Hot CPI Meets Jobless Spike: Why Markets Still See a Fed Cut Frenzy Ahead

The August Consumer Price Index delivered a mixed message to investors, policymakers, and markets just days before the Federal Reserve convenes for its September meeting. While the headline numbers generally came in line with expectations, the monthly increase ran hotter than consensus, reinforcing the persistence of certain inflationary pressures. At the same time, labor market data released alongside CPI showed an unexpected surge in jobless claims, a development that may carry as much weight for the Fed’s deliberations as the inflation report itself. Together, the data cement expectations for a 25 basis point cut next week, while largely eliminating the possibility of a more aggressive 50 basis point move.

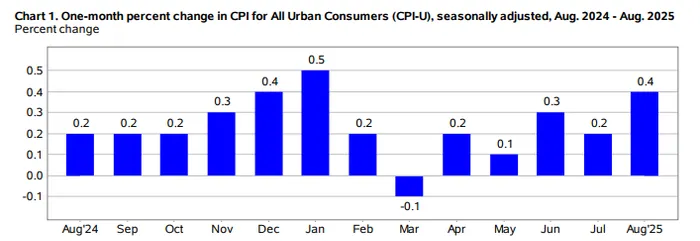

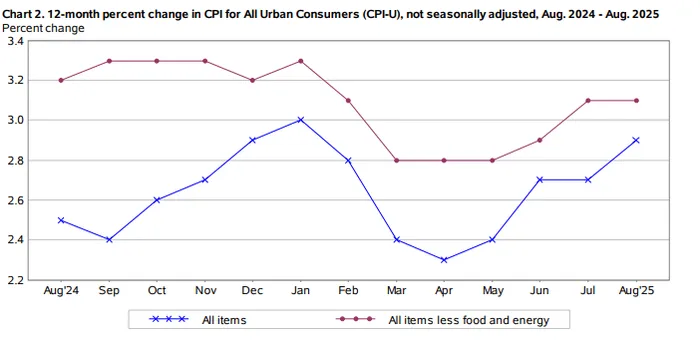

The CPI headline index rose 0.4 percent in August, above consensus expectations of a 0.3 percent gain, and double the 0.2 percent increase recorded in July. On a year-over-year basis, headline CPI rose 2.9 percent, precisely in line with expectations, and up modestly from July’s 2.7 percent annual pace. Core CPI, which strips out volatile food and energy components, increased 0.3 percent on the month and 3.1 percent over the prior year, both exactly in line with consensus. In short, while the monthly print underscored sticky price pressures, the annual trends suggest that inflation remains contained near 3 percent, giving the Fed some breathing room to proceed with its long-telegraphed easing cycle.

Breaking down the categories, shelter once again played its familiar role as the largest driver of monthly price gains. The index rose 0.4 percent in August, reflecting increases in both rents and owners’ equivalent rent, while lodging away from home jumped 2.3 percent. Shelter inflation has proven the most stubborn component in the CPI basket, and while it has moderated somewhat over the past year, it continues to provide an outsized contribution to the monthly increase. Food prices also accelerated, climbing 0.5 percent in August after being unchanged in July. All six major grocery store food categories posted gains, with notable spikes in fruits and vegetables (+1.6 percent, led by tomatoes and apples), and meats861191--, poultry, fish, and eggs (+1.0 percent, with beef prices up across the board). Coffee prices surged as well, with roasted and instant categories posting increases above 3 percent.

Energy contributed to the hotter-than-expected headline figure. After falling 1.1 percent in July, the energy index rose 0.7 percent in August, driven by a 1.9 percent rebound in gasoline. Electricity ticked slightly higher, while natural gas prices fell. On a year-over-year basis, energy prices remain subdued, with gasoline down 6.6 percent, but the monthly volatility highlights the sensitivity of headline inflation to commodity markets.

Core goods and services presented a mixed picture. Airline fares surged 5.9 percent in August, compounding a 4.0 percent increase the prior month. Apparel climbed 2.2 percent, reversing softness earlier this summer, while used cars and trucks rose 1.0 percent after months of choppiness. Tobacco products and motor vehicle maintenance also saw sharp increases. On the flip side, medical care services861198-- dipped slightly, with dental and prescription drug costs easing, partially offset by gains in physician services. Recreation and communication indexes also slipped modestly.

The breadth of the August report suggests that while inflation was not broadly accelerating across all categories, several sticky components—including shelter, services tied to travel, and parts of the food complex—are still rising faster than desired. Tariffs may be beginning to exert influence as well. Oxford IndustriesOXM--, in its recent earnings, flagged tariff-related pressures, and the rise in apparel prices this month could reflect some of those cost pass-throughs. However, for now the tariff impact looks uneven and not yet systemic across the CPI basket.

While CPI dominated headlines, the bigger surprise came from the labor market. Initial jobless claims spiked to 263,000 in the week ending September 6, well above consensus expectations of 235,000 and the prior week’s 236,000. This marks the highest level since October 2021. The four-week moving average climbed to 240,500 from 230,750, underscoring that the rise is not just a one-week anomaly. Continued claims, however, held steady at 1.939 million. The jump in claims reinforces the narrative of a cooling labor market and may overshadow the CPI release in shaping the Fed’s decision.

Markets interpreted the dual data points as supportive of further easing. Rates futures are now pricing four consecutive 25 basis point cuts at each of the Fed’s remaining meetings this year, the most dovish outlook investors have embraced in 2025. Importantly, the hotter monthly CPI print was enough to take a 50 basis point move off the table next week, but not enough to derail expectations for a steady easing cycle. Treasury yields fell, with the 10-year dipping below 4 percent for the first time since early April, reflecting a combination of softer labor market signals and conviction that inflation pressures are no longer spiraling.

Equities initially dipped on the CPI headline before reversing higher as claims data reinforced expectations for a dovish Fed. The S&P 500 futures pushed back toward session highs, while the euro strengthened modestly against the dollar, aided by the rate differential narrative.

In sum, the August CPI report, coupled with jobless claims, leaves the Fed on track to cut 25 basis points next week, while virtually closing the door on a larger cut. The data highlights the ongoing tug-of-war between sticky inflation in categories like shelter and food and the broader disinflationary impulse from goods and a cooling labor market. With markets now pricing the most aggressive easing path of the year, attention turns to the Fed’s September meeting, where policymakers must balance managing expectations with reaffirming their commitment to data dependency. The August data gives them cover to begin cutting, but it also warns against complacency: the battle against sticky inflation is not yet won.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet