than double in a single quarter and Micron's production lines already dedicated to AI, the company is well-placed to capture the resulting price and volume surge.

The AI Chip Rival: AMD's Strategic Push

The buzz around AMD is a direct reaction to Nvidia's stumble. As the AI spending cycle faces a pause, the world's most valuable company is on shaky stock market footing, with shares down about 8% since hitting a record on Oct. 29. This pullback has created a clear opportunity for its primary rival.

AMD is a key competitor in the AI chip market, gaining share as competition intensifies. The company has already won major data center orders from OpenAI and Oracle, and its data center revenue is projected to jump about 60% to almost $26 billion in 2026. In a market where Nvidia commands over 90% of the AI chip market, this growth is a structural catalyst. It signals that the competitive landscape is shifting, and investors are beginning to look beyond the dominant player.

The recent drop in Nvidia's stock price has amplified this dynamic. It crystallizes concerns about the sustainability of AI spending and Nvidia's grip on the market, which are risks AMD is not directly exposed to. This creates a potential mispricing in the broader narrative, where attention and investment could flow to the company best positioned to capture market share in a more competitive environment.

While AMD's own stock performance isn't detailed here, its position as a key competitor is the catalyst. The event is Nvidia's vulnerability, and AMD's strategic push is the response. For investors, this sets up a classic event-driven trade: a potential rotation from a stretched leader to a capable challenger as the AI investment cycle finds its footing.

Comentarios

Aún no hay comentarios