The $150 Trillion Mineral Wealth Opportunity: How the Supreme Court's Reversal of the Chevron Doctrine Is Unlocking a New Era for Resource Investors

The Supreme Court’s 2024 reversal of the ChevronCVX-- doctrine in Loper Bright Enterprises v. Raimondo has fundamentally reshaped the regulatory landscape for mineral rights and resource development in the United States. By eliminating the long-standing principle of judicial deference to federal agencies’ interpretations of ambiguous statutes, the ruling has created a more litigious but potentially more dynamic environment for resource investors. This shift, coupled with aggressive federal and corporate initiatives to secure domestic critical mineral supply chains, is unlocking access to an estimated $150 trillion in untapped mineral wealth, particularly in lithium, rare earth elements (REEs), copper, and cobalt [1]. For investors, this represents a once-in-a-generation opportunity to capitalize on a structural inflection point in the energy transition and geopolitical realignment.

The Chevron Reversal: A Catalyst for Regulatory Uncertainty and Opportunity

Prior to the Loper Bright decision, federal agencies like the Bureau of Land Management (BLM) and the Department of the Interior wielded broad discretion to interpret statutes governing mineral rights and resource regulation. This authority, rooted in the Chevron deference framework, allowed agencies to enforce rules even when statutory language was ambiguous [2]. The Court’s rejection of this doctrine now mandates that courts independently evaluate the “best reading” of statutes, effectively shifting the burden of legal interpretation from agencies to the judiciary [3]. While this has increased litigation risks, it has also weakened regulatory barriers to resource extraction, particularly on federal lands.

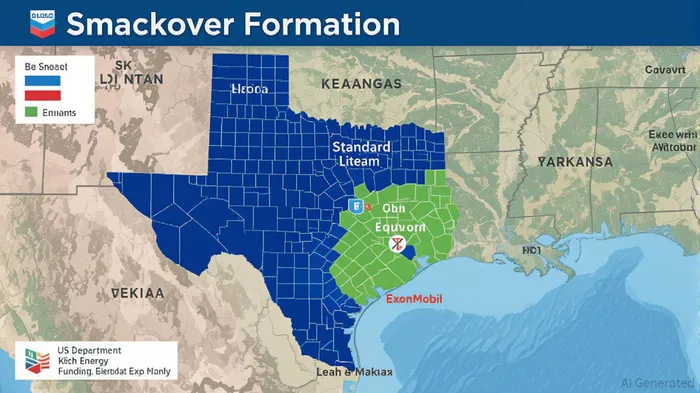

For example, the Smackover Formation in Texas and Arkansas—a lithium-rich brine deposit—has become a focal point for energy majors like Chevron, ExxonMobil, and EquinorEQNR--. Chevron’s recent acquisition of 125,000 net acres in the region, coupled with its deployment of direct lithium extraction (DLE) technology, exemplifies how companies are leveraging the post-Chevron environment to fast-track projects previously stalled by regulatory delays [4]. The U.S. Department of Energy (DOE) has further amplified this momentum by allocating nearly $1 billion in funding for critical mineral projects, including battery material processing and rare earth element (REE) recovery [5].

Actionable Investment Opportunities: From Lithium to Rare Earths

The post-Chevron regulatory shift has created a fertile ground for both established energy giants and junior mining firms to expand their portfolios. Key sectors and companies to watch include:

- Lithium: The Energy Transition’s Cornerstone

- Chevron (CVX): The oil giant’s entry into the lithium market via DLE technology in the Smackover Formation positions it to capitalize on projected 500-700% growth in lithium demand by 2030 [6]. Its partnership with Equinor and Standard Lithium’s joint venture in Arkansas, which aims to produce 22,500 tonnes of battery-grade lithium carbonate annually by 2028, underscores the sector’s scalability [7].

Smackover Lithium (Standard Lithium + Equinor): This joint venture has secured Arkansas’ first lithium royalty approval, with a 2.5% royalty rate and $65.05/acre annual brine fee. The project’s alignment with the DOE’s $1 billion critical minerals initiative further de-risks its commercial viability [8].

Rare Earth Elements (REEs): A National Security Priority

- Idaho Strategic Resources (IDR): With significant REE deposits in Idaho’s REE-Th Belt, this company is leveraging the U.S. government’s designation of REEs as critical minerals. Its dual focus on gold and REEs, combined with sustainable extraction methods, aligns with federal incentives for domestic supply chains [9].

MP Materials (MP): As the sole U.S. producer of rare earth elements, MP MaterialsMP-- is expanding its processing capabilities to meet surging demand for neodymium and dysprosium in electric vehicle motors and wind turbines [10].

Copper and Cobalt: The Backbone of Decarbonization

- TMC The Metals Company (TMC): This deep-sea mining pioneer is exploring polymetallic nodules in the Pacific, rich in nickel, cobalt, and copper. With the U.S. adding copper to its critical minerals list in 2025, TMC’s technology could address supply chain bottlenecks for EVs and renewable energy infrastructure [11].

- Sidney Resources Corp. (SDRC): Operating in Idaho’s Warren Mining District, SDRC’s focus on gold, silver, and copper aligns with the DOE’s emphasis on repurposing industrial byproducts for critical mineral recovery [12].

Government Policy: Accelerating the Transition

President Trump’s March 2025 executive order to streamline federal permitting for mineral projects has further catalyzed the sector. By designating 10 projects under the FAST-41 program and delegating emergency powers under the Defense Production Act, the administration is prioritizing domestic production of lithium, cobalt, and REEs [13]. This policy environment, combined with tax incentives like Arkansas’ sales-and-use tax exemption for lithium projects, is reducing capital costs for developers [14].

Risks and Considerations

While the post-Chevron landscape offers significant upside, investors must remain cautious. The shift to Skidmore deference—where courts consider agency interpretations as persuasive but not binding—could lead to inconsistent rulings across circuits, prolonging project timelines [15]. Additionally, the influx of capital into lithium and REEs may eventually lead to oversupply and pricing pressures, as seen in the solar panel and EV battery markets [16].

Conclusion

The Supreme Court’s reversal of the Chevron doctrine has dismantled a key regulatory barrier to resource development, while federal and corporate initiatives are accelerating the monetization of critical minerals. For investors, the path forward lies in identifying companies with strategic assets in high-demand sectors—lithium, REEs, copper, and cobalt—and strong alignment with policy tailwinds. As the energy transition gains momentum, the $150 trillion mineral wealth opportunity is no longer a hypothetical but a tangible reality for those positioned to act.

Source:

[1] Policy Earthquake: Supreme Court Ruling Reignites Debate [https://finance.yahoo.com/news/policy-earthquake-supreme-court-ruling-214400974.html]

[2] What's Next for the Regulatory Landscape Post-Chevron? [https://www.hklaw.com/en/insights/publications/2024/07/whats-next-for-the-regulatory-landscape-post-chevron]

[3] Litigation after the Demise of Chevron Deference [https://www.hugheshubbard.com/news/litigation-after-the-demise-of-chevron-deference]

[4] Chevron Enters Domestic Lithium Sector to Support U.S. Energy Security [https://www.chevron.com/newsroom/2025/q2/chevron-enters-domestic-lithium-sector-to-support-us-energy-security]

[5] DOE Announces Nearly $1 Billion to Secure US Critical Minerals and Materials Supply Chain [https://www.hunton.com/the-nickel-report/doe-announces-nearly-1-billion-to-secure-us-critical-minerals-and-materials-supply-chain]

[6] Investing in Critical Minerals: Growth Strategies for 2025 [https://discoveryalert.com.au/news/critical-minerals-investment-growth-strategies-2025/]

[7] Smackover Lithium's South West Arkansas Project Receives Special Designation [https://www.standardlithium.com/investors/news-events/press-releases/detail/190/smackover-lithiums-south-west-arkansas-project-receives]

[8] Lithium Updates from the Smackover Region [https://argentfinancial.com/argent-insights/lithium-updates-from-the-smackover-region/]

[9] 4 Stocks to Benefit from the American Mining Executive Order [https://www.nasdaq.com/press-release/4-stocks-benefit-american-mining-executive-order-2025-04-01]

[10] MP Materials Expands Rare Earth Processing [https://www.mp.com/newsroom]

[11] TMC The MetalsTMC-- Company’s Deep-Sea Nodule Exploration [https://www.tmcmetals.com]

[12] Buried Treasure: The U.S. Is Throwing Away Its Critical Minerals [https://www.earth.com/news/buried-treasure-the-u-s-is-throwing-away-its-critical-minerals/]

[13] Immediate Measures to Increase American Mineral Production [https://www.whitehouse.gov/presidential-actions/2025/03/immediate-measures-to-increase-american-mineral-production/]

[14] Arkansas Sales-and-Use Tax Exemption for Lithium Projects [https://argentfinancial.com/argent-insights/lithium-updates-from-the-smackover-region/]

[15] Who Gets to Say? Agency Deference in a Post-Chevron World [https://nationalaglawcenter.org/who-gets-to-say-agency-deference-in-a-post-chevron-world-skidmore-v-swift/]

[16] Golden Opportunity as Financing Constraints Create Supply Gaps in Junior Mining [https://www.cruxinvestor.com/posts/golden-opportunity-as-financing-constraints-create-supply-gaps-in-junior-mining-across-essential-commodities]

Comentarios

Aún no hay comentarios